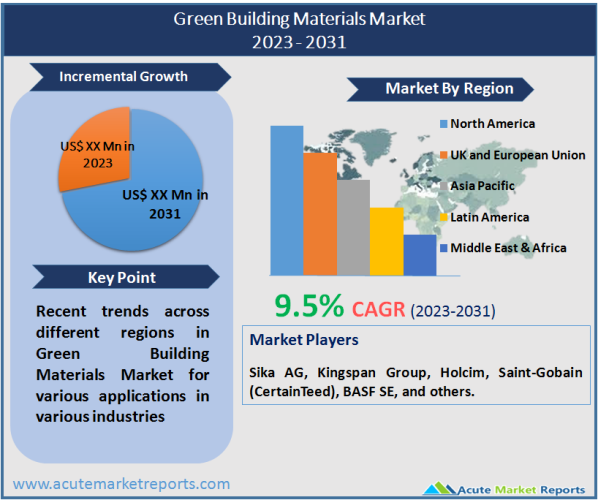

The global market for green building materials is anticipated to grow at a CAGR of 9.5% during the forecast period of 2024 to 2032. The outbreak of COVID-19 in 2020 and the first half of 2021 had a significant impact on the global construction industry due to government-imposed bans and restrictions, thereby restraining the growth of the market for green building materials. Residential real estate was hardest hit, as strict lockdown measures in major cities halted home registrations and slowed the distribution of home loans. Since these restrictions were lifted, however, the sector has been recovering strongly. Over the past two years, the market recovery has been driven by a rise in home sales, the introduction of new projects, and a rise in demand for new offices and commercial spaces.

The potential application of green building materials in energy-efficient buildings is the major factor driving the growth of the studied market over the medium term. In addition, there are favorable government policies that support green building construction and ensure industry-wide standardization of practices. These policies are compelling construction material manufacturers to incorporate more green material compositions/systems into their products. On the other hand, the high initial capital investments for green building construction compared to conventional buildings are expected to be the key factor restraining the growth of the studied market over the forecast period. Nonetheless, the increasing emphasis of various economies on achieving carbon neutrality, the declining operating costs of green buildings over time, and the rising trends in recycled construction are likely to generate lucrative growth opportunities in the global market in the near future. During the forecast period, North America is anticipated to dominate the market. This dominance is a result of the high demand for framing, roofing, insulation, and other applications in the residential, commercial, industrial, and infrastructure markets.

Increased Cost Savings remains the Most Impactful Market Driver

Green building materials are defined as non-toxic, eco-friendly, and sustainable materials that result in improved occupant health decreased energy costs and decreased energy consumption. The operating costs of green buildings are lower than those of conventional buildings, as they consume 63% less water and 55% less electricity. The market for green building materials is segmented based on application, end-user industry, and region. By application, the market is divided into framing, insulation, roofing, exterior siding, and interior finishing. The market is segmented by end-user industry into residential, commercial, industrial and institutional, and infrastructure segments. In addition, the report provides market size and forecasts for the green building materials market in 15 countries across the world's most important regions. The market size and forecasts for each segment have been determined based on revenue (USD million).

Structural Segment Dominated the Market by Product

By product type, structural accounted for over 65% of the construction sustainable materials market share in 2023. In addition to reducing the carbon footprint, structural products offer exceptional durability at an affordable price. The expansion of the construction industry, particularly in developing nations, will likely drive market expansion. The increasing popularity and use of various cladding styles on residential buildings increase the demand for construction sustainable insulation materials that provide air and weatherproofing while accommodating any post-construction movement or stresses the buildings may be subjected to. Insulation materials enhance the durability of repaired joints and provide an efficient means of enhancing the building's overall sustainability without requiring the substitution of existing building materials.

Insulation Segment Dominated the Application Market

By application, insulation accounted for more than 28.0% of the market for sustainable construction materials in 2023. Insulation of the roof, walls, attic, and foundations is essential for energy-efficient residential construction. Due to the inefficiency of glass as an insulator, the insulation of see-through windows, envelopes, and skylights significantly reduces heat loss or gain, thereby reducing heat transfer and vapor condensation. Consequently, insulation materials prevent humidity, freezing, mold, and deformation caused by corrosion in construction works, thereby protecting the building.

Residential Constructions remains the Dominant End User

In 2023, residential construction accounted for 45.0% of the market share for sustainable materials in the construction industry. The increasing global population and urbanization rate are responsible for the expansion of both new construction and renovation projects. Strict government regulations to reduce environmental pollution and improve the building's energy efficiency are major factor driving market demand.

Historically, the residential end-user segment of the global market for sustainable building materials has held a significant share. Sustainable building materials for residential settings such as apartments, villas, flats, housing complexes, communities, etc., have gained significant traction due to the growing demand for energy-efficient residential buildings. In addition, the use of renewable power sources, proper insulation, recyclable materials for window panes, doors, and roofing, as well as sustainable coatings for water-proofing and preventing leakage, etc., has expanded the global market for Sustainable Building Materials. Moreover, the growing emphasis on promoting sustainability in residential building construction and the requirement for energy certification of buildings have also contributed to market expansion. In this regard, the Government of India has provided various incentive programs in its various states for buildings rated by the Indian Green Building Council (IGBC) in India. Consequently, it is anticipated that these initiatives will further accelerate the growth of the global market for sustainable building materials between 2023 and 2031.

Increasing Green Building Material Consumption in the Residential Segment

The residential sector is the primary market for green building materials in 2023. Diverse green building materials are gaining popularity in residential construction due to the rising demand for materials that are energy-efficient, moisture-resistant, long-lasting, and simple to maintain. Factors such as personal safety, growing awareness and affinity for green building materials, and government regulations support the continued expansion of the residential use of green building materials.

The residential construction industry is increasingly incorporating green building materials such as fiber cement siding, thermally modified wood, bamboo, fly ash or ashcrete, hempcrete, and recycled plastic. Other natural materials such as cellulose, hemp, and cork are utilized for insulation purposes. Natural fibers such as cotton, jute, and wool, recycled materials such as terrazzo, and recycled concrete, stucco, stone, and rubber-based materials are also used in the residential sector for a variety of applications.

The governments of numerous nations are providing green housing incentives to encourage the development of environmentally friendly residential projects. For example, tax credits in the United States and Spain, the Green Mark incentive program in Singapore, and subsidies in New Zealand encourage the construction of green residential buildings in the country, which is likely to benefit the studied market.

Japan has made significant strides in green building leadership over the past year, and its impressive Leadership in Energy and Environmental Design (LEED) portfolio continues to expand. Japan has more than 268 LEED-certified projects totaling approximately 29,500,000 square feet. Additionally, the KreditanstaltfürWiederaufbau (KfW) program in Germany offers low-interest loans and grants for construction and renovation projects with certification ratings exceeding code performance. China is the largest construction market in the world. The Chinese government prioritized the country's Thirteenth Five-Year Plan, which includes initiatives for green building. The country's national climate commitment requires that 50 percent of all new buildings constructed by 2020 be certified as environmentally friendly. India has approximately 6,548 green building projects registered. The IIA and the CII-IGBC signed an agreement in June 2021 to promote green building practices in the fields of architectural design and planning. Utilization and demand for green building materials for residential construction applications are anticipated to increase during the forecast period due to the aforementioned factors.

North America Remains as the Global Leader

In North America, the primary factor driving the growth of the green building materials market is the high consumption of green building materials across all types of construction activities. In the United States, the LEED rating system is the most popular green building rating system. It provides a framework for green buildings that are healthy, efficient, carbon-saving, and cost-saving. Buildings with the LEED certification save money, increase efficiency, and reduce carbon emissions. As of October 2023, the United States had approximately 20,125 Certified LEED projects, 21,068 Silver projects, 21,206 Gold projects, and 7,027 Platinum projects, according to the USGBC.

According to the US Energy Information Administration, the residential and commercial sectors accounted for 28% of the nation's end-use energy consumption in 2021, consuming a total of 21 quadrillion Btu. The US government has announced plans to invest USD 3.16 billion to transform approximately 450,000 homes in low-income areas into energy-efficient structures and reduce the country's utility bills in response to the high energy demand of buildings. In order to protect the environment and mitigate the effects of climate change, the Canadian government has pledged to reduce the country's total greenhouse gas emissions by 40-45 percent below 2005 levels by 2030 and to net zero by 2050. The Canada Green Buildings Strategy was allocated 150 million CAD in the country's budget for 2023 in order to achieve these objectives. To achieve this objective, this strategy will mobilize national action to transform markets and reduce costs.

According to the WGBC, the sector with the best performance in Canada for green buildings is new institutional construction. Currently, more than one-third of all new projects in the country are environmentally friendly, and this proportion is projected to increase substantially in the coming years. The expansion of the green building industry in Canada is driven by environmental regulations and efforts to reduce energy consumption.

According to the USGBC, Mexico ranked tenth globally in terms of square feet (sq. ft.) of LEED certification in 2021, with a total of 47 projects certifying 10,285,729.57 sq. ft. Additionally, as of December 2021, two Mexican REITs, Fibra Macquarie and Fibra Shop, were in the process of obtaining green certification for their entire portfolios via a combination of retrofit investments and higher quality-on-entry standards. Additionally, privately held Mexican companies demonstrate their commitment to LEED and green building.

All of the aforementioned factors are likely to stimulate the growth of the green building materials market in North America over the forecast period.

Market Competition to Intensify During the Forecast Period

The global market for green building materials is fragmented, with many players holding small market shares. Some of the major corporations include Sika AG, Kingspan Group, Holcim, Saint-Gobain (CertainTeed), BASF SE, and others. The leading players in the market for sustainable construction materials are outfitted with advanced production facilities and engage in numerous R&D initiatives.

Historical & Forecast Period

This study report represents analysis of each segment from 2022 to 2032 considering 2023 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2024 to 2032.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Green Building Materials market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2022-2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Year | 2022 |

| Unit | USD Million |

| Segmentation | |

Application

| |

End-use Industry

| |

Type

| |

|

Region Segment (2022-2032; US$ Million)

|

Key questions answered in this report