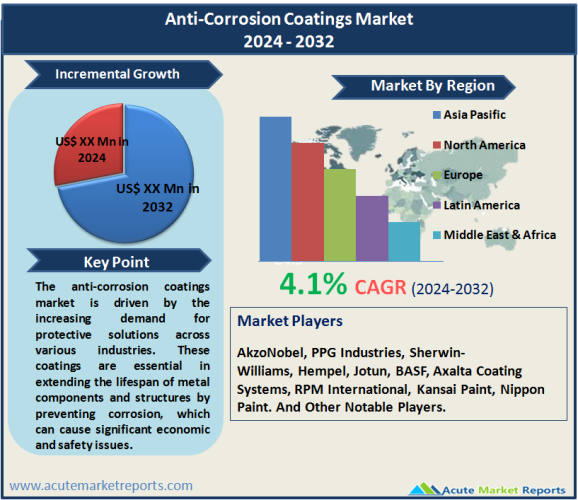

The anti-corrosion coatings market is expected to grow at a CAGR of 4.1% during the forecast period of 2026 to 2034, driven by the increasing demand for protective solutions across various industries. These coatings are essential in extending the lifespan of metal components and structures by preventing corrosion, which can cause significant economic and safety issues. Key conclusions from the market analysis indicate that the demand for anti-corrosion coatings is expected to continue rising due to their critical role in maintaining the integrity and performance of infrastructure, industrial machinery, and transportation equipment. The geographic analysis highlights the regional trends and growth opportunities, with Asia-Pacific leading in revenue and Europe expected to register the highest CAGR. The competitive landscape underscores the strategic efforts of leading companies to enhance their market presence and drive innovation. Overall, the anti-corrosion coatings market is set to achieve substantial growth, driven by the increasing demand for efficient, sustainable, and cost-effective corrosion protection solutions across various regions and applications.

Key Drivers

Rising Infrastructure Development

Infrastructure development is a major driver of the anti-corrosion coatings market. Governments and private sectors globally are investing heavily in infrastructure projects, including bridges, highways, railways, and airports. These structures are constantly exposed to harsh environmental conditions, making them susceptible to corrosion. For instance, the construction boom in emerging economies such as China and India has significantly boosted the demand for anti-corrosion coatings. In China, the government's Belt and Road Initiative, which aims to enhance regional connectivity through massive infrastructure development, has created a substantial market for anti-corrosion coatings. Similarly, in India, the Smart Cities Mission and other urban development programs have driven the need for durable and long-lasting construction materials. Anti-corrosion coatings are applied to steel and other metal components used in these projects to protect them from moisture, chemicals, and extreme weather conditions, thereby ensuring the longevity and safety of the structures. Moreover, the increasing focus on sustainable infrastructure and the adoption of advanced materials has further propelled the demand for high-performance anti-corrosion coatings that comply with environmental regulations and provide superior protection.

Growth in the Oil & Gas Industry

The oil and gas industry is another significant driver of the anti-corrosion coatings market. This industry involves extensive use of metal infrastructure, such as pipelines, rigs, and storage tanks, which are exposed to corrosive environments, including seawater, chemicals, and high temperatures. Corrosion can lead to catastrophic failures, environmental disasters, and substantial financial losses. Therefore, the oil and gas sector invests heavily in anti-corrosion coatings to protect their assets. The increasing exploration and production activities, particularly in offshore regions, have heightened the demand for advanced anti-corrosion solutions. Companies like AkzoNobel, PPG Industries, and Sherwin-Williams have developed specialized coatings that offer enhanced resistance to harsh marine environments and chemical exposures. For instance, AkzoNobel's Intershield 300 series is widely used in offshore platforms due to its excellent anti-corrosive properties and durability. Additionally, the rising global energy demand and the shift towards deepwater and ultra-deepwater drilling have further fueled the need for reliable anti-corrosion coatings. These coatings not only extend the operational life of equipment but also minimize maintenance costs and downtime, thereby improving the overall efficiency of oil and gas operations.

Increasing Automotive Production

The automotive industry has also significantly contributed to the growth of the anti-corrosion coatings market. As automotive manufacturers strive to enhance vehicle durability and performance, the application of anti-corrosion coatings has become essential. These coatings protect various automotive components, including body panels, underbodies, and engine parts, from rust and corrosion caused by exposure to moisture, road salts, and other environmental factors. The rising production of vehicles, particularly in regions like Asia-Pacific and North America, has driven the demand for high-quality anti-corrosion coatings. For example, China, the world's largest automotive market, has seen a surge in vehicle production, leading to increased consumption of anti-corrosion coatings. Similarly, in North America, the automotive industry's recovery post the COVID-19 pandemic has spurred the demand for corrosion protection solutions. Major players in the coatings industry, such as BASF and Axalta Coating Systems, provide advanced anti-corrosion coatings specifically designed for automotive applications. BASF's CathoGuard series, for instance, offers excellent corrosion resistance and is widely used in automotive manufacturing. Additionally, the growing trend towards electric vehicles (EVs) has further boosted the demand for anti-corrosion coatings. EVs require specialized coatings to protect battery components and electrical systems from corrosion, ensuring safety and performance. As the automotive industry continues to evolve and expand, the demand for anti-corrosion coatings is expected to grow, driven by the need for enhanced durability and reliability of vehicles.

Key Restraint

Stringent Environmental Regulations

One of the primary restraints in the anti-corrosion coatings market is the stringent environmental regulations imposed by governments and regulatory bodies worldwide. These regulations aim to minimize the environmental impact of coatings by restricting the use of volatile organic compounds (VOCs) and hazardous chemicals commonly found in traditional anti-corrosion coatings. For instance, the European Union's REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) regulation and the U.S. Environmental Protection Agency's (EPA) rules on VOC emissions have posed significant challenges to coating manufacturers. Compliance with these regulations often requires reformulating existing products or developing new environmentally friendly alternatives, which can be costly and time-consuming. Moreover, the growing emphasis on sustainability and green manufacturing practices has led to increased scrutiny of the raw materials and production processes used in the coatings industry. Companies are now required to invest in research and development to create eco-friendly coatings that offer the same level of performance and protection as traditional products. While these regulations are essential for protecting the environment and human health, they can also limit market growth by increasing production costs and creating barriers to entry for new players. Nonetheless, the industry is gradually adapting to these challenges by innovating and developing sustainable solutions that meet regulatory requirements without compromising on quality and performance.

Market Segmentation by Type

The anti-corrosion coatings market is segmented by type, including epoxy, polyurethane, acrylic, alkyd, zinc, chlorinated rubber, and others. In 2025, epoxy coatings generated the highest revenue due to their excellent adhesion, chemical resistance, and durability. Epoxy coatings are widely used in various applications, including marine, oil & gas, and industrial, where superior protection against corrosion is critical. Their versatility and effectiveness make them a preferred choice for protecting metal surfaces exposed to harsh environments. For instance, in the marine industry, epoxy coatings are extensively used on ship hulls, offshore platforms, and other marine structures to prevent corrosion caused by saltwater and marine organisms. Companies like Hempel and Jotun have developed high-performance epoxy coatings that provide long-lasting protection and meet stringent environmental standards. However, the polyurethane coatings segment is expected to register the highest CAGR during the forecast period of 2026 to 2034. Polyurethane coatings offer excellent flexibility, abrasion resistance, and UV stability, making them suitable for a wide range of applications. These coatings are increasingly used in automotive, infrastructure, and construction sectors to protect surfaces from corrosion and enhance their aesthetic appeal. The growing demand for durable and aesthetically pleasing coatings in these industries is expected to drive the growth of the polyurethane coatings segment. Additionally, the development of waterborne polyurethane coatings, which offer lower VOC emissions and improved environmental performance, is expected to further boost the market growth. The continuous innovation in coating technologies and the increasing focus on sustainability are likely to drive the demand for both epoxy and polyurethane coatings in the coming years.

Market Segmentation by Technology

The market segmentation by technology includes solvent-borne, waterborne, powder-based coating, and others. In 2025, solvent-borne coatings generated the highest revenue due to their widespread use and superior performance characteristics. Solvent-borne coatings are known for their excellent adhesion, durability, and resistance to harsh environmental conditions. They are commonly used in industrial applications, including oil & gas, marine, and infrastructure, where robust protection against corrosion is essential. However, the powder-based coating segment is expected to register the highest CAGR during the forecast period of 2026 to 2034. Powder-based coatings offer several advantages, including low VOC emissions, high durability, and a wide range of color options. These coatings are applied electrostatically and then cured under heat, resulting in a hard, protective finish. The growing focus on sustainability and the increasing adoption of environmentally friendly coating solutions are expected to drive the demand for powder-based coatings. Additionally, the automotive and transportation industries are increasingly using powder-based coatings to enhance the corrosion resistance and aesthetic appeal of vehicles and components. Companies like PPG Industries and AkzoNobel are leading providers of powder-based coatings, offering innovative solutions that meet stringent environmental regulations and provide superior performance. The continuous development of advanced coating technologies and the growing awareness of the environmental impact of traditional coatings are expected to drive the growth of both solvent-borne and powder-based coatings in the coming years.

Market Segmentation by End-Use

The anti-corrosion coatings market is segmented by end-use, including marine, oil & gas, industrial, infrastructure, power generation, automotive & transportation, and others. In 2025, the oil & gas industry accounted for the highest revenue due to the extensive use of anti-corrosion coatings in protecting pipelines, storage tanks, and offshore platforms. The harsh environments and exposure to corrosive substances in this industry necessitate the use of high-performance coatings to ensure the longevity and safety of assets. Companies like Sherwin-Williams and Hempel provide specialized anti-corrosion coatings for the oil & gas sector, offering superior protection and durability. However, the infrastructure segment is expected to register the highest CAGR during the forecast period of 2026 to 2034. The increasing investments in infrastructure development, particularly in emerging economies, are driving the demand for anti-corrosion coatings. These coatings are used to protect bridges, highways, airports, and other structures from corrosion caused by environmental factors. The growing focus on sustainable and resilient infrastructure is expected to boost the demand for high-performance anti-corrosion coatings in this segment. Additionally, the industrial sector is also expected to witness significant growth, driven by the increasing automation and digitalization of manufacturing processes. The use of anti-corrosion coatings in industrial machinery and equipment helps prevent downtime and maintenance costs, ensuring smooth and efficient operations. The continuous innovation in coating technologies and the development of environmentally friendly solutions are likely to drive the growth of the anti-corrosion coatings market across various end-use industries in the coming years.

Geographic Segment

Geographically, the anti-corrosion coatings market exhibits varying trends and growth patterns across different regions. In 2025, the Asia-Pacific region generated the highest revenue, driven by rapid industrialization, urbanization, and infrastructure development in countries such as China, India, and Japan. The robust economic growth in these countries has led to increased investments in construction, automotive, and marine industries, which are significant consumers of anti-corrosion coatings. China's Belt and Road Initiative, India's Smart Cities Mission, and Japan's extensive infrastructure projects have created substantial demand for durable and high-performance anti-corrosion coatings. Additionally, the presence of major manufacturing hubs in Asia-Pacific has further fueled the market growth, as industries seek to protect their assets from corrosion and enhance operational efficiency. The region's dominance in the anti-corrosion coatings market is also attributed to the availability of raw materials and low production costs, which attract manufacturers to establish their production facilities in this region. However, Europe is expected to register the highest CAGR during the forecast period of 2026 to 2034. The stringent environmental regulations and the increasing focus on sustainability have driven the demand for eco-friendly anti-corrosion coatings in Europe. The region's well-established automotive, marine, and industrial sectors are significant consumers of advanced coating solutions. Countries like Germany, France, and the UK are leading adopters of high-performance anti-corrosion coatings, driven by the need to comply with regulatory standards and enhance the durability of assets. The growing emphasis on green manufacturing practices and the adoption of advanced coating technologies are expected to drive market growth in Europe. Additionally, the North American market is also expected to witness substantial growth, driven by the recovery of the automotive industry and the increasing investments in infrastructure development. The continuous innovation in coating technologies and the development of sustainable solutions are likely to drive the growth of the anti-corrosion coatings market across various regions in the coming years.

Competitive Trends

The anti-corrosion coatings market is highly competitive, with key players focusing on strategic initiatives such as mergers and acquisitions, product innovation, and expansion into emerging markets to strengthen their market position. Major companies in the market include AkzoNobel, PPG Industries, Sherwin-Williams, Hempel, Jotun, BASF, Axalta Coating Systems, RPM International, Kansai Paint, and Nippon Paint. These companies have been continuously innovating to develop advanced coating solutions that offer superior protection and comply with stringent environmental regulations. For instance, AkzoNobel has been investing in research and development to introduce eco-friendly coatings that provide high performance and meet regulatory standards. The company's focus on sustainability and innovation has enabled it to maintain a strong market presence. Similarly, PPG Industries has been expanding its product portfolio and enhancing its distribution network to cater to the growing demand for anti-corrosion coatings in various industries. The company's strategic acquisitions and collaborations have further strengthened its market position. Sherwin-Williams, known for its extensive range of protective coatings, has been focusing on expanding its global footprint and enhancing its product offerings. The company's acquisition of Valspar Corporation has significantly boosted its market share and product portfolio. Hempel and Jotun, leading providers of marine coatings, have been focusing on developing high-performance solutions that offer long-lasting protection in harsh marine environments. These companies have been expanding their presence in emerging markets to tap into the growing demand for anti-corrosion coatings. BASF and Axalta Coating Systems have also been investing in advanced coating technologies and expanding their production capacities to meet the increasing demand for sustainable and high-performance coatings. The continuous innovation and strategic initiatives by these key players are expected to drive the competitive dynamics and foster growth in the anti-corrosion coatings market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Anti-Corrosion Coatings market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Technology

|

|

End-Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report