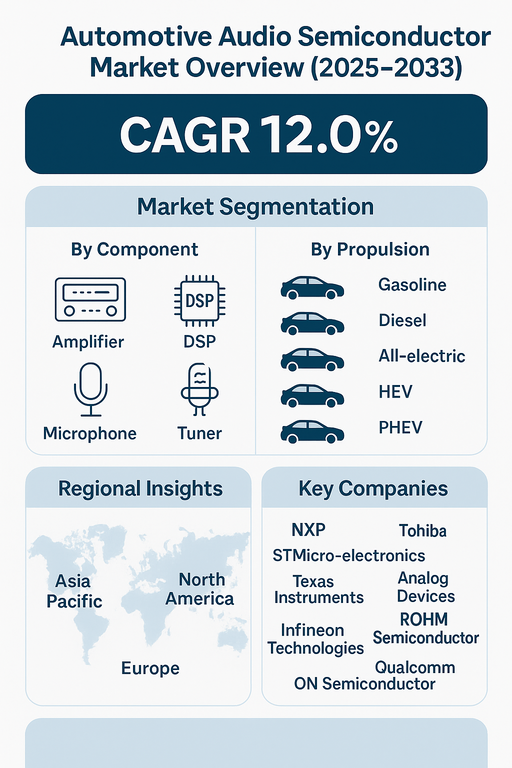

The global automotive audio semiconductor market is projected to expand at a CAGR of 12.0% from 2025 to 2033. Growth is driven by rising demand for advanced in-vehicle infotainment systems, premium audio solutions, and connectivity features across passenger and commercial vehicles. As consumers increasingly expect immersive in-car experiences, automakers are integrating high-performance audio semiconductors to support voice recognition, noise cancellation, and seamless smartphone integration.

Increasing Demand for In-Vehicle Infotainment

The expansion of connected and autonomous vehicles is significantly boosting demand for audio semiconductors. Amplifiers, digital signal processors (DSPs), microphones, and tuners are increasingly essential for advanced infotainment, hands-free communication, and driver-assist applications. Electric and hybrid vehicles further enhance this trend, as manufacturers emphasize premium entertainment features to differentiate their offerings. Strategic collaborations between semiconductor companies and automotive OEMs are accelerating product innovation and adoption.

Challenges: Cost Pressures and Integration Complexity

Despite strong growth drivers, challenges include high design complexity, stringent automotive standards, and cost pressures across the semiconductor supply chain. The need for high reliability in harsh automotive environments adds further design challenges. Additionally, chip shortages and supply chain disruptions impact availability. However, increasing adoption of system-on-chip (SoC) designs, ongoing miniaturization, and integration of AI-based audio processing are expected to reduce these barriers.

Market Segmentation by Component

By component, the market is segmented into amplifier, DSP, microphone, and tuner. In 2024, amplifiers held the largest share due to widespread integration in premium audio systems. DSPs are witnessing rapid growth with rising demand for advanced sound processing, noise reduction, and voice recognition. Microphones are increasingly adopted in driver-assist features and hands-free systems, while tuners remain integral for radio and broadcast reception, especially in emerging markets.

Market Segmentation by Propulsion

By propulsion, the market is divided into gasoline, diesel, all-electric, hybrid electric vehicles (HEV), plug-in hybrid electric vehicles (PHEV), and fuel-cell electric vehicles (FCEV). Gasoline and diesel vehicles currently dominate due to large installed bases, but all-electric and hybrid vehicles are the fastest-growing segments, supported by strong EV adoption trends globally. PHEVs and FCEVs are emerging opportunities, particularly in regions with strong clean mobility policies.

Regional Insights

In 2024, Asia Pacific led the market, driven by rapid automotive production, EV adoption in China, and strong presence of semiconductor manufacturing hubs. Europe followed with significant demand for premium in-car infotainment and strict regulations driving electrification. North America showed steady growth, supported by demand for advanced connectivity and premium vehicle segments. Latin America and Middle East & Africa (MEA) are emerging markets, where affordability remains a challenge but rising car ownership and OEM investments are creating opportunities.

Competitive Landscape

The 2024 market featured strong competition among global semiconductor leaders. NXP, STMicroelectronics, Texas Instruments, and Infineon Technologies led with comprehensive automotive-grade semiconductor solutions. Analog Devices, Renesas Electronics, and Qualcomm expanded positions with innovations in DSPs and connectivity-driven solutions. Toshiba Electronic Devices, ROHM Semiconductor, and ON Semiconductor strengthened portfolios in power-efficient and application-specific audio semiconductors. Competitive differentiation is driven by performance, power efficiency, scalability, integration of AI capabilities, and close partnerships with automotive OEMs and Tier-1 suppliers.

Historical & Forecast Period

This study report represents analysis of each segment from 2023 to 2033 considering 2024 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2025 to 2033.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Automotive Audio Semiconductor market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2023-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Historical Year | 2023 |

| Unit | USD Million |

| Segmentation | |

Component

| |

Propulsion

| |

Application

| |

Vehicle

| |

Installation

| |

|

Region Segment (2023-2033; US$ Million)

|

Key questions answered in this report