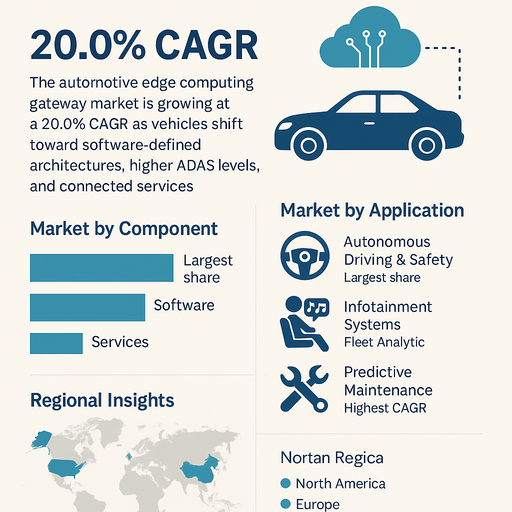

The automotive edge computing gateway market is growing at a 20.0% CAGR as vehicles shift toward software-defined architectures, higher ADAS levels, and connected services that require local processing of large data streams from sensors, ECUs, and cloud services. Edge gateways sit between in-vehicle networks and external connectivity, aggregating, filtering, and analyzing data close to its source to reduce latency, cut backhaul costs, and improve security. Within components, hardware currently generates the highest revenue because OEMs and Tier-1s are deploying dedicated gateway ECUs and domain controllers across new vehicle platforms, while software is expected to post the highest CAGR as value moves toward virtualization, containerized workloads, and analytics running on standardized hardware. By application, autonomous driving and safety systems together account for the largest revenue share today, whereas fleet analytics and predictive maintenance are expected to record the highest CAGR as commercial operators monetize data and optimize operations at scale.

Market Drivers

Market growth is driven by rising data volume from cameras, radar, lidar, V2X modules, and connected infotainment systems, which makes it inefficient to send all raw data directly to the cloud. Edge computing gateways enable local pre-processing, sensor fusion, and decision-making for ADAS, autonomous driving, and safety functions with millisecond-level latency requirements. OEMs are moving from distributed ECUs toward centralized and zonal architectures, where powerful gateways manage multiple domains and in-vehicle networks (CAN, LIN, FlexRay, Ethernet). The push for over-the-air updates, remote diagnostics, and cyber-secure connectivity also increases demand for gateways that can host security stacks, firewalls, and update managers. For fleets, telematics and edge analytics on fuel use, driver behavior, and component health support lower total cost of ownership and new service revenues, further supporting demand for edge-capable gateways.

Market Restraints

Adoption is limited by the complexity of integrating edge computing into legacy vehicle platforms and fragmented electronic architectures. Designing gateways that combine real-time control, functional safety, and IT-style compute and connectivity is challenging and can extend development cycles. OEMs face cost pressures and must ensure that added gateway hardware and software do not raise bill-of-materials beyond what can be recovered through higher vehicle prices or service revenues. Cybersecurity and safety regulations require extensive validation, secure boot, encryption, and patch management, raising engineering and maintenance costs. In addition, lack of unified standards for data models, APIs, and orchestration between in-vehicle edge and cloud platforms slows ecosystem development and can lock customers into proprietary stacks.

Market by Component

Hardware forms the backbone of the automotive edge computing gateway market today. High-performance gateway ECUs, domain controllers, and zonal controllers integrate multicore processors, accelerators, memory, automotive Ethernet, and multiple legacy network interfaces. Within components, hardware currently generates the highest revenue as every next-generation vehicle platform requires one or more such units to manage connectivity, data routing, and local processing. As architectures stabilize, software becomes the key differentiator, including operating systems, hypervisors, container runtimes, security frameworks, and application layer analytics. Software is expected to post the highest CAGR, driven by demand for flexible deployment of autonomous driving modules, predictive algorithms, and OTA-delivered features over a vehicle’s lifetime. Services, including system integration, software customization, cybersecurity consulting, remote monitoring, and lifecycle management, are growing steadily as OEMs and fleets need support to design and operate edge architectures, but they start from a smaller base than hardware and software.

Market by Application

Autonomous driving is a core application area, where edge gateways and central compute units process sensor data and run perception, localization, and decision algorithms in real time. Safety systems, including ADAS, collision avoidance, and emergency braking, also depend on low-latency edge processing and secure data paths. Together, autonomous driving and safety systems currently account for the highest revenue share among applications because they require the most powerful edge hardware and tightly integrated software stacks. Infotainment systems use gateways to manage content streaming, app ecosystems, user profiles, and connectivity to smartphones and cloud services, often sharing compute resources with other functions in a domain controller. Predictive maintenance uses edge analytics to monitor engine, drivetrain, battery, and chassis components, generating alerts before failures occur; along with fleet analytics, it is expected to record the highest CAGR as commercial fleets, logistics operators, and mobility service providers scale connected operations and rely on vehicle data for efficiency and uptime gains. The “Others” category includes insurance telematics, usage-based services, location-based offerings, and energy management in electric vehicles, which gradually expand as data-driven business models mature.

Regional Insights

Asia Pacific leads in volume as large vehicle production hubs in China, Japan, and South Korea adopt more connected and ADAS-equipped vehicles and benefit from strong local semiconductor and telecom ecosystems. North America shows strong growth driven by higher ADAS penetration, early autonomous driving pilots, and the presence of technology-driven OEMs and platform players that design vehicles around centralized compute and edge connectivity. Europe is a major market with focus on safety, emissions regulations, and premium vehicles, where complex electronic architectures and high levels of driver assistance drive demand for advanced gateways. Other regions, including Latin America and the Middle East, are at earlier stages but see growing adoption in higher-end models and in imported vehicles with advanced connectivity. Markets that move fastest toward software-defined vehicles, electrification, and commercial fleet digitization will show the highest growth in edge computing gateways.

Competitive Landscape

Bosch, Continental, and Denso are leading Tier-1 suppliers providing gateway ECUs, domain controllers, and software stacks that integrate in-vehicle networks, security, and OTA capabilities for global OEMs. NXP, Renesas Electronics, Infineon, STMicroelectronics, and Qualcomm supply the core processors, microcontrollers, and connectivity chipsets that power edge gateway platforms, focusing on automotive-grade performance, functional safety, and cybersecure designs. NVIDIA supplies high-performance compute platforms that combine GPUs and SoCs for autonomous driving and data-intensive edge workloads, often integrated into domain controllers that act as edge gateways. Huawei participates with in-vehicle connectivity, telematics, and edge computing solutions, particularly in markets where it partners closely with local OEMs and telecom operators. Companies that can provide scalable hardware platforms, robust software ecosystems, and strong security and update frameworks are positioned to lead current revenue, while those that enable flexible, over-the-air upgradable edge architectures for autonomous, electric, and fleet-intensive applications are likely to capture the highest CAGR in the automotive edge computing gateway market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Automotive Edge Computing Gateway market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Component

|

|

Application

|

|

Vehicle

|

|

Enterprise Size

|

|

Deployment Mode

|

|

|

Deployment Mode |

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report