The global market for automotive Silicon Carbide Market is expected to grow at a CAGR of 12.5 % during the forecast period of 2026 to 2034. Due to its ability to withstand extremely high temperatures, silicon carbide has an extended application across various application segments. Because of its high utility and one-of-a-kind properties, silicon carbide is witnessing increased revenues due to expanding worldwide demand for electric vehicles (EV). This demand is being driven by the rapid adoption of technologies that produce zero emissions. The global pandemic (Covid-19) and the subsequent shutdown of production activities had a direct impact on new order bookings, which ultimately led to the shortfall for the fiscal year 2021. The imposition of social distance, in conjunction with restrictions on movement, had an immediate and direct impact on the rate of productivity achieved by local manufacturers.

Increasing Demand for Electric Vehicle is the Key Motivating Factor

It is anticipated that the demand for silicon carbide would be driven by the growing adoption of technologies that produce zero emissions, which has led to an increase in the global demand for electric vehicles. As per The International Energy Agency (IEA), 2022 electric vehicle registrations climbed by 41% in 2021, and around 3 million electric vehicles were sold all over the world. The rapid adoption of electric vehicles, as opposed to fuel-based vehicles, can play an important role in achieving the goal of limiting the global temperature rise to 1.5 degrees Celsius above pre-industrial times, as decided by the United Nations in the Paris Agreement. This target was established in order to combat the effects of climate change (UN). Nevertheless, rising investments in the installation of electric vehicle charging stations are required to complement the widespread use of electric vehicles (EVs). There were around 300,000 sales of electric vehicles in 2021, which accounted for approximately 2% of the market for new automobiles in the United States, which is anticipated to grow at a rapid rate. The federal government of the United States has committed USD 15 billion toward the construction of 500,000 electric vehicle charging stations. In a similar vein, on April 10, 2021, the government of China-funded USD 1.42 billion to increase the number of charging stations for electric vehicles (EVs) around the country by a factor of fifty percent. When compared to silicon-based charging infrastructure, a silicon carbide charging infrastructure is able to produce greater voltages and a higher level of power. Silicon carbide is utilized in electric vehicle charging infrastructure. A SiC fast DC charging system has the ability to deliver 33% more power in 25% of the space, while also reducing losses by 50%. Silicon carbide MOSFETs, rather than silicon IGBTs, are employed in battery electric vehicles (BEVs) because they offer more robust conduction and switching loss performance, which results in a higher range for the vehicle. Because of this, engineers have been able to build power converters that are more compact and lighter as a result of the combination of smaller passive components and a decreased cooling system.

As a result of several steps being taken by the governments across countries such as Japan to enable the large-scale manufacture and rapid adoption of electric vehicles, a surge in sales has been observed. The percentage of new EV accounted for 36% in 2021from and 35% if 2019 in Japan. Since Toyota first began selling the Prius in Japan in 1997, there has been a considerable increase in the demand for hybrid electric vehicles (HEVs) on the Japanese market. In point of fact, hybrid electric vehicles (HEVs) accounted for 98% of all new electric vehicles sold in the year 2021. This was followed by plug-in hybrid electric vehicles (PHEVs), battery electric vehicles (BEVs), and fuel cell electric vehicles (FECVs). It is anticipated that this will boost the market for SiC MOSFETs, which will, in turn, drive revenue growth within the segment.

High Manufacturing and Processing Cost is Negating the Market Growth

Since silicon carbide does not exist as a naturally occurring mineral, it must be synthesized through the use of several furnace processes. SiC materials are made commercially under high-temperature conditions, and the resulting products are significantly more expensive than silicon. The decreased number of available fabrication facilities is just one of the many factors that contribute to the higher overall cost of device manufacturing for foundries. Doping in SiC is difficult to manufacture due to a number of factors, including its chemical inertness and its poor diffusion coefficient. The current production procedures result in numerous distinct kinds of material faults being produced in SiC substrates. Additionally, the availability of alternatives such as gallium nitride, which has similar properties such as the capability of sustaining high voltage, high frequency, similar bandwidth, and breakdown field, can restrain the growing demand for silicon carbide as a third-generation semiconductor material. These properties include the capability of sustaining high voltage, high frequency, similar bandwidth, and breakdown field. Since gallium nitride has higher electron mobility than silica carbide, it is more suited for use in high-frequency applications. It is anticipated that the growth of the market's revenue will be hampered by these factors.

Product Flaws are the Biggest Challenges that Companies are Seeking to Overcome

It is common to find micropipes, which are holes of a micrometer or smaller, dispersed throughout SiC materials, particularly crystals. SiC devices are subject to a variety of flaws throughout the manufacturing process of bigger wafers. These problems include stacking faults, dislocations, and prototype inclusions, among others. These flaws are brought about by a silicon and carbon precursor balance that is less than ideal, in addition to a local instability in either pressure or temperature. These faults have an effect on the efficiency of the device and cause a degradation in its electrical characteristics.

The SiC Discrete Accounted for the Largest Market Share

The global market for silicon carbide has been divided into three submarkets: SiC Discrete, SiC Bare Die, and SiC Module, each of which is based on the type of device. The SiC Discreteaccounted for the largest market share in 2022. SiC MOSFETs and SiC diodes are two more sub-segments that fall under the umbrella of the SiC discrete category. Small power applications, such as industrial power supplies and power supplies for high-power LEDs, are where discrete SiC MOSFET packages find the majority of their applications. Discrete packaging typically has a bigger cooling area than continuous packaging, which allows it to perform admirably even in environments with restricted cooling capacity. Schottky diodes made of silicon carbide (SiC) offer superior switching performance, in addition to higher power density, improved efficiency, and reduced system costs. These diodes are capable of reaching a significantly greater breakdown voltage, in addition to providing 0% reverse recoveries, a low forward voltage drop, current stability, high surge voltage capability, and a positive temperature co-efficient. In addition, they have a high surge voltage capability. The forward voltage of silicon carbide diodes produced by market companies such as STMicroelectronics N.V. ranges from 600 to 1,200 V, and these diodes include characteristics such as 0% reverse recoveries and improved forward voltage.

6-inch SiC Wafer to Dominate the Market

The global market for silicon carbide has been segmented into the 2-inch, 4-inch, and 6-inch wafer sizes, according to the size of the wafers. Because of factors such as the growing demand for electric vehicles (EVs) and the increasing preference for silicon carbide over silicon among original equipment manufacturers (OEMs) and auto manufacturers, the 6-inch segment is anticipated to account for the largest revenue share during the forecast period. When compared to their Si MOSFET counterparts, SiC MOSFETs offer superior performance, higher switching frequencies, and higher efficiencies. Maintaining the device's voltage rating while simultaneously reducing its thickness is made possible by a critical breakdown field with a larger critical value. In addition to this, because the bandgap is larger, it has a lower leakage of current. Because of this, market participants have increased the production of wafers based on silicon carbide for a diverse set of applications.

APAC Emerged as Global Leader

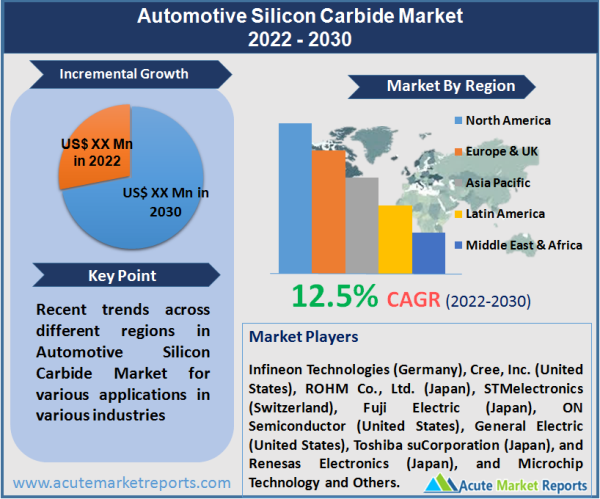

In terms of revenue, the Asia-Pacific region held the largest share of the global silicon carbide market in 2022. This region reported a market share of 55% in 2022, coming in ahead of Europe and North America, respectively. It is anticipated that the market in APAC will continue to have the greatest size throughout the forecast period. The most important markets for electric vehicles and hybrid electric vehicles in Asia are China, Japan, South Korea, and India. According to the study from the IEA outlook 2021, China was responsible for a share of 47% of the worldwide sales of electric buses in 2019. This greatly contributed to the growth of SiC market in APAC. It is anticipated that during the forecast period, the market will be further driven by the initiatives taken by many governments of APAC region to promote the use of electric cars.

Product Remains the Key Focus of Market Players

In order to increase their market share in the silicon carbide industry, prominent firms that have product launches and developments as the primary component of their business strategy. This has been followed by acquisitions, partnerships, collaborations, contracts, and agreements. Strategic collaborations such as M&A and JVs are enabling the companies to expand their product portfolio. Major companies operating in the silicon carbide market, include Infineon Technologies (Germany), Cree, Inc. (United States), ROHM Co., Ltd. (Japan), STMelectronics (Switzerland), Fuji Electric (Japan), ON Semiconductor (United States), General Electric (United States), Toshiba corporation (Japan), and Renesas Electronics (Japan), and Microchip Technology and Others.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Automotive Silicon Carbide market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Device Type

|

|

Wafer Size

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report