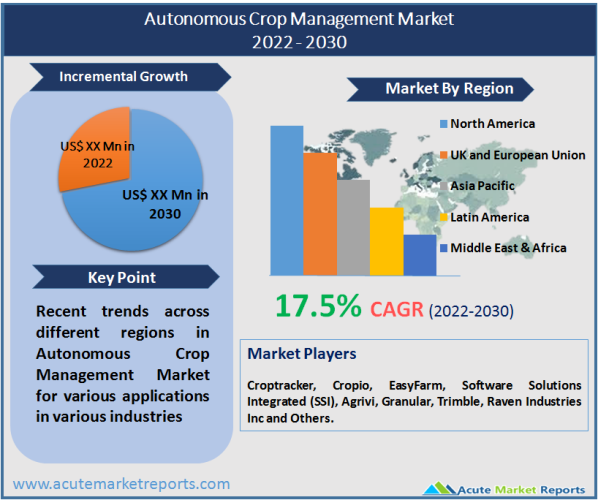

In 2022, the global market for autonomous crop management was valued at USD 1.45 billion and is projected to expand at a CAGR of 17.5% during the forecast period of 2026 and 2034. Farmers' increased awareness of benefits such as improved crop planning and tracking, labor cost reduction, and weather forecasting is driving the expansion of the industry. The expansion is also attributable to the expanding use of cloud computing for real-time crop data management and the growing global population, which has led to an increase in food demand. During the forecast period, it is anticipated that a greater emphasis by farmers on crop yield, productivity, and farm efficiency will spur economic expansion. It is anticipated that technological advances such as cloud computing and the Internet of Things (IoT) will encourage the use of big data, AI, and robots in agriculture. Utilizing big data analysis in autonomous crop management is essential for providing farmers with predictive insights, reengineering business processes, and making operational decisions in real-time to increase agricultural productivity.

Increasing Global Population to Boost the Market for Autonomous Crop Management Market

With a global population growth rate of over 1% per year, it will be difficult to meet the food demands of all these people in the coming years. Adopting the most advanced agricultural technology is one approach to addressing this problem. According to the Food and Agriculture Organization of the United Nations (FAO), 70% of global food production is expected to increase by 2050. Precision farming is the solution adopted in densely populated nations such as India and China to meet the rising demand for food. Artificial intelligence and machine learning have become more pervasive, allowing for real-time data access that simplifies data management tasks such as planning, purchasing, harvesting, feeding, marketing, and inventory control. Agricultural operations that collect data in real time facilitate analysis and decision-making.

Growth in Agro Tech Industry Favouring the Market Expansion

In the past few years, the agri-tech industry has experienced exponential growth worldwide. According to a report by Accel Partners and Omnivore, the sector's investments increased from $45.8 billion in 2015 to a staggering $430,6 billion by March 2021. The agri-tech industry has been expanding at a rate of 25% per year in India as well. Experts attribute this expansion to increased digitization, government initiatives, and rising investor interest. According to estimates, the agri-tech market in the United States will reach $24 billion by 2026. The software enables farmers to implement environmentally friendly agricultural practices, thereby reducing the use of water, fertilizers, and pesticides and ensuring food safety. In addition, modern agricultural practices would replace inefficient conventional agricultural methods, thereby assisting the agriculture sector in addressing sustainability concerns. This change is anticipated to have a positive impact on the autonomous crop management industry's growth over the forecast period. According to a study by Nasscom, India has over 450 agri-tech startups that have received over $248 million in funding. Notably, India is home to every ninth agri-tech startup in the world.

Software Segmented Dominates the Market by Solutions

In 2022, the software segment accounted for the largest revenue share, at 65%, and is anticipated to maintain its dominance over the forecast period. Based on professional and managed services, the service segment is subdivided. System integration & consulting and maintenance & support are the two types of professional services. The crop management software improves planning and tracking, reduces input and labor costs, and complies with regulatory standards.

The use of management software enables farmers to employ the most efficient and environmentally friendly farming methods. This modification enables farmers to produce safe food while using less water, fertilizer, and pesticides. The software assists farmers with crop rotation, soil management, harvesting times, and optimal planting times.

On-Premises Deployment Accounted for Over 50% of the Market

In 2022, the on-premises segment held the largest market share, at 55%. The segment of cloud-based autonomous crop management is expected to experience the highest CAGR during the forecast period. By focusing on storage devices, shared networks, and servers, cloud computing eliminates the high costs associated with maintaining software and hardware infrastructure. Cloud computing to monitor crop inputs and output in agriculture can contribute to climate change. In addition, the majority of businesses are adopting partnership strategies to improve cloud-based applications. In 2021, for instance, Trimble partnered with Ecobot, a software provider that offers cloud-based services to expedite environmental regulatory reporting. Through this agreement, the company's GNSS was integrated with Ecobot's Natural Resources Platform to enable rapid, sub-meter-accurate wetland delineation.

Crop tracking and Management Dominates the Market by Applications

Crop tracking and management accounted for 30% of total revenue in 2022 and is anticipated to maintain its dominance throughout the forecast period. This is also attributable to the increasing demand for crop growth monitoring and waste reduction through the timely delivery of essential water and minerals. Agriculture-type applications include crop tracking and management, weather tracking and forecasting, irrigation management, labor, and resource tracking, and others. From 2026 to 2034, the weather tracking and forecasting segment is anticipated to grow at the highest CAGR. Monitoring the weather can reduce expenses, prevent over- or under-watering, and increase crop yields. Predicting the weather aids in preventing the spread of pests and other crop diseases, as well as crop-destroying problems. The market has expanded due to the development of advanced data analytics services and machine learning techniques, which have enhanced the dependability and precision of weather forecasts. Increasing environmental awareness among consumers and growing water scarcity have necessitated the modification of agricultural management techniques that conserve natural resources, such as soil, air, and water, to boost the market growth. In addition, the segment of irrigation management is anticipated to expand significantly in the coming years.

North America Remains as the Global Leader

North America accounted for the largest revenue share of 38% in 2022, and its dominance is anticipated to continue in the years to come. North America is home to numerous technology companies that provide crop management solutions. Additionally, the region is regarded as an early adopter of technology. Increasing government initiatives to adopt modern agricultural technologies and developed infrastructure are the primary factors driving market expansion. For example, the North America Climate Smart Agriculture Alliance (NACSAA) was formed to educate and equip farmers for sustainable agricultural productivity. In addition, the high income and purchasing power of farmers in developed nations such as the United States and Canada is a major factor in the adoption of crop management solutions. Digital farming requires substantial investments, which is a disadvantage for farmers, particularly in developing nations such as India, China, and Brazil. Smart agriculture requires a relatively large capital investment, but it provides a significant return on investment by increasing crop productivity and enhancing crop resilience.

Moreover, the U.S. and UAE Agriculture Innovation Mission for Climate (AIM4C) program requires participating nations and businesses to make substantial investments in "climate-smart" agriculture over the next five years. The US $4 billion program will fund public and private agricultural research facilities and make them more accessible to farmers to encourage new scientific discoveries.

Asia-Pacific is projected to experience the highest CAGR between 2026 and 2034. The region is anticipated to experience significant growth over the projected period. Smart farming is in the adoption stage in the region, where an increase in government initiatives and a rise in cultivator awareness are the primary drivers of growth. For example, the Japanese agriculture ministry has funded the development of precision agriculture. Farmers' groups and community-based organizations in each nation are committed to advancing sustainable agriculture.

Acquisitions to Start on Market Consolidation

The companies use a variety of inorganic growth strategies, such as partnerships, regular mergers, and acquisitions, to expand their product offerings. CropX, a leading provider of soil and agricultural analytics, acquired CropMetrics to expand its presence in the American market. Using their extensive dealer network, service model, user-friendly platform, and Variable Rate Irrigation System, the purpose of this acquisition was to expand CropMetrics' product offerings throughout significant U.S. regions. Approximately 65% of the market's presence is held by crop monitoring and dairy farm management, the market's top segment leaders. As of 2022, other technologies, such as inventory management and harvesting and picking, represent approximately 35% of the market presence. Croptracker, Cropio, EasyFarm, Software Solutions Integrated (SSI), Agrivi, Granular, Trimble, and Raven Industries Inc. are key companies operating in the autonomous crop management market.

Recent developments in the market include the following:

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Autonomous Crop Management market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Solution

|

|

Deployment

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report