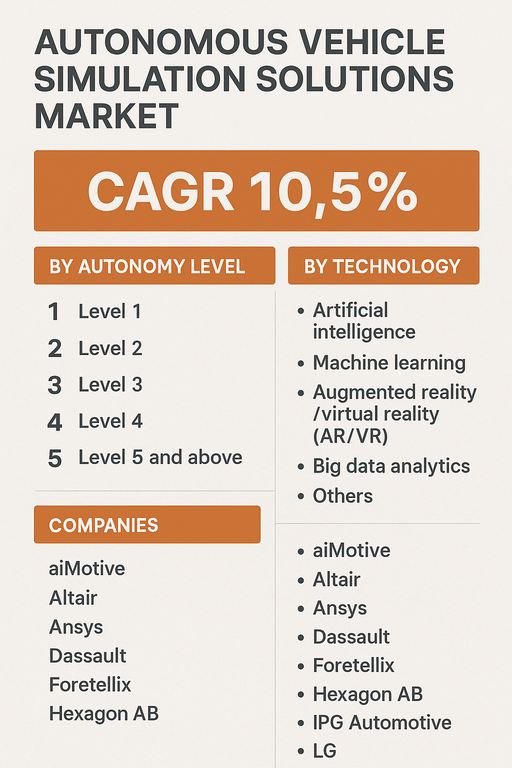

The global autonomous vehicle simulation solutions market is projected to grow at a CAGR of 10.5% from 2026 to 2034, driven by the increasing complexity of autonomous driving systems, growing need for safety validation, and accelerated development of software-defined vehicles. Simulation platforms enable automakers and technology providers to test, validate, and optimize autonomous driving algorithms in virtual environments that replicate real-world traffic scenarios, weather conditions, and edge cases significantly reducing the time, cost, and risk of on-road testing.

Increasing Demand for Scalable and Safe AV Testing Environments

As the automotive industry transitions toward higher levels of driving autonomy, the need for extensive validation through safe and scalable simulation has become critical. Autonomous driving stacks comprising sensor fusion, perception, localization, planning, and control modules must be tested against a wide array of traffic conditions, vehicle behaviors, and unexpected obstacles. Physical testing alone cannot address the billions of driving miles required to ensure safety compliance. Simulation solutions allow developers to test edge cases, iterate quickly, and integrate software updates into virtual vehicle environments ensuring accelerated and secure AV development lifecycles.

Adoption of AI, ML, and XR Technologies in AV Simulations

Advanced technologies such as artificial intelligence (AI), machine learning (ML), and augmented/virtual reality (AR/VR) are revolutionizing simulation environments. AI enables adaptive scenario generation, intelligent traffic modeling, and autonomous behavior prediction. Machine learning models are trained using simulated datasets, enhancing perception and decision-making algorithms in L2–L5 autonomy systems. AR/VR technologies provide immersive testing capabilities for human-machine interface (HMI) and driver behavior studies. Big data analytics plays a vital role in identifying system performance gaps, safety incidents, and environment-specific anomalies across large-scale test simulations. These technologies collectively improve realism, accuracy, and learning efficiency in AV validation processes.

Barriers in Data Standardization, Cost, and Integration

Despite robust growth, the AV simulation market faces challenges including lack of standardized testing protocols, high costs of simulation environments, and complexity in integrating simulations with physical testbeds. Ensuring cross-platform compatibility and interoperability between simulation tools, real-world sensor data, and vehicle control systems can be technically demanding. Additionally, building highly accurate 3D environments and digital twins of global road networks requires substantial resources and data availability. Regulatory bodies and industry alliances are working toward developing standardized test frameworks to support simulation-based AV safety certifications.

Market Segmentation by Autonomy Level

By autonomy level, the market is segmented into Level 1, Level 2, Level 3, Level 4, and Level 5 and above. In 2025, Level 2 and Level 3 systems dominated simulation investments as OEMs and tech firms focused on enhancing driver assistance and conditional automation features. These levels require intensive validation of handover scenarios, driver monitoring, and lane change behavior. Level 4 and Level 5 simulations are gaining traction in robotaxi, last-mile delivery, and urban mobility projects, where full automation is required in controlled environments. From 2026 onward, increased testing for higher autonomy levels is expected to drive demand for more sophisticated simulation frameworks.

Market Segmentation by Technology

By technology, the market includes Artificial Intelligence, Machine Learning, AR/VR, Big Data Analytics, and Others. Artificial intelligence held the largest share in 2025 due to its role in predictive modeling, scenario-based testing, and behavior analytics. Machine learning is widely used to train vision systems, adaptive cruise control, and planning algorithms. AR/VR-based simulations are instrumental in immersive training, HMI validation, and simulation of driver–vehicle interactions. Big data analytics supports the aggregation, correlation, and benchmarking of millions of simulated miles, enabling developers to fine-tune algorithms based on real-time feedback and comparative outcomes.

Regional Trends and Adoption

North America led the autonomous vehicle simulation solutions market in 2025, supported by robust R&D investments, favorable regulatory sandboxes, and the presence of autonomous driving innovators such as Waymo, Cruise, and Tesla. The region benefits from partnerships between simulation vendors and mobility providers. Europe followed, with countries like Germany, Sweden, and France investing in digital twin infrastructure and AV safety validation frameworks. Asia Pacific is anticipated to grow at the fastest CAGR from 2026 to 2034, driven by rapid AV deployment pilots in China, South Korea, and Japan. Public-private partnerships, tech adoption, and focus on smart city development are accelerating simulation uptake in the region. LATAM and MEA are in early adoption phases, with limited AV testing programs but growing interest in AV-related safety platforms.

Competitive Landscape

The 2025 market featured a mix of simulation software providers, digital engineering firms, and OEM tech collaborators. Ansys, Altair, and Dassault Systèmes offered multiphysics simulation platforms for AV system integration, crash testing, and sensor modeling. Hexagon AB, through VIRES and MSC Software, provided high-fidelity simulation environments and road data modeling. Siemens, with its Prescan and Simcenter platforms, supported end-to-end AV software validation. Mechanical Simulation, IPG Automotive, and Foretellix specialized in scenario-based testing and validation of AV perception and behavior. aiMotive and LG provided perception simulation and data-driven development tools. Competitive strategies revolve around enhancing realism, scenario coverage, interoperability with hardware-in-the-loop (HIL) and software-in-the-loop (SIL) systems, and expanding libraries of AV-ready test cases.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Autonomous Vehicle Simulation Solutions market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Component

|

|

Autonomy level

|

|

Technology

|

|

Vehicle

|

|

Deployment

|

|

Application

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report