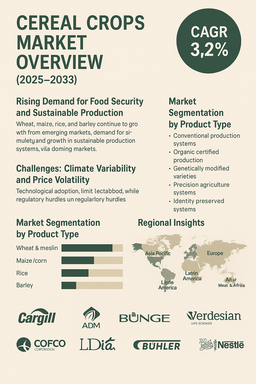

The global cereal crops market is projected to grow at a CAGR of 3.2% from 2026 to 2034, driven by rising global food demand, population growth, and the central role of cereals in ensuring food security. Wheat, maize, rice, and barley continue to serve as the primary staples for billions of people worldwide, forming the foundation of agricultural production systems. Increasing focus on sustainable farming practices, advancements in crop breeding technologies, and growing demand for organic and identity-preserved grains are reshaping the market.

Rising Demand for Food Security and Sustainable Production

Global food security challenges are fueling the expansion of cereal crops as governments and agricultural organizations prioritize stable, high-yield production. Wheat, maize, and rice dominate worldwide consumption, while barley plays a vital role in feed and brewing industries. Rising per capita consumption in developing countries, combined with food security initiatives and urbanization, is driving consistent demand growth. Simultaneously, sustainable production models such as organic farming and precision agriculture are witnessing strong adoption. These systems address consumer preferences for healthier, eco-friendly products while aligning with corporate and government sustainability targets, thereby generating opportunities for high-value certified cereal varieties.

Challenges: Climate Variability and Price Volatility

The cereal crops market faces challenges associated with climate change, including erratic rainfall, water scarcity, and soil degradation, all of which threaten yield stability. Price volatility is another pressing issue, as grain markets remain sensitive to geopolitical tensions, supply chain disruptions, and fluctuating input costs. Limited adoption of modern technologies in some regions constrains productivity, while regulatory complexities surrounding genetically modified crops hinder broader adoption. Moreover, consumer concerns about the safety and labeling of GM varieties impact acceptance in certain markets. Despite these obstacles, technological advancements in drought-resistant seed varieties, improved nutrient management, and risk-hedging mechanisms are expected to support long-term resilience and stable growth.

Market Segmentation by Product Type

By product type, wheat and meslin remain the most widely produced and consumed cereals, supported by their use in bread, flour, and processed food industries across global markets. Maize, or corn, holds a strong position given its dual role in human diets, animal feed, and industrial uses such as biofuels. Rice continues to dominate the Asia Pacific region, where it serves as the dietary foundation for billions and receives government support through subsidies and production programs. Barley, though smaller in scale compared to the other segments, maintains a steady role in brewing industries and livestock feed, with consistent demand in developed countries.

Market Segmentation by Production System

By production system, conventional farming practices continue to dominate global cereal output due to their established infrastructure and cost efficiency. However, organic certified production is witnessing the fastest growth, reflecting consumer preferences for chemical-free and sustainably farmed food products. Genetically modified varieties are gaining ground in key maize and soybean-producing regions, offering higher yields and improved resistance to pests and diseases. Precision agriculture is enabling farmers to optimize inputs, reduce waste, and improve profitability through data-driven cultivation practices. Identity-preserved systems are increasingly being adopted for premium export markets, ensuring traceability and meeting specific quality standards demanded by global buyers.

Regional Insights

In 2025, Asia Pacific led the global cereal crops market, primarily due to the dominance of rice cultivation in China, India, and Southeast Asia, coupled with the expanding production of maize and wheat. North America held the second-largest position, supported by large-scale maize and wheat production, high adoption of precision farming, and strong export markets. Europe maintained its competitive strength in wheat and barley production, further influenced by strict sustainability regulations and rising consumer demand for organic and identity-preserved grains. Latin America, particularly Brazil and Argentina, has been expanding its global footprint in maize and wheat exports, benefiting from fertile land and favorable climates. The Middle East and Africa remain emerging markets where population growth, urbanization, and government food security programs are increasing investments in modern agricultural practices, gradually improving their role in global supply chains.

Competitive Landscape

The competitive landscape of the cereal crops market in 2025 was dominated by global agribusiness leaders and seed innovators. Companies such as Cargill Inc., Archer Daniels Midland Company, Bunge Limited, COFCO Corporation, and Louis Dreyfus Company held significant influence due to their extensive trading, processing, and distribution capabilities. Verdesian Life Sciences has been driving advancements in nutrient efficiency, while Avani Seeds Ltd and Lidea are focusing on innovative seed varieties that enhance crop resilience. Buhler remains a leader in processing technologies that improve post-harvest handling and supply chain performance. Downstream players such as Nestlé and Agrovita Foods are shaping demand by integrating cereals into processed foods, packaged products, and consumer-focused innovations. The competitive differentiation across the market is increasingly defined by sustainability initiatives, digital agriculture platforms, advanced seed genetics, and integrated supply chain strategies that ensure efficiency and traceability.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Cereal Crops market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product Type

|

|

Production System

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report