The global cerebral palsy treatment market is projected to grow at a CAGR of 3.0% from 2026 to 2034. Growth is driven by rising awareness of neurological disorders, increasing access to rehabilitation and pharmaceutical therapies, and supportive government and non-profit initiatives focused on pediatric neurodevelopmental conditions. Cerebral palsy (CP), a group of permanent movement disorders caused by early brain development damage, is managed primarily through pharmacological treatments, rehabilitation, and supportive care. While no curative therapy exists, the expanding range of symptomatic treatments and novel therapeutic research is strengthening the market outlook.

Rising Focus on Symptomatic Management and Quality of Life

The demand for effective cerebral palsy treatment is being fueled by the growing prevalence of the condition worldwide, coupled with the need for improved patient quality of life. Pharmaceutical interventions, such as muscle relaxants and anticonvulsants, are widely used to manage spasticity, seizures, and movement disorders in CP patients. Increasing focus on multidisciplinary care models, combining pharmacological therapies with physiotherapy, occupational therapy, and speech therapy, is boosting treatment adoption. Furthermore, advancements in research on neuroprotective and regenerative therapies are expected to create long-term opportunities in the market.

Challenges: Limited Curative Options and High Treatment Costs

Despite the steady growth, the market faces challenges due to the absence of curative therapies for cerebral palsy. Current treatments remain primarily symptomatic, addressing complications rather than the root cause. High costs associated with long-term care and pharmaceutical therapies pose significant barriers, particularly in low- and middle-income countries. Additionally, variability in treatment effectiveness and side effects of long-term drug use, such as dependency and fatigue, limit adoption. Awareness gaps and limited access to advanced therapies in underdeveloped regions further restrict market penetration.

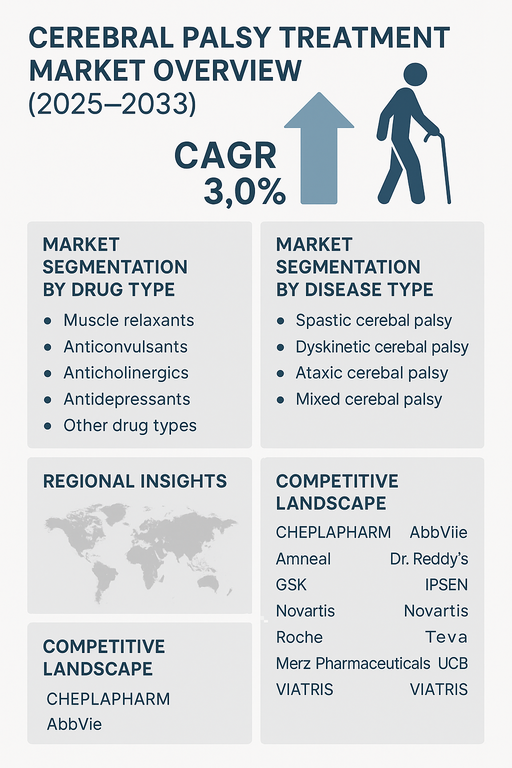

Market Segmentation by Drug Type

By drug type, the market is segmented into muscle relaxants, anticonvulsants, anticholinergics, antidepressants, and other drug classes. Muscle relaxants represent the largest share due to their widespread use in managing spasticity, a common symptom of CP. Anticonvulsants are also significant, addressing seizure-related complications in many CP patients. Anticholinergics and antidepressants, though smaller segments, support management of associated movement and mental health issues, while other drug types include adjunct therapies for specialized patient needs.

Market Segmentation by Disease Type

By disease type, the market is divided into spastic, dyskinetic, ataxic, and mixed cerebral palsy. Spastic cerebral palsy accounts for the largest share, as it is the most common form globally. Dyskinetic CP, characterized by involuntary movements, represents a smaller but critical segment due to the need for tailored pharmacological interventions. Ataxic CP, though rare, requires specialized treatments for balance and coordination issues. Mixed CP cases drive demand for multi-drug treatment approaches, highlighting the complexity of care in this market.

Regional Insights

In 2025, North America led the cerebral palsy treatment market, supported by advanced healthcare infrastructure, strong availability of pharmaceuticals, and active research initiatives. Europe followed, with high patient awareness and government-backed support programs in countries such as Germany, France, and the UK. Asia Pacific is expected to experience the fastest growth, driven by rising healthcare investments, increasing diagnosis rates, and expanding access to neurological care in China, India, and Japan. Latin America and the Middle East & Africa (MEA) are emerging markets where improving healthcare access, rising awareness campaigns, and international collaborations are gradually enhancing adoption.

Competitive Landscape

The 2025 market was shaped by a mix of global pharmaceutical leaders and specialized neurology-focused companies. AbbVie, IPSEN, and Merz Pharmaceuticals are key players in muscle relaxants and spasticity management. CHEPLAPHARM, Amneal, and Teva maintain strong portfolios in generic anticonvulsants and adjunct therapies. Dr. Reddy’s and VIATRIS are expanding access to affordable treatment options in emerging markets. Novartis, Roche, GSK, and UCB focus on broader neurology and CNS pipelines, contributing innovative therapies with potential CP applications. Competitive strategies center on drug portfolio expansion, partnerships with neurology research institutions, and patient-centric programs aimed at improving long-term outcomes.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Cerebral Palsy Treatment market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Drug Type

|

|

Disease Type

|

|

Route of Administration

|

|

Distribution Channel

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report