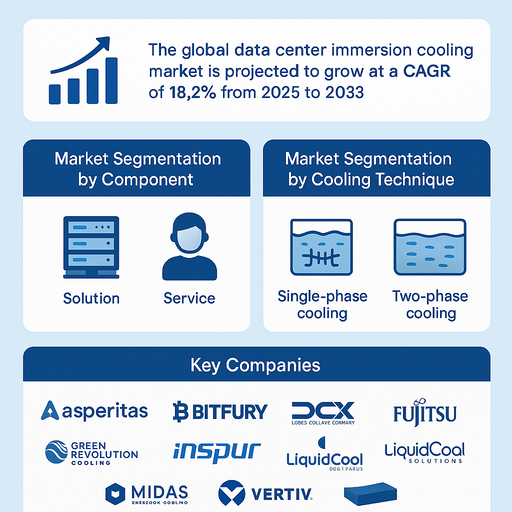

The global data center immersion cooling market is projected to expand at a robust CAGR of 18.2% from 2026 to 2034, driven by rising data center energy consumption, increasing rack density, and growing demand for efficient thermal management solutions. As traditional air-based cooling systems struggle to meet the needs of high-performance computing (HPC), artificial intelligence (AI), and edge deployments, immersion cooling is emerging as a viable alternative that offers lower energy use, reduced carbon emissions, and improved server lifespan. Key adoption drivers include rising sustainability mandates, cost-saving opportunities, and data center expansion across hyperscale and colocation facilities.

Market Drivers

Surge in High-Density Compute Applications

With exponential growth in AI/ML workloads, blockchain processing, and cloud computing, server heat density has surged beyond the effective threshold of conventional air cooling. Immersion cooling offers up to 95% heat removal efficiency by directly submerging hardware in thermally conductive dielectric fluids. This eliminates the need for fans, lowers power usage effectiveness (PUE), and enables compact server architectures. Hyperscale operators and enterprises running HPC workloads are increasingly shifting to single- or two-phase immersion solutions for sustained compute performance.

Environmental Sustainability and Energy Cost Optimization

Governments and data center operators are under pressure to meet carbon neutrality goals. Immersion cooling significantly reduces energy consumed by cooling infrastructure and water usage. With electricity costs forming a major share of total data center operating expenditure, immersion cooling provides long-term savings and contributes to meeting ESG benchmarks. Additionally, as data centers expand into hot climates and urban locations, immersion technology enables thermal stability without reliance on chilled water systems or mechanical chillers.

Market Restraint

High Upfront Costs and Integration Complexity

Despite its advantages, widespread adoption of immersion cooling faces challenges such as high capital investment, limited availability of immersion-ready server hardware, and retrofitting difficulties in existing facilities. The need for customized server enclosures, modified maintenance procedures, and fluid management expertise adds to the complexity. Many operators hesitate to shift from established air-cooled infrastructure due to the risks and downtime associated with operational transitions. Standardization and broader OEM support are still evolving, which may limit market penetration in cost-sensitive regions.

Market Segmentation by Component

By component, the market is segmented into Solution and Service. In 2025, the Solution segment dominated market share, comprising immersion cooling tanks, dielectric fluids, integrated racks, and compatible hardware systems. As more vendors develop modular and scalable cooling systems, solution offerings are being tailored to diverse workloads from AI inference to blockchain mining. The Service segment which includes installation, consulting, maintenance, and fluid monitoring is expected to grow significantly from 2026 to 2034, especially as enterprises seek specialized expertise for deployment, retrofitting, and optimizing cooling efficiency across hybrid environments.

Market Segmentation by Cooling Technique

Based on technique, the market is categorized into Single-Phase and Two-Phase Immersion Cooling. In 2025, Single-Phase Cooling led the market due to its simpler design, lower cost, and easier maintenance. It involves submerging IT equipment in a thermally conductive, non-boiling dielectric fluid that circulates through pumps and heat exchangers. Two-Phase Cooling, which uses low-boiling-point fluids that evaporate upon contact with heat and condense back in a closed-loop system, is expected to record the highest CAGR during 2026–2034. This method offers superior heat transfer efficiency, making it ideal for ultra-high-density compute clusters and edge deployments with space constraints.

Geographic Trends

North America held the largest share of the immersion cooling market in 2025, fueled by hyperscale expansion, energy efficiency regulations, and adoption by blockchain, AI, and government computing entities. The U.S. led deployments due to its concentration of cloud service providers and colocation facilities. Europe followed, with countries like Germany, the Netherlands, and Scandinavia advancing sustainability-driven adoption in response to energy-efficiency mandates and land use limitations. Asia Pacific is expected to post the highest CAGR from 2026 to 2034, driven by surging data center investments in China, India, and Southeast Asia. Edge infrastructure growth, smart city initiatives, and energy constraints are accelerating regional adoption. Latin America and the Middle East & Africa are also exploring immersion solutions, particularly in climate-challenged zones and areas with power scarcity.

Competitive Trends

The 2025 immersion cooling market was characterized by innovation from niche technology players, infrastructure firms, and OEMs. Companies like Asperitas, Submer, and Green Revolution Cooling led with purpose-built immersion systems for colocation and HPC applications. Vertiv and Fujitsu expanded their offerings through partnerships and thermal system integration. DCX Liquid Cooling Company and Midas Immersion Cooling focused on scalable modular units tailored for mid-sized data centers. Bitfury Group deployed immersion solutions extensively in crypto mining, influencing thermal management best practices. LiquidCool Solutions and Inspur addressed enterprise adoption through high-density compute compatibility and integrated server architectures. Key strategies included developing environmentally friendly dielectric fluids, launching standardized immersion-ready IT hardware, expanding global service networks, and forming OEM alliances to accelerate adoption in mainstream data center operations.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Data Center Immersion Cooling market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Component

|

|

Coolig Technique

|

|

Cooling Fluid

|

|

Organization Size

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report