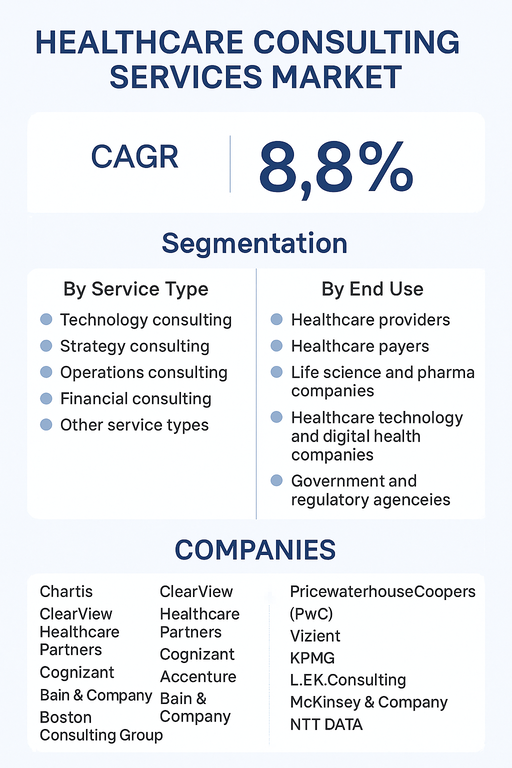

The global healthcare consulting services market is projected to grow at a CAGR of 8.8% from 2025 to 2033, driven by the rising complexity of healthcare systems, digital transformation initiatives, and the growing demand for value-based care models. Healthcare consulting services support providers, payers, and life sciences organizations in enhancing operational efficiency, improving patient outcomes, and navigating regulatory environments. With the shift toward integrated healthcare ecosystems, consulting services are becoming critical enablers for technology adoption, strategic planning, and financial sustainability across the sector.

Rising Demand for Digital Transformation and Strategic Expertise

The healthcare sector is rapidly adopting digital solutions such as electronic health records (EHRs), telehealth, AI-driven analytics, and cloud platforms. This digital shift creates strong demand for specialized consulting services to manage technology integration, cybersecurity, and compliance with privacy regulations. Additionally, the move toward value-based care and outcome-driven reimbursement models is encouraging healthcare organizations to seek strategy and operations consulting to redesign care delivery, optimize costs, and align with regulatory reforms. The focus on patient-centric and data-driven healthcare models further strengthens the market outlook.

Challenges: High Costs and Implementation Barriers

Despite robust growth, the market faces challenges related to the high costs of consulting services, which may be prohibitive for smaller providers and organizations in emerging markets. Implementation barriers such as legacy IT infrastructure, workforce resistance to change, and fragmented healthcare systems slow adoption of advanced strategies. Additionally, regulatory complexity across geographies often requires extensive customization, increasing project timelines and costs. Limited availability of skilled consultants in niche areas such as AI integration or precision medicine strategy also presents hurdles. However, increasing public-private partnerships, global standardization initiatives, and growing investment in digital health infrastructure are expected to mitigate these challenges.

Market Segmentation by Service Type

By service type, the market is segmented into technology consulting, strategy consulting, operations consulting, financial consulting, and other services. Technology consulting currently dominates due to rising demand for EHR modernization, cloud transformation, and AI-enabled solutions. Strategy consulting is gaining momentum as healthcare companies adapt to evolving reimbursement frameworks and competitive dynamics. Operations consulting supports efficiency improvements in hospital workflows, supply chains, and patient management, while financial consulting provides guidance on cost control, mergers & acquisitions, and revenue cycle optimization. Other services, including compliance and HR-related advisory, contribute to holistic market growth.

Market Segmentation by End Use

By end use, healthcare consulting services are utilized by healthcare providers, payers, life science and pharma companies, healthcare technology firms, and government agencies. Healthcare providers represent the largest segment, focusing on digital integration and operational efficiency. Payers increasingly rely on consulting to improve claims management, fraud detection, and patient engagement. Life sciences and pharma companies leverage consulting to navigate R&D strategies, clinical trials, and regulatory compliance. Digital health and technology firms are turning to consultants for market entry strategies, scalability, and interoperability support. Government and regulatory agencies seek consulting partnerships to strengthen public health programs and policy frameworks.

Regional Insights

In 2024, North America dominated the healthcare consulting services market due to advanced healthcare infrastructure, strong adoption of digital health solutions, and high consulting penetration among providers and payers. Europe followed, led by the UK, Germany, and France, where regulatory harmonization and healthcare innovation initiatives drive demand. Asia Pacific is expected to record the fastest growth, supported by healthcare digitization programs in China, India, and Japan, along with growing investments in hospital infrastructure. Latin America and Middle East & Africa (MEA) are emerging markets where rising healthcare expenditure, policy reforms, and expanding access to consulting services are unlocking new opportunities.

Competitive Landscape

The healthcare consulting services market in 2024 was highly competitive, with global consulting giants and specialized healthcare advisory firms shaping industry trends. McKinsey & Company, Boston Consulting Group (BCG), Bain & Company, and L.E.K. Consulting lead the strategy segment with strong healthcare vertical expertise. Deloitte, PwC, Ernst & Young, KPMG, and Accenture dominate technology and operations consulting, leveraging broad digital transformation portfolios. IQVIA, ClearView Healthcare Partners, and Chartis specialize in life sciences, clinical trials, and provider-focused advisory. Guidehouse, Huron, and Vizient strengthen their presence in provider operations and performance improvement. Companies like NTT DATA and Capgemini provide end-to-end digital healthcare solutions across global markets. Competitive differentiation is driven by deep industry specialization, advanced analytics capabilities, regulatory expertise, and digital transformation leadership.

Historical & Forecast Period

This study report represents analysis of each segment from 2023 to 2033 considering 2024 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2025 to 2033.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Healthcare Consulting Services market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2023-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Historical Year | 2023 |

| Unit | USD Million |

| Segmentation | |

Service Type

| |

End Use

| |

|

Region Segment (2023-2033; US$ Million)

|

Key questions answered in this report