Heat meters, also known as heat cost allocators, are devices used to measure and regulate the amount of heat energy consumed, typically in residential, commercial, or industrial setups. They play an integral role in district heating or cooling systems by ensuring accurate billing, monitoring consumption patterns, and promoting energy conservation. The global emphasis on energy efficiency, coupled with increasing urbanization, has fueled the growth of the heat meter market. Let's delve into the intricate factors driving this industry forward and explore a potential restraint. Heat meter marketis estimated to grow at a CAGR of 6.6% from 2026 to 2034, propelled by global energy efficiency movements, technological advancements, and the spread of district heating and cooling systems.

Escalating Demand for Energy Efficiency

Over the past few years, governments worldwide have instituted regulations promoting energy efficiency. For instance, the European Union's Energy Efficiency Directive mandates member countries to install heat meters in buildings to accurately bill consumers based on consumption. Such directives underscore the role of heat meters in achieving national energy-saving targets. The last decade has witnessed a surge in consumer awareness regarding energy conservation. Households and businesses, understanding the economic and environmental implications of wastage, have increasingly adopted heat meters to monitor and manage their consumption, leading to significant energy and cost savings.

Advancements in Heat Metering Technology

The integration of the Internet of Things (IoT) with heat meters has revolutionized the industry. Modern meters equipped with IoT capabilities allow real-time monitoring, predictive maintenance, and seamless data transfer to centralized systems. For example, residents in smart cities in Scandinavia have benefitted from IoT-enabled heat meters, experiencing reductions in energy bills due to real-time consumption insights. Recent advancements have improved the accuracy and lifespan of heat meters. Ultrasonic heat meters, for instance, have no moving parts, reducing wear and tear, and offering precise readings. Their adoption has been witnessed in various parts of Germany, where building codes prioritize accurate energy measurement.

Expansion of District Heating and Cooling Systems

Urbanization and Infrastructure Development: With rapid urbanization, especially in Asian countries like China and India, there's a growing demand for centralized heating and cooling systems. New infrastructure projects often incorporate district heating systems, necessitating the deployment of heat meters for efficient energy distribution and billing. District heating systems, when combined with heat meters, offer long-term cost advantages. For cities in Northern Europe, where district heating is prevalent, residents have observed consistent reductions in energy bills, attributing the savings to the effectiveness of heat meters in regulating consumption.

High Initial Installation Cost and Complexity

While heat meters promise long-term savings, their initial installation costs can be prohibitive for many. Setting up a comprehensive heat metering system in a building or district entails not just the cost of the meters themselves but also associated infrastructure like piping, valves, and control systems. The process of integrating heat meters, especially in older buildings or districts without pre-existing infrastructure, can be complex. In cities with aged architecture, such as Rome or Paris, retrofitting heat meters has presented challenges due to the intricacies of the building layouts and the need to preserve historical aesthetics.

Market Segmentation by Type

The Mechanical meters, with their traditional systems and proven reliability, commanded the lion's share of revenue. Established businesses and older infrastructures predominantly preferred them for their long-standing reputation and ease of integration into legacy systems. On the other hand, the Static meters, which utilize electronic or ultrasonic means for measurement, had the distinction of having the highest Compound Annual Growth Rate (CAGR). The allure of Static meters was their improved accuracy, lack of moving parts leading to reduced wear and tear, and adaptability with modern infrastructures. As residential and commercial spaces became more technologically integrated, the surge in Static meter adoption was observable, particularly in regions undergoing rapid urban development.

Market Segmentation by Connectivity

Segmenting the market by connectivity revealed a contrasting dynamic. Wired heat meters, being the traditional method of connectivity, brought in the highest revenue in 2025. Their reliability, paired with their extensive use in existing setups, solidified their dominant revenue position. Yet, the highest CAGR belonged to the Wireless heat meters. With the proliferation of smart homes and the integration of Internet of Things (IoT) devices, Wireless heat meters experienced significant adoption. Their easy installation, real-time monitoring capabilities, and elimination of cumbersome wiring made them particularly attractive for newer establishments and those seeking system upgrades.

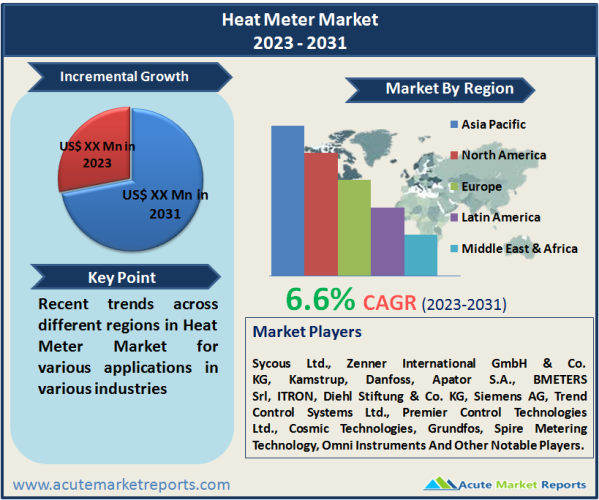

Asia Pacific will Lead the Market During Forecast Period

From a geographic standpoint, Europe took the lead in 2025 as the region generating the highest revenue percentage. This dominance can be credited to the region's strong inclination towards energy efficiency, established district heating systems, especially in Northern European countries, and stringent government regulations. However, the highest CAGR was observed in the Asia-Pacific region. With countries like China and India undergoing massive urbanization, infrastructure development, and a renewed focus on sustainable energy consumption, the demand for advanced heat meters skyrocketed. Predictions from 2026 to 2034 suggest that the Asia-Pacific region might further strengthen its position in the heat meter market, driven by its vast population, urban expansion, and government initiatives promoting energy efficiency.

Competitive Landscape

Reflecting on competitive trends, 2026 was rife with innovations and strategic moves by leading players in the heat meter industry, including Sycous Ltd., Zenner International GmbH & Co. KG, Kamstrup, Danfoss, Apator S.A., BMETERS Srl, ITRON, Diehl Stiftung & Co. KG, Siemens AG, Trend Control Systems Ltd., Premier Control Technologies Ltd., Cosmic Technologies, Grundfos, Spire Metering Technology, Omni Instruments. While Kamstrup focused on IoT integration, offering advanced metering solutions with real-time data monitoring, Diehl Stiftung & Co. KG and Danfoss emphasized enhancing meter accuracy and durability. These market leaders also engaged in partnerships, mergers, and acquisitions to consolidate their market positions and expand their geographic footprints. From 2026 to 2034, the competitive landscape is expected to intensify, with companies likely investing more in research and development, exploring sustainable materials for meter construction, and forging alliances to penetrate untapped markets.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Heat Meter market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Connectivity

|

|

End-Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report