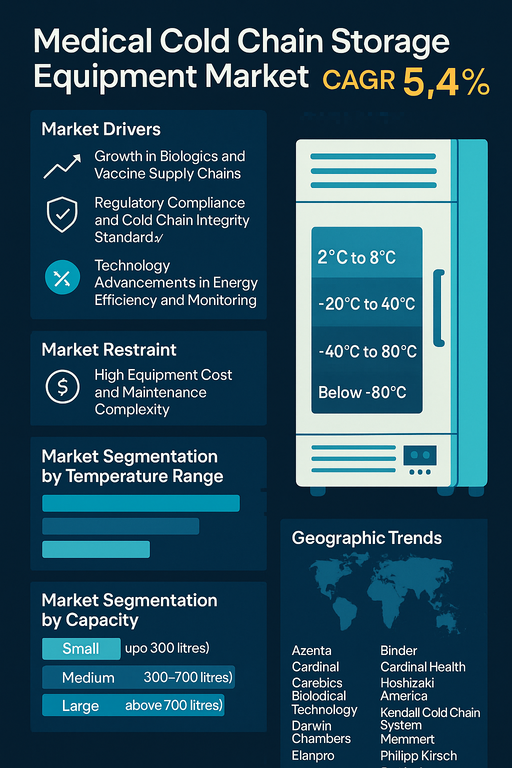

The medical cold chain storage equipment market is projected to grow at a CAGR of 5.4% from 2026 to 2034, fueled by rising demand for temperature-sensitive pharmaceuticals, biologics, and vaccines, along with stricter regulatory compliance related to medical product storage. The increasing adoption of mRNA-based therapies, cell and gene therapy products, and temperature-sensitive biologics necessitates advanced cold storage solutions that ensure product integrity throughout transportation and warehousing. Market dynamics are shaped by the integration of IoT-enabled monitoring, backup power systems, and eco-friendly refrigerants in cold storage infrastructure, which is helping to minimize risk and comply with global safety and sustainability norms.

Market Drivers

Growth in Biologics and Vaccine Supply Chains

The expanding production and global distribution of vaccines, monoclonal antibodies, and other biologics require cold chain systems with precise temperature control. Biopharmaceutical companies and healthcare logistics providers are investing in cold storage freezers and refrigerators that support a wide range of storage temperatures, from standard refrigeration to ultra-low temperatures. This trend is further strengthened by government immunization campaigns and preparedness for pandemic-like scenarios, which place emphasis on stockpiling and secure storage of temperature-sensitive products.

Regulatory Compliance and Cold Chain Integrity Standards

Regulatory agencies including the WHO, FDA, and EMA have imposed strict guidelines for maintaining consistent temperature profiles for storage and transport of pharmaceuticals. As a result, hospitals, labs, and manufacturers are upgrading to certified cold storage units that offer validated temperature control, real-time alerts, and GMP compliance. The need for audit readiness, reduced product wastage, and reliable chain-of-custody systems is creating sustained demand for high-performance cold chain equipment.

Technology Advancements in Energy Efficiency and Monitoring

Energy-efficient compressors, smart defrosting systems, and solar-powered backup mechanisms are becoming key differentiators in cold chain storage. Advanced cold storage units now incorporate digital interfaces, cloud-based monitoring systems, and predictive maintenance features that ensure uninterrupted operation and quality assurance. These innovations are especially critical for rural or remote healthcare sites, mobile vaccination programs, and biotech facilities requiring uninterrupted cold environments.

Market Restraint

High Equipment Cost and Maintenance Complexity

Initial investment in medical-grade cold chain storage equipment, particularly ultra-low temperature freezers (ULTs), can be prohibitively high. Costs related to unit acquisition, calibration, maintenance, and redundant power systems deter adoption among smaller clinics and rural health centers. Additionally, equipment requiring sub-80°C performance levels involves complex insulation, vapor sealing, and robust compressor technologies, which add to operational expenditure. These factors create affordability barriers, especially in low- and middle-income countries.

Market Segmentation by Temperature Range

By temperature range, the market is categorized into 2°C to 8°C, -20°C to -40°C, -40°C to -80°C, and Below -80°C. In 2025, the 2°C to 8°C segment held the highest revenue share due to its compatibility with routine vaccines, insulin, and other widely distributed pharmaceuticals. However, the -40°C to -80°C and Below -80°C categories are expected to register the fastest growth due to rising use of advanced biologics and genetic materials requiring ULT (ultra-low temperature) storage. These segments are particularly relevant in biotechnology R&D and vaccine cold storage facilities, where sample integrity at cryogenic temperatures is critical.

Market Segmentation by Capacity

Based on storage volume, the market is segmented into Small (up to 300 litres), Medium (300–700 litres), and Large (above 700 litres). The Medium capacity segment dominated the market in 2025, owing to its widespread use in hospitals, diagnostics labs, and research institutions with moderate inventory needs. Large capacity units are expected to witness significant growth in centralized storage hubs, pharmaceutical manufacturing facilities, and biobanks, driven by long-term inventory storage requirements and centralization of vaccine storage infrastructure. Small capacity equipment continues to serve the needs of clinics, mobile vaccination units, and on-site medical labs, especially in remote and resource-limited settings.

Geographic Trends

In 2025, North America led the medical cold chain storage equipment market in terms of revenue, backed by advanced healthcare infrastructure, pharmaceutical R&D intensity, and strong cold chain logistics in the U.S. and Canada. The region is expected to maintain steady growth through modernization of hospital storage units and vaccine stockpiling. However, Asia Pacific is projected to experience the highest CAGR from 2026 to 2034, supported by rapid healthcare expansion, vaccine rollout efforts, and biopharma investments in China, India, and Southeast Asia. Europe represents a mature market, with strong regulations and cold chain standardization across Germany, the UK, and France. Latin America and Middle East & Africa are emerging growth areas, particularly in Brazil, Mexico, South Africa, and the GCC nations, where healthcare infrastructure upgrades and public-private partnerships are enhancing cold chain reach.

Competitive Trends

The competitive landscape is shaped by manufacturers focusing on temperature precision, long-term reliability, and remote monitoring capabilities. In 2025, Haier Biomedical, Cardinal Health, and Philipp Kirsch led the market with wide product portfolios ranging from medical refrigerators to ultra-low temperature freezers with built-in data logging and alarm systems. Elanpro, Memmert, and Darwin Chambers focused on energy-efficient models for hospital and lab settings. Azenta, Hoshizaki America, and Carebios Biological Technology gained traction through specialized cold storage units for blood banks, vaccine centers, and biotech labs. Summit Appliances and Thalheimer Kuhlung strengthened their presence through cost-effective solutions for mid-tier users, while Kendall Cold Chain System, Farrar, and Roemer Industries focused on modular and transportable storage units. Through 2034, strategic collaborations with healthcare service providers, third-party logistics (3PL) firms, and vaccine manufacturers are expected to define competitive positioning.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Medical Cold Chain Storage Equipment market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Equipment Type

|

|

Temperature Range

|

|

Capacity

|

|

Technology

|

|

Application

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report