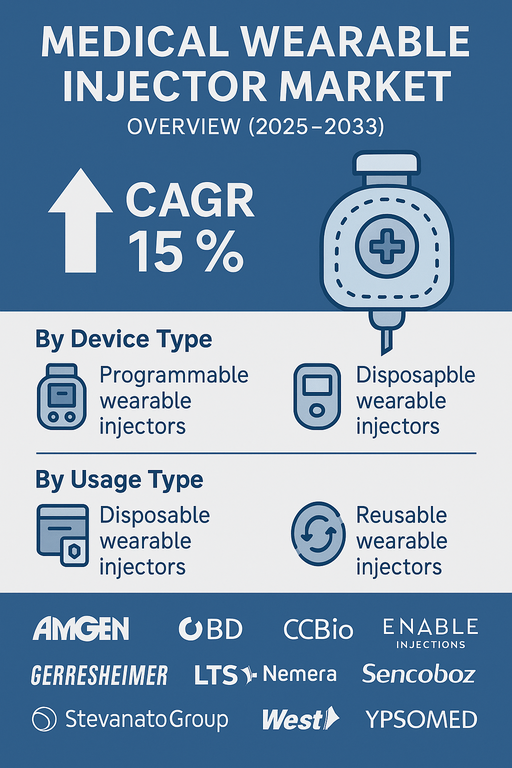

The global medical wearable injector market is projected to grow at a CAGR of 15% between 2025 and 2033. This growth is driven by the increasing adoption of self-administered therapies for chronic conditions, a shift toward home-based healthcare, and advancements in biologic drug delivery. Wearable injectors offer patients a more comfortable and convenient method of receiving large-volume subcutaneous injections without clinical supervision, thereby improving adherence, reducing hospital visits, and lowering healthcare costs. These devices are increasingly integrated into digital health ecosystems, offering monitoring, feedback, and enhanced user engagement.

Market Drivers

Rising Prevalence of Chronic Diseases and Demand for Home-Based Care

The growing incidence of chronic conditions such as diabetes, cancer, and autoimmune diseases is fueling the demand for patient-centric drug delivery solutions. Medical wearable injectors enable safe, accurate, and long-duration drug administration outside clinical settings. As healthcare systems seek to reduce inpatient loads and promote cost-effective models, wearable injectors are becoming essential tools in facilitating long-term treatments at home. They also align with healthcare payers’ priorities of improving outcomes and reducing hospitalization costs.

Advancements in Biologics and Drug Delivery Technologies

The increasing pipeline of biologics and large-molecule drugs typically requiring parenteral delivery has created a need for novel injection technologies. Wearable injectors are specifically designed to handle high-viscosity formulations and large volumes over extended durations. Improvements in device ergonomics, on-body adhesives, connectivity, and user feedback mechanisms are making these injectors more patient-friendly and reliable. Integration with mobile apps and digital platforms allows real-time monitoring and adherence tracking, enhancing treatment personalization.

Market Restraint

Cost and Regulatory Compliance Challenges

Despite strong growth potential, the market faces restraints in terms of high device development and manufacturing costs. Ensuring safety, sterility, and reliability in compact, body-worn systems involves complex engineering and rigorous validation. Regulatory approvals for combination products (drug + device) are lengthy and often fragmented across regions. In addition, concerns over skin reactions, device adhesion failure, and user errors may hinder adoption, especially in elderly or less tech-savvy patient populations.

Market Segmentation by Device Type

By device type, the market is segmented into Programmable Wearable Injectors and Non-Programmable Wearable Injectors. Programmable injectors dominated the market in 2024 due to their enhanced functionalities, including dosing control, delay timers, and electronic feedback systems. These devices are increasingly favored for complex therapies and clinical trials where precision and flexibility are critical. Non-programmable injectors, though more limited in features, offer a cost-effective solution for simpler drug delivery needs and are widely adopted in resource-constrained settings.

Market Segmentation by Usage Type

Based on usage, the market is segmented into Disposable Wearable Injectors and Reusable Wearable Injectors. In 2024, Disposable injectors held the largest market share due to their convenience, reduced risk of contamination, and ease of use. These are typically used in oncology and autoimmune treatments requiring intermittent, high-volume dosing. However, Reusable injectors are gaining traction, especially in chronic disease management programs, due to their long-term cost-effectiveness and sustainability benefits. This segment is expected to grow rapidly as manufacturers address usability and cleaning concerns.

Geographic Trends

In 2024, North America accounted for the largest share of the medical wearable injector market, supported by a high prevalence of chronic illnesses, strong reimbursement frameworks, and early adoption of patient-centric technologies. Europe followed, with rising biologic drug approvals and home-care initiatives in countries like Germany, France, and the UK. Asia Pacific is projected to witness the highest CAGR from 2025 to 2033, driven by increasing healthcare access, the growing elderly population, and government initiatives promoting self-administered treatments in China, Japan, and India. Latin America and Middle East & Africa are emerging markets where telehealth expansion and biologics market penetration are expected to drive gradual adoption.

Competitive Trends

In 2024, the medical wearable injector market was led by a combination of pharmaceutical giants, device developers, and contract manufacturers. Amgen remained a key player with its commercialized wearable injector platforms integrated into biologic therapy delivery. Becton Dickinson (BD) and West Pharmaceutical Services led in developing advanced wearable delivery systems for pharma clients. Enable Injections and Ypsomed offered customizable solutions for large-volume biologics, emphasizing patient comfort and digital integration. Stevanato Group, Gerresheimer, and Nemera focused on contract development and manufacturing services (CDMO) for pharma clients adopting on-body delivery formats. CCBio, LTS Lohmann Therapie-Systeme AG, Sencoboz, and others contributed innovation in adhesive systems, form factor miniaturization, and user-interface enhancements. Strategic priorities include platform modularity, connectivity integration, regulatory alignment, and lifecycle cost optimization.

Historical & Forecast Period

This study report represents analysis of each segment from 2023 to 2033 considering 2024 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2025 to 2033.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Medical Wearable Injector market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2023-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Historical Year | 2023 |

| Unit | USD Million |

| Segmentation | |

Device Type

| |

Usage Type

| |

Technology

| |

Application

| |

|

Region Segment (2023-2033; US$ Million)

|

Key questions answered in this report