The global next-generation batteries market is expected to witness significant revenue growth over the forecast period, with a CAGR of approximately 7% during the forecast period of 2026 to 2034. The next-generation batteries market has been experiencing rapid growth and innovation, driven by the increasing demand for high-capacity, long-lasting, and sustainable energy storage solutions. Next-generation batteries encompass a range of advanced technologies, including lithium-air, lithium-sulfur, solid-state, and flow batteries, among others. These batteries offer superior energy density, improved safety, and longer cycle life compared to traditional lithium-ion batteries, making them highly attractive for various applications. One of the key drivers behind this growth is the expanding market for electric vehicles (EVs). Next-generation batteries, such as lithium-sulfur and solid-state batteries, offer higher energy density, longer driving ranges, and reduced charging times compared to conventional lithium-ion batteries. These advancements are crucial in meeting the increasing demand for EVs and accelerating the transition toward sustainable transportation. Moreover, the renewable energy sector is also fueling the demand for next-generation batteries. The intermittent nature of renewable energy sources necessitates efficient and reliable energy storage solutions, and advanced batteries play a vital role in enabling the integration of renewable energy into the grid. The high energy density and long cycle life of next-generation batteries make them well-suited for renewable energy storage applications, ensuring a stable and sustainable power supply.

Increasing Demand for Electric Vehicles (EVs)

The rising demand for electric vehicles is a significant driver for the next-generation batteries market. EVs are gaining popularity as a cleaner and more sustainable alternative to traditional internal combustion engine vehicles. Next-generation batteries, with their higher energy density and longer driving ranges, are crucial for the widespread adoption of EVs. Governments worldwide are implementing stringent emission regulations and offering incentives to promote the adoption of electric vehicles. For instance, countries like China, the United States, and European nations have set ambitious targets for electric vehicle sales, creating a favorable environment for the growth of next-generation batteries. The increasing sales of electric vehicles support the need for advanced batteries. According to the International Energy Agency (IEA), global electric car sales reached over 3 million in 2021, representing a 43% increase compared to the previous year. This trend is expected to continue, driving the demand for next-generation batteries.

Growing Renewable Energy Integration

The integration of renewable energy sources into the grid presents a significant opportunity for next-generation batteries. As the world transitions towards cleaner energy systems, there is a need for efficient and reliable energy storage solutions to address the intermittent nature of renewable energy generation. The global capacity of renewable energy installations, such as solar and wind, has been steadily increasing. According to the Renewable Capacity Statistics 2022 report by the International Renewable Energy Agency (IREA), the total renewable energy capacity reached 2,799 GW by the end of 2021. This capacity expansion drives the demand for advanced energy storage systems, including next-generation batteries. Next-generation batteries offer high energy density, longer cycle life, and improved safety, making them well-suited for grid-scale energy storage applications. These batteries help stabilize the grid by storing excess renewable energy during periods of high generation and releasing it during peak demand, ensuring a reliable and stable power supply.

Technological Advancements and Research Efforts

Ongoing technological advancements and research efforts play a vital role in driving the growth of the next-generation batteries market. Companies and academic institutions are continuously exploring new materials, electrode architectures, and manufacturing processes to enhance battery performance and reduce costs. Collaborative research initiatives between academia, industry, and government bodies are accelerating advancements in next-generation battery technologies. These collaborations enable the exchange of knowledge, resources, and expertise, leading to breakthroughs in battery performance and reliability. The number of patent filings related to next-generation battery technologies is increasing, indicating active research and development efforts in the field. Patents provide evidence of innovative ideas and novel technologies being developed, which will ultimately contribute to the growth of the market.

Cost and Manufacturing Challenges

Despite the promising advancements in next-generation batteries, one significant restraint for the market is the cost and manufacturing challenges associated with these advanced battery technologies. Developing and manufacturing next-generation batteries involves complex processes, specialized materials, and advanced manufacturing techniques, which can drive up production costs. Next-generation batteries often require rare or expensive materials, such as lithium-sulfur batteries that use sulfur as a cathode material. Sulfur is abundant but requires additional processing steps to achieve the desired performance, increasing the overall cost of the batteries. Advanced battery technologies, such as solid-state batteries, often involve intricate manufacturing processes that require precise control over temperature, pressure, and material deposition. These complexities can lead to higher production costs, as specialized equipment and skilled labor are needed. Transitioning from lab-scale prototypes to large-scale production is a significant challenge for next-generation batteries. Scaling up production while maintaining performance, consistency, and reliability requires substantial investments in production facilities, equipment, and quality control measures. Next-generation battery technologies are still evolving, and there is a lack of standardized manufacturing processes and quality control protocols. This lack of standardization increases the complexity and costs of manufacturing, as manufacturers need to invest in research and development efforts to optimize their production processes.

Lithium-ion Battery Segment to Promise Significant Opportunities during the Forecast Period

Among the various types of next-generation batteries, the lithium-ion battery segment holds the highest revenue and exhibits the highest CAGR in the market during the forecast period of 2026 to 2034. Lithium-ion batteries have been widely adopted across numerous applications due to their superior energy density, longer cycle life, and high efficiency. They are extensively used in electric vehicles, consumer electronics, and energy storage systems. The increasing demand for electric vehicles and portable electronic devices is driving the growth of the lithium-ion battery market, resulting in substantial revenue generation. Additionally, advancements in lithium-ion battery technology, such as the development of solid-state lithium-ion batteries, are further propelling their market growth. On the other hand, while lithium-sulfur batteries and solid-state batteries hold promise for next-generation energy storage, they currently face challenges such as limited cycle life and manufacturing complexities. Despite these challenges, ongoing research and development efforts are focused on overcoming these limitations and improving their performance. As a result, lithium-sulfur and solid-state batteries are expected to experience significant growth in the coming years, contributing to the overall market expansion. Other types of next-generation batteries such as nickel-cadmium, magnesium-ion, ultra-capacitors, metal-air, and nickel metal hydride batteries also have their unique applications and advantages. However, their market growth and revenue potential are comparatively lower than lithium-ion batteries, mainly due to factors such as lower energy density, limited cycle life, or challenges related to manufacturing, safety, and cost-effectiveness. Nevertheless, ongoing research and technological advancements in these battery types may pave the way for future growth opportunities and broader market adoption.

Transportation Segment Leads the Revenues and Growth

The transportation segment held the highest revenue in 2025 and is expected to exhibit the highest CAGR during the forecast period of 2026 to 2034 in the next-generation batteries market. The increasing demand for electric vehicles (EVs) is a major driver for the growth of this segment. Next-generation batteries, particularly lithium-ion batteries, are extensively used in EVs due to their high energy density, longer driving ranges, and shorter charging times compared to conventional batteries. The transition towards sustainable transportation and the implementation of strict emission regulations worldwide are propelling the adoption of EVs, thereby driving the demand for next-generation batteries. Additionally, the energy storage segment is also witnessing significant growth, driven by the need for efficient energy storage systems in renewable energy integration and grid stability. Next-generation batteries, such as lithium-sulfur and solid-state batteries, are being increasingly utilized in renewable energy storage projects to store excess energy and release it during peak demand. Moreover, the consumer electronics segment has been a key end-use sector for next-generation batteries, driven by the demand for high-performance and long-lasting batteries in smartphones, laptops, tablets, and wearable devices. While the industrial segment encompasses various applications such as robotics, aerospace, and marine, it currently holds a lower market share compared to transportation, energy storage, and consumer electronics. However, ongoing advancements in battery technology and increasing applications in industrial sectors are expected to drive growth in the coming years. Other sectors, including medical devices, defense, and telecommunications, fall under the "Others" category and have their unique applications for next-generation batteries. Although they may not contribute significantly to the overall market revenue, they present niche opportunities for specialized battery solutions.

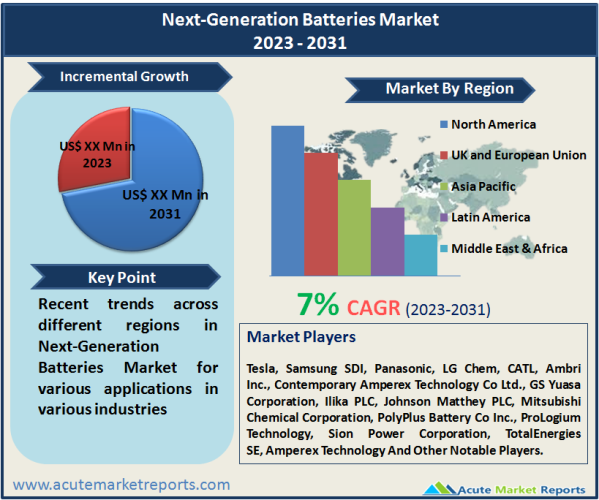

North America Remains as the Global Leader

North America held the highest revenue percentage in the market in 2025, primarily driven by factors such as the presence of major electric vehicle manufacturers, growing investments in renewable energy projects, and supportive government policies promoting clean energy initiatives. The region has witnessed significant advancements in battery technologies, with a focus on the development of solid-state batteries and lithium-sulfur batteries. On the other hand, the Asia Pacific region is expected to exhibit the highest CAGR during the forecast period of 2026 to 2034 in the next-generation batteries market. Factors contributing to this growth include the rapid expansion of the electric vehicle market, increasing renewable energy integration, and government initiatives to reduce greenhouse gas emissions. Countries like China, Japan, and South Korea are investing heavily in research and development, manufacturing capabilities, and infrastructure for next-generation batteries. China, in particular, has become a major hub for battery production and EV adoption, supported by favorablegovernment policies and incentives. Europe is also a significant market for next-generation batteries, driven by stringent emission regulations, the growing focus on clean energy, and the increasing adoption of electric vehicles. The European Union has set ambitious targets for EV market penetration, stimulating demand for advanced battery technologies. The region has seen collaborations between automakers, battery manufacturers, and research institutions to develop and commercialize next-generation batteries. Additionally, countries like Germany, Sweden, and the Netherlands have made significant investments in renewable energy storage projects, further boosting the demand for advanced energy storage solutions.

Market Competition to Intensify during the Forecast Period

The next-generation batteries market is fiercely competitive, with leading players such as Tesla, Samsung SDI, Panasonic, LG Chem, CATL, Ambri Inc., Contemporary Amperex Technology Co Ltd., GS Yuasa Corporation, Ilika PLC, Johnson Matthey PLC, Mitsubishi Chemical Corporation, PolyPlus Battery Co Inc., ProLogium Technology, Sion Power Corporation, TotalEnergies SE, Amperex Technology driving innovation and market growth. The market is characterized by intense research and development activities, strategic partnerships, and technological advancements aimed at improving battery performance, safety, and cost-effectiveness. Companies are heavily investing in R&D activities to develop new materials, improve battery performance, and overcome challenges related to energy density, cycle life, and manufacturing processes. Strategic partnerships with automakers, energy companies, and research institutions are common in the next-generation batteries market. These collaborations aim to leverage combined expertise and resources to accelerate the innovation and commercialization of advanced battery technologies. Key players are expanding their manufacturing capabilities to meet the growing demand for next-generation batteries. This involves establishing new production facilities and scaling up existing ones to achieve economies of scale and cost reductions. Companies are emphasizing the development of sustainable and safe battery technologies. This includes efforts to improve the recyclability of batteries, reduce reliance on rare or hazardous materials, and enhance safety features to prevent incidents such as thermal runaways.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Next-Generation Batteries market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report