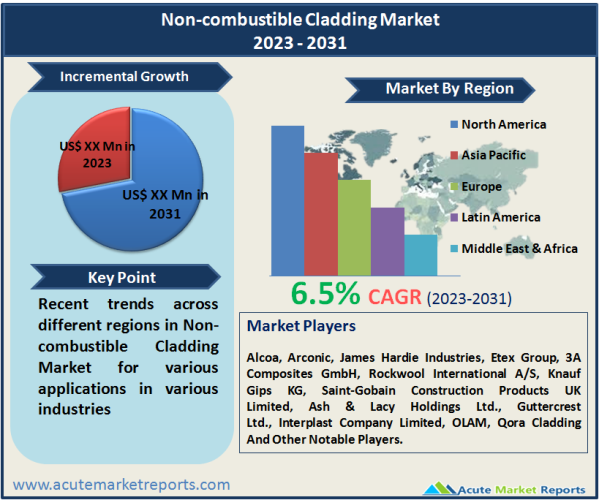

The non-combustible cladding market is expected to grow at a CAGR of 6.5% during the forecast period of 2026 to 2034. The non-combustible cladding market plays a pivotal role in enhancing building safety and reducing the risk of fire-related incidents in the construction industry. The non-combustible cladding market is driven by stringent safety regulations, urbanization, and a growing awareness of fire safety. However, cost constraints pose a significant challenge. Market segmentation by type and material provides a comprehensive view of the industry, and geographic trends vary across regions. Competitive players are actively engaged in innovation and partnerships to maintain their market position. Overall, the non-combustible cladding market is poised for growth as safety continues to be a top priority in construction.

Stringent Building Safety Regulations

One of the primary drivers stimulating the growth of the non-combustible cladding market is the implementation of stringent building safety regulations. Governments and regulatory bodies across the globe are increasingly emphasizing the need for fire-resistant building materials to ensure the safety of occupants and mitigate the risk of catastrophic fire incidents. For instance, after the tragic Grenfell Tower fire in London in 2017, numerous countries, including the United Kingdom, Australia, and the United States, revised their building codes and regulations to mandate the use of non-combustible cladding materials in high-rise buildings. These regulations require developers and builders to opt for A1 or A2 materials, which have the highest fire resistance ratings.

Rising Urbanization and Construction Activities

The rapid pace of urbanization, particularly in emerging economies, has led to a surge in construction activities. As more skyscrapers and high-rise buildings are erected, there is an increasing demand for non-combustible cladding materials to ensure the structural integrity and fire safety of these buildings. Countries like China and India have witnessed exponential growth in their construction sectors. These nations have adopted non-combustible cladding materials to meet safety standards and adhere to strict fire safety regulations. This trend is expected to continue as urbanization persists and more megacities emerge.

Growing Awareness of Fire Safety

Another crucial driver is the growing awareness among architects, builders, and property owners regarding the importance of fire safety in construction. The tragic consequences of fire incidents have prompted stakeholders to prioritize fire-resistant materials like non-combustible cladding. The increased focus on fire safety has led to a shift in consumer preferences toward materials with better fire-resistant properties. The demand for A1 and A2 materials has risen significantly as consumers recognize the need for materials that can withstand fire and prevent its rapid spread.

Cost Constraints

Despite the numerous advantages of non-combustible cladding materials, a significant restraint in their widespread adoption is the higher initial cost compared to combustible alternatives. A1 and A2 materials are often more expensive, which can deter some construction projects, especially those with tight budgets. Many construction projects, especially in the residential sector, face budget constraints. In such cases, builders and developers may opt for more budget-friendly alternatives, compromising on fire safety. This restraint highlights the need for market players to develop cost-effective non-combustible cladding solutions to address this challenge.

Market by Type: A1 Material Dominate in terms of Market Revenue

A1 materials represent a category of non-combustible cladding materials known for their exceptional fire resistance. They are designed to withstand high-temperature environments and are often used in buildings and structures where stringent fire safety regulations apply. In 2025, A1 materials recorded the highest revenue in the non-combustible cladding market, reflecting their critical role in fire-safe construction. Moreover, A1 materials are expected to maintain the highest CAGR) during the forecast period from 2026 to 2034. This growth can be attributed to the increasing emphasis on fire safety standards in the construction industry. A2 materials also offer a high level of fire resistance and are commonly used in construction projects where fire safety is a top priority. While A1 materials lead in revenue, A2 materials hold the second position in terms of revenue generation within the non-combustible cladding market in 2025. During the forecast period of 2026 to 2034, A2 materials are expected to experience a substantial CAGR, driven by the growing awareness of fire safety measures and their incorporation into building codes and regulations.

Market by Material: Aluminum Cladding Materials Dominate in terms of Market Revenue

Aluminum-based non-combustible cladding materials are favored for their lightweight properties and resistance to corrosion. In 2025, aluminum cladding materials generated substantial revenue within the non-combustible cladding market. The demand for aluminum cladding is expected to continue growing, contributing to a significant CAGR from 2026 to 2034. This growth can be attributed to their versatility and applicability in various building projects. Steel cladding materials, known for their exceptional strength and durability, found extensive use in industrial and commercial structures in 2025. Steel cladding materials are expected to maintain a steady CAGR from 2026 to 2034 due to their fire-resistant properties and suitability for projects where structural integrity is paramount. Concrete and brick cladding materials, appreciated for their superior fire resistance, were widely used in construction projects in 2025. While their revenue contribution was substantial, their CAGR from 2026 to 2034 is expected to be moderate. However, they remain a preferred choice in projects where both aesthetics and fire safety are essential. Fiber cement cladding materials offer a balance between fire resistance and design flexibility. In 2025, they contributed significantly to the non-combustible cladding market. Their CAGR during the forecast period of 2026 to 2034 is expected to be competitive due to their adaptability to various architectural styles and fire-resistant properties. This category encompasses various alternative non-combustible cladding materials that may include composite materials, specialty coatings, or innovative solutions. These materials cater to specific project requirements and are expected to experience varying revenue and CAGR trends within the non-combustible cladding market during the forecast period.

North America Remains as the Global Leader

Geographically, the market exhibits varying trends. In regions with a high level of urbanization and stringent building regulations, such as North America and Europe, there is a robust demand for non-combustible cladding materials. In contrast, emerging economies in Asia-Pacific are witnessing a growing adoption of these materials as urbanization and construction activities increase. North America, particularly the United States and Canada, has witnessed substantial growth in the non-combustible cladding market. The region's robust construction industry and stringent building codes emphasizing fire safety have propelled the demand for non-combustible cladding materials. Europe has a well-established market for non-combustible cladding materials, owing to strict fire safety regulations and a growing emphasis on sustainable construction practices. Countries like the United Kingdom, Germany, and France have been at the forefront of adopting non-combustible cladding solutions. The Asia-Pacific region is experiencing rapid urbanization and infrastructure development. Countries such as China, India, and Japan have witnessed a surge in construction projects. Non-combustible cladding materials are gaining popularity in this region due to their fire-resistant properties. China is poised to exhibit the highest CAGR in the Asia-Pacific region during the forecast period of 2026 to 2034. The Chinese government's focus on urban safety and stringent building codes have driven the adoption of non-combustible cladding materials in the country. The Middle East, particularly the United Arab Emirates, is anticipated to have the highest CAGR during the forecast period in the Rest of the World. The region's ambitious construction projects, such as high-rise buildings and mega-infrastructure, require robust fire safety measures, making non-combustible cladding materials essential.

Market Competition to Intensify during the Forecast Period

The non-combustible cladding market is highly competitive, with key players like Alcoa, Arconic, James Hardie Industries, Etex Group, 3A Composites GmbH, Rockwool International A/S, Knauf Gips KG, Saint-Gobain Construction Products UK Limited, Ash & Lacy Holdings Ltd., Guttercrest Ltd., Interplast Company Limited, OLAM, and Qora Cladding leading the industry. These companies are focusing on product innovation and strategic partnerships to gain a competitive edge. Key players in the non-combustible cladding market are continuously investing in research and development to introduce advanced and sustainable cladding materials. This includes developing cladding materials with enhanced fire-resistant properties, durability, and aesthetic appeal. Many companies in this market are forming strategic partnerships with architects, construction firms, and regulatory bodies. These collaborations aim to promote the use of non-combustible cladding in various construction projects, ensuring compliance with safety standards and regulations. Embracing digitalization and technology is a trend among leading companies. This involves using digital tools for design, simulation, and installation planning, enhancing efficiency, and reducing project lead times. Some players are opting for acquisitions to expand their market presence rapidly. By acquiring smaller cladding manufacturers or complementary businesses, they aim to strengthen their market position and gain access to new customer segments.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Non-combustible Cladding market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Material

|

|

Application

|

|

End-Use

|

|

Distribution Channel

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report