The percutaneous nephrolithotomy (PCNL) market is growing at a 6.6% CAGR as urology centers and hospitals manage rising volumes of complex kidney stones that cannot be treated effectively with extracorporeal shock wave lithotripsy (ESWL) or ureteroscopy alone. PCNL remains the mainstay procedure for large, staghorn, and hard stones, and is being refined through miniaturized access, improved visualization, and more efficient lithotripsy systems. Demand is supported by greater availability of hybrid operating rooms, higher imaging capability, and a growing burden of lifestyle-related stone disease in both developed and emerging markets.

Market Drivers

Growth is driven by increasing incidence of nephrolithiasis linked to aging populations, diabetes, obesity, and dietary patterns. As more patients present with larger or complex stones, PCNL is often preferred to achieve high stone-free rates in a single session. Improvements in imaging, including CT-based planning and intraoperative fluoroscopy and ultrasound guidance, support more precise access and safer procedures. Mini-PCNL and micro-PCNL techniques reduce tract size, shorten recovery, and expand the eligible patient pool, including those who may not tolerate standard PCNL. Hospitals and ambulatory centers are investing in dedicated PCNL towers, nephroscopes, and energy platforms to attract referrals and differentiate their urology service lines. In parallel, reimbursement recognition for complex stone procedures and training programs that promote minimally invasive stone surgery support broader adoption, especially in high-volume stone centers.

Market Restraints

The market faces restraints from the technical complexity of PCNL, limited access to trained urologists in some regions, and capital cost for advanced equipment. PCNL has a longer learning curve than ESWL or basic ureteroscopy, and complication risks such as bleeding, infection, and adjacent organ injury require structured training and infrastructure. Smaller hospitals may hesitate to invest in full PCNL suites, especially where case volumes are uncertain. In low- and middle-income markets, limited imaging and operating room capacity, as well as patient affordability, can delay adoption of advanced PCNL platforms. Competing technologies, including flexible ureteroscopy with high-power lasers and newer stone-dusting techniques, can be preferred for certain stone profiles, reducing PCNL share for smaller stones. Regulatory pressures on reusable devices and sterilization standards also add to operational complexity and cost.

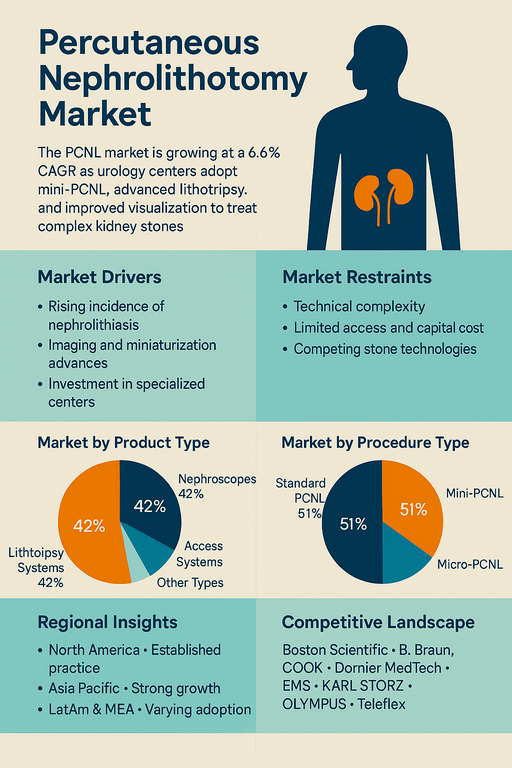

Market by Product Type

By product type, nephroscopes account for the highest revenue share in the percutaneous nephrolithotomy market because they are central to every PCNL procedure, are used across standard, mini-, and micro-PCNL techniques, and are purchased by both large hospitals and specialized stone centers, while lithotripsy systems are expected to post the highest CAGR as facilities upgrade to newer laser and ultrasonic lithotripsy platforms that improve stone fragmentation efficiency, shorten procedure time, and support miniaturized access; access systems, including dilators, sheaths, and guidewires, remain essential recurring-use products that grow in line with procedure volumes, and other product types such as visualization accessories, suction devices, and irrigation components contribute steady incremental revenue as centers standardize complete PCNL kits and system bundles.

Market by Procedure Type

By procedure type, standard PCNL still generates the highest revenue because it remains the reference approach for very large, complex, and staghorn calculi, is widely practiced in established urology centers, and uses a mature installed base of instruments and access systems, while mini-PCNL is expected to record the highest CAGR as urologists and patients favor smaller tract sizes, reduced blood loss, shorter hospital stays, and wider eligibility for minimally invasive treatment, and micro-PCNL, though starting from a smaller base, grows as a complementary niche for selected pediatric cases and smaller stones where ultra-miniaturized instrumentation can offer clinical and cosmetic advantages.

Regional Insights

North America and Europe represent key markets for PCNL devices, supported by well-established urology practices, high diagnostic rates of kidney stones, and strong adoption of minimally invasive techniques. Centers of excellence and teaching hospitals drive uptake of mini-PCNL and micro-PCNL, supporting demand for newer nephroscopes, lithotripsy energy sources, and access systems. Asia Pacific is expected to experience strong growth due to a high and rising stone burden in countries such as India and China, growing middle-class access to advanced urology care, and investment in tertiary hospitals and specialty stone centers. Latin America and the Middle East & Africa are at varying stages of adoption, with leading private and public hospitals investing in PCNL suites while smaller facilities still rely heavily on ESWL and ureteroscopy. Regions with expanding urology training programs, improving imaging and operating room infrastructure, and supportive reimbursement for complex stone procedures will see faster PCNL market expansion.

Competitive Landscape

ADVIN, ELMED, PolyDiagnost, and other specialized device makers supply nephroscopes, access systems, and complementary PCNL instruments tailored to different tract sizes and surgeon preferences. B. Braun, Becton, Dickinson and Company, Teleflex, and COOK MEDICAL offer a wide range of access, guidewire, catheter, and drainage solutions that are integrated into PCNL workflows across hospitals and ambulatory centers. Boston Scientific, Dornier MedTech, EMS Electro Medical Systems, and KARL STORZ play strong roles in lithotripsy and endourology platforms, providing energy sources, nephroscopes, and tower systems for comprehensive stone management. OLYMPUS and Richard Wolf are major endoscopy and imaging players, supplying nephroscopes, camera systems, and visualization solutions that support both standard and miniaturized PCNL approaches. Coloplast contributes drainage and stent products that are important for peri- and post-procedure management. As the market develops, companies that can bundle nephroscopes, lithotripsy systems, access instrumentation, and training into integrated PCNL solutions, and support the shift toward mini- and micro-PCNL with dedicated product lines, are likely to lead revenue, while those that innovate in imaging integration, single-use or hybrid scopes, and more efficient lithotripsy energy platforms are positioned to capture the highest CAGR in the percutaneous nephrolithotomy market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Percutaneous Nephrolithotomy market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product Type

|

|

Procedure Type

|

|

Patient

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report