The global personalized knee implants market is projected to grow at a CAGR of 6.0% from 2026 to 2034, supported by rising demand for customized orthopedic solutions, increasing prevalence of osteoarthritis, and advancements in 3D printing and patient-specific design technologies. Personalized knee implants are tailored to a patient’s unique anatomy, leading to improved alignment, better implant fit, reduced surgical complications, and enhanced postoperative outcomes. This market is gaining momentum as healthcare systems prioritize precision medicine and patient satisfaction in joint replacement procedures.

Rising Adoption of Customized Orthopedic Solutions

With growing awareness about implant longevity and functional outcomes, orthopedic surgeons and patients are increasingly favoring knee replacement systems that match individual anatomical and biomechanical needs. Personalized knee implants reduce the need for bone resection and intraoperative adjustments, minimizing surgical time and promoting faster recovery. These implants are especially beneficial for patients with unusual bone morphology, deformities, or prior implant failures. As elective procedures recover post-COVID and patient volumes rise, demand for tailored joint reconstruction options continues to expand.

Technological Innovations in Imaging, CAD, and 3D Printing

The market is being driven by innovation in preoperative planning, computer-aided design (CAD), and 3D manufacturing processes. Technologies such as MRI- and CT-based patient mapping, robotic-assisted surgery, and additive manufacturing are enabling production of highly accurate, patient-specific implants. These tools facilitate optimized implant sizing, better bone-implant contact, and enhanced joint stability. Furthermore, advancements in biocompatible materials and precision milling are improving durability and reducing the risk of wear-related failures, thereby increasing adoption across primary and complex procedures.

Challenges in Cost and Reimbursement Landscape

Despite clinical advantages, the high cost of personalized implants and limited reimbursement in some healthcare systems continue to pose challenges to market expansion. The lead time required for imaging, digital modeling, and production can also delay surgery scheduling. Additionally, access to personalized solutions remains limited in low- and middle-income countries due to resource constraints and lack of surgeon training in patient-specific planning platforms. However, as production becomes more scalable and digital workflows are streamlined, the cost gap between standard and personalized implants is expected to narrow.

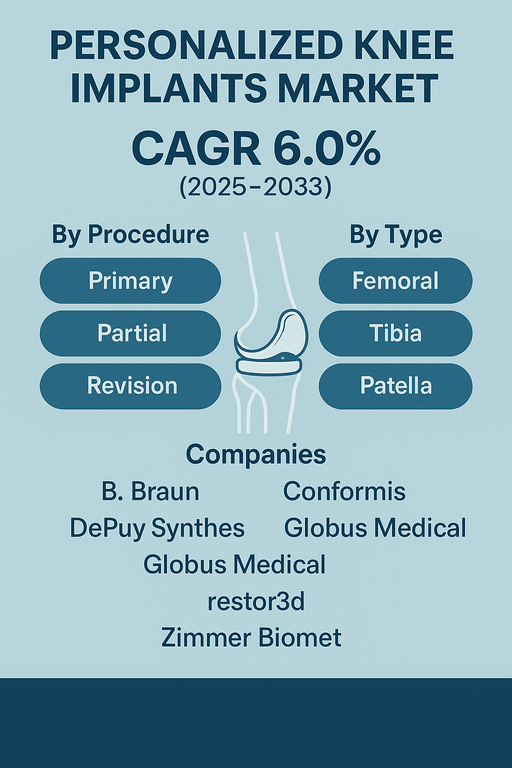

Market Segmentation by Procedure

By procedure, the market is segmented into primary, partial, and revision knee replacements. In 2025, primary knee procedures accounted for the largest market share due to the high volume of patients undergoing total knee replacement for end-stage osteoarthritis. Personalized implants in primary procedures improve implant longevity and patient satisfaction. Partial procedures, including unicompartmental knee replacements, are projected to grow at a significant rate, particularly among younger, active patients looking to preserve bone and avoid total replacement. Revision surgeries, although smaller in volume, represent a critical application segment where personalized implants can resolve issues of implant misfit and bone loss.

Market Segmentation by Type

By type, the market includes femoral, tibia, and patella components. Femoral implants held a dominant share in 2025 due to their critical role in articulation and load distribution. These components benefit significantly from patient-specific contouring for proper fit and alignment. Tibial components are also essential, particularly for cementless and modular fixation techniques. Patella implants, though used selectively, are gaining importance in improving anterior knee tracking and reducing post-surgical discomfort. Personalized patella resurfacing is increasingly integrated into comprehensive customized implant packages to improve surgical outcomes.

Regional Market Insights

North America led the personalized knee implants market in 2025, supported by advanced healthcare infrastructure, high adoption of 3D planning technologies, and the presence of major orthopedic device manufacturers. The U.S. is a key driver of innovation, supported by growing demand for same-day outpatient joint replacements. Europe followed, particularly in Germany, Switzerland, and the UK, where value-based care models and surgeon-led customization are gaining prominence. Asia Pacific is anticipated to register the fastest growth through 2034 due to rising orthopedic procedure volumes, expanding healthcare access, and government support for medtech innovation in countries like China, India, and Japan. Latin America and the Middle East & Africa are gradually emerging with demand driven by rising aging populations and medical tourism.

Competitive Landscape

The competitive landscape of the personalized knee implants market in 2025 included global orthopedic leaders and specialist companies offering customized solutions. Zimmer Biomet, DePuy Synthes (Johnson & Johnson), and B. Braun led the market with integrated digital platforms, preoperative planning software, and robotic-assisted capabilities. Conformis remained a pioneer in fully personalized total and partial knee implants using patient imaging and 3D printing. Medacta and Globus Medical focused on precision alignment technologies and anatomical implants designed for high-performance outcomes. Market players continue to invest in digital pre-surgical planning, surgeon education, and cloud-based imaging platforms to enhance customization, reduce procedural variability, and improve long-term implant performance.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Personalized Knee Implants market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Procedure

|

|

Type

|

|

Material

|

|

Fixation Material

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report