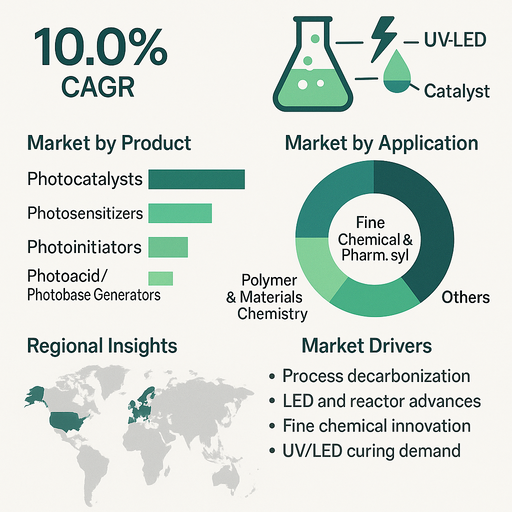

The photochemistry reagents for green synthesis market is growing at a 10.0% CAGR as chemical, pharmaceutical, and advanced materials companies adopt light-driven processes to cut energy use, improve selectivity, and reduce solvent and waste footprints. Light-activated catalysts, sensitizers, and initiators are being built into new synthesis routes, UV-LED curing systems, and photocatalytic treatment lines. Within products, photocatalysts currently generate the highest revenue because they are used in bulk for environmental remediation, coatings, and surface treatments, while photosensitizers are expected to post the highest CAGR as photoredox and visible-light organic synthesis scale up in fine chemicals and pharmaceuticals. By application, environmental remediation contributes the highest revenue today due to large photocatalyst volumes in water and air treatment, whereas fine chemical and pharmaceutical synthesis is expected to record the highest CAGR as more batch and flow processes are redesigned around green photochemical routes.

Market Drivers

Growth is driven by regulatory and corporate pressure to decarbonize chemical processes and reduce hazardous reagents and byproducts. Photochemical routes often operate at lower temperatures and use milder conditions, which helps lower energy consumption and improve safety. Advances in LED sources, reactor design, and photocatalyst engineering make it easier to scale lab protocols into industrial processes. In fine chemicals and pharmaceuticals, visible-light photoredox methods enable new bond-forming reactions, late-stage functionalization, and cleaner oxidation or reduction steps, which supports both innovation and process intensification. In polymers and coatings, UV and LED curing use photoinitiators to achieve fast, low-temperature crosslinking with low volatile organic compounds (VOC), which fits with stricter environmental norms. Environmental remediation applications benefit from photocatalysts that degrade organic pollutants, dyes, and other contaminants without adding secondary chemicals, aligning with circular water and air management strategies.

Market Restraints

Adoption is constrained by the complexity of scaling photochemical processes from lab to plant, including light penetration limits, reactor design, and uniform irradiation in larger volumes. Many legacy plants are not designed for photochemical equipment, so retrofitting or new builds can require significant capital. Some photocatalysts and photosensitizers rely on rare or expensive metals, which raises material cost and raises sustainability questions of their own. Deactivation, fouling, or leaching of catalysts in continuous processes can affect long-term economics and require regeneration strategies. In fine chemicals and pharmaceuticals, process validation, regulatory approvals, and detailed impurity control slow the replacement of established synthetic routes, even when photochemical options look attractive on paper. For some applications, lack of experienced process engineers and standardized reactor solutions further delays wider industrial adoption.

Market by Product

Photocatalysts are used to drive reactions under UV or visible light without being consumed, commonly based on metal oxides such as TiO₂ and other semiconductor materials. They are widely deployed in environmental remediation, self-cleaning coatings, and selected synthetic steps; within products, photocatalysts currently generate the highest revenue due to high-volume use in water and air treatment, coatings, and building materials. Photosensitizers absorb light and transfer energy or electrons to substrates or catalysts, enabling visible-light reactions in organic synthesis and specialty chemistry. As photoredox catalysis gains ground in fine chemical and pharmaceutical routes, photosensitizers are expected to post the highest CAGR, driven by demand for high-selectivity transformations and compatibility with LED light sources. Photoinitiators and photoacid/photobase generators are essential in polymer and materials chemistry, initiating or catalyzing polymerization and crosslinking upon irradiation. They are used in UV/LED-curable coatings, inks, adhesives, and 3D printing resins and show steady growth as industries switch from thermal to light-based curing to cut energy use and meet VOC and curing-speed targets.

Market by Application

Environmental remediation uses photocatalysts in reactors and surface treatments to break down organic pollutants in wastewater, industrial effluents, and air streams. Applications include treatment plants, advanced oxidation processes, photocatalytic tiles, and coatings for indoor air quality. This segment currently contributes the highest revenue as large volumes of photocatalyst are consumed or embedded in environmental systems. Fine chemical and pharmaceutical synthesis uses photocatalysts, photosensitizers, and photoinitiators for selective transformations, oxidative and reductive steps, and innovative bond constructions in APIs, intermediates, and specialty chemicals. As companies redesign routes to minimize waste, avoid heavy metals or harsh oxidants, and enable continuous flow, this segment is expected to record the highest CAGR. Polymer and materials chemistry relies on photoinitiators and photoacid/photobase generators for UV and LED curing of coatings, inks, electronics materials, and 3D printing resins, combining faster curing, lower bake temperatures, and better control over film properties. The “Others” category includes academic and pilot-scale research, agrochemicals, fragrance and flavor synthesis, and emerging photochemical processes in areas like energy storage, where green synthesis and functional materials development are converging.

Regional Insights

Europe and North America lead adoption of photochemistry reagents for green synthesis due to strong environmental regulation, high energy costs, and advanced fine chemical, pharmaceutical, and coatings industries. These regions invest heavily in R&D and pilot plants that demonstrate photochemical routes, and they act as early adopters of UV/LED curing in industrial coatings, printing, and electronics. Asia Pacific is expected to show strong growth as chemical hubs in China, India, Japan, and South Korea expand capacity for specialty chemicals, pharmaceuticals, and advanced materials and seek greener processes to comply with tightening emission standards and improve export competitiveness. In emerging markets, environmental remediation projects and water treatment upgrades create opportunities for photocatalyst suppliers. Regions with strong regulatory drivers, technical expertise, and access to renewable or low-carbon electricity will be best positioned to scale photochemical processes at industrial level.

Competitive Landscape

BASF SE, Huntsman Corporation, and Corning Incorporated participate in the market by supplying functional materials, specialty chemicals, and reactor or glass technologies that support photochemical processes in fine chemicals, polymers, and environmental systems. Chemours, Kronos Worldwide, Lomon Billions Group, Tayca Corporation, Tronox, Venator Materials, and Ishihara Sangyo Kaisha are major producers of titanium dioxide and related inorganic pigments, several of which are engineered or adapted as photocatalysts for environmental remediation, self-cleaning coatings, and functional surfaces. These companies leverage large-scale oxide production, surface treatment expertise, and application labs to develop photocatalyst grades suited to specific light sources and reactor conditions. Suppliers that can offer consistent-quality photocatalysts and photosensitizers, support customers with reactor and process design, and demonstrate strong performance in real industrial environments are positioned to lead current revenue, while those that co-develop photochemical routes for pharmaceuticals, specialty chemicals, and advanced materials are likely to capture the highest CAGR within the photochemistry reagents for green synthesis market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Photochemistry Reagents for Green Synthesis market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report