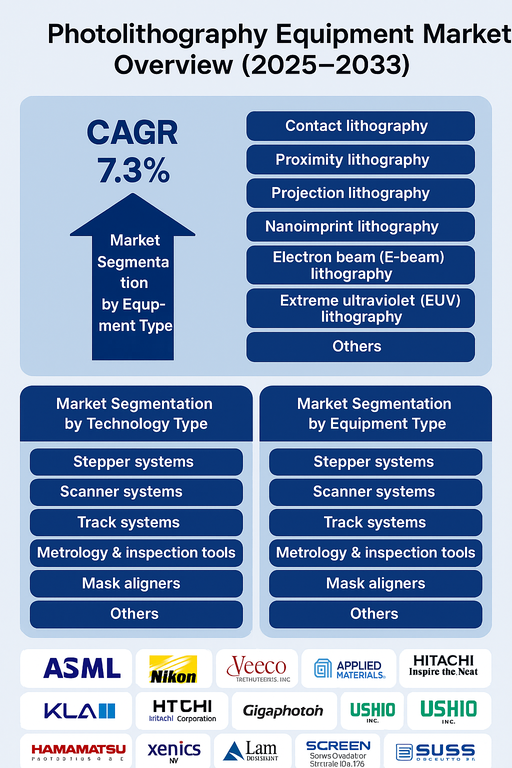

The global photolithography equipment market is projected to expand at a CAGR of 7.3% from 2026 to 2034, driven by the rapid growth of the semiconductor industry, rising demand for advanced integrated circuits (ICs), and increasing adoption of next-generation lithography technologies. Photolithography is a critical process in semiconductor manufacturing, enabling the precise transfer of circuit patterns onto silicon wafers. With growing demand for smaller, faster, and more energy-efficient chips, equipment manufacturers are investing in advanced technologies such as extreme ultraviolet (EUV) lithography and electron beam lithography.

Semiconductor Miniaturization and Technological Advancements Fueling Growth

The ongoing drive toward miniaturization in semiconductors, propelled by applications in AI, 5G, autonomous vehicles, and IoT, is a key growth driver for photolithography equipment. EUV lithography systems, in particular, are gaining traction for enabling nodes below 7nm, supporting advanced logic and memory chip production. Additionally, innovations in mask aligners, metrology tools, and scanner systems are enhancing precision and throughput. Governments and private companies are investing heavily in domestic semiconductor capabilities, further boosting demand for high-performance lithography equipment.

High Cost and Operational Complexity Remain Challenges

Despite strong growth, the adoption of advanced photolithography equipment is limited by high costs and technical complexity. EUV lithography systems are among the most expensive semiconductor tools, requiring significant capital investments and specialized infrastructure. Operational challenges such as mask defects, light source stability, and contamination control also pose risks. Moreover, smaller semiconductor manufacturers often struggle with the affordability of cutting-edge lithography equipment. However, ongoing R&D, government subsidies, and growing demand for advanced chips are expected to mitigate these barriers.

Market Segmentation by Technology Type

The market is segmented into contact lithography, proximity lithography, projection lithography, nanoimprint lithography, electron beam (E-beam) lithography, extreme ultraviolet (EUV) lithography, and others. In 2025, projection lithography held the largest share due to its widespread use in mainstream semiconductor manufacturing. EUV lithography is the fastest-growing segment, driven by demand for advanced nodes in logic and memory. E-beam lithography remains important in R&D and mask-making applications, while nanoimprint lithography is gaining traction for niche applications in nanotechnology and photonics.

Market Segmentation by Equipment Type

By equipment type, the market is divided into stepper systems, scanner systems, track systems, metrology & inspection tools, mask aligners, and others. In 2025, scanner systems dominated due to their high throughput and precision in high-volume manufacturing. Stepper systems remain widely used in legacy semiconductor production. Metrology and inspection tools are witnessing strong growth due to increasing demand for defect detection and process control. Mask aligners continue to play a role in research, specialty devices, and low-volume production.

Regional Insights

In 2025, Asia Pacific dominated the photolithography equipment market, led by semiconductor hubs in Taiwan, South Korea, Japan, and China, where companies such as TSMC, Samsung, and SMIC are investing in capacity expansion. North America followed, with strong demand from U.S. semiconductor manufacturers supported by initiatives like the CHIPS Act. Europe also maintained a significant share, primarily due to ASML Holding N.V., the global leader in EUV lithography, and growing investments in semiconductor supply chain resilience. Latin America and Middle East & Africa are emerging regions with limited but growing demand, primarily driven by electronics assembly and government-backed industrial development programs.

Competitive Landscape

The market in 2025 was dominated by a few global players with strong technological leadership. ASML Holding N.V. led the EUV lithography segment with a near-monopoly position. Nikon Corporation and Canon Inc. remained significant in legacy and optical lithography solutions. KLA Corporation, Onto Innovation Inc., and Hitachi High-Tech Corporation specialized in metrology and inspection tools. Applied Materials, Lam Research, and SCREEN Semiconductor Solutions supported lithography through complementary process equipment and track systems. SUSS MicroTec SE and EV Group (EVG) provided leading-edge mask aligners and nanoimprint lithography systems. Light source providers such as Gigaphoton Inc., Cymer LLC, Ushio Inc., and Hamamatsu Photonics K.K. played key roles in enabling advanced lithography. Veeco Instruments Inc. and Xenics NV contributed niche solutions in inspection, imaging, and process enhancement. Competitive differentiation is driven by resolution capability, throughput, equipment stability, and ability to support advanced semiconductor nodes.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Photolithography Equipment market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Technology Type

|

|

Equipment Type

|

|

Light Source

|

|

Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report