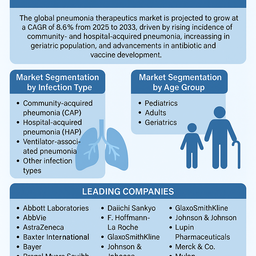

The global pneumonia therapeutics market is projected to grow at a CAGR of 8.6% from 2026 to 2034, driven by the increasing incidence of community- and hospital-acquired pneumonia, rising geriatric population, and advancements in antibiotic formulations and vaccines. Pneumonia continues to be a major cause of morbidity and mortality, especially among children under five and elderly populations. The rising prevalence of drug-resistant bacterial strains and greater awareness of early diagnosis and treatment are further boosting therapeutic demand.

Growing Incidence and Advancements in Treatment

The market is expanding as healthcare systems worldwide intensify efforts to combat respiratory infections through improved vaccination coverage, faster diagnostics, and next-generation antibiotics. Rising healthcare expenditure, particularly in developing nations, and increased access to advanced care facilities have fueled demand for both branded and generic pneumonia therapeutics. Biopharmaceutical companies are investing in novel drug formulations, combination therapies, and inhaled antibiotic delivery systems, while public health agencies continue to promote preventive immunization programs against pneumococcal infections.

Challenges: Antibiotic Resistance and Regulatory Complexity

The market faces significant challenges due to the emergence of multidrug-resistant (MDR) pathogens, limiting the effectiveness of traditional antibiotics. Moreover, the high cost and long timelines associated with the development and approval of new antibacterial drugs discourage innovation. However, the growing shift toward personalized medicine, novel mechanisms of action, and monoclonal antibody-based therapies is expected to create new growth opportunities over the forecast period.

Market Segmentation by Infection Type

In 2025, community-acquired pneumonia (CAP) accounted for the largest market share, driven by its widespread prevalence, especially in low- and middle-income countries. Improved access to outpatient care and rapid point-of-care diagnostics are supporting the growth of CAP treatment. The hospital-acquired pneumonia (HAP) segment is expected to record the highest CAGR due to the increasing number of hospitalized and immunocompromised patients, particularly those undergoing invasive procedures. Growing awareness of nosocomial infections and expanded antibiotic stewardship programs are also contributing to segmental growth.

Market Segmentation by Age Group

In 2025, the geriatrics segment dominated the market, as older adults are more susceptible to severe pneumonia due to weakened immune systems and coexisting health conditions such as COPD, diabetes, and heart disease. The pediatrics segment is projected to witness steady growth, supported by large patient pools in developing regions and expanding pediatric vaccination programs. The adult population remains a critical focus area for preventive vaccination and antibiotic therapy as lifestyle and pollution-related respiratory conditions rise globally.

Regional Insights

In 2025, North America held the largest market share, driven by robust healthcare infrastructure, availability of advanced antibiotics, and strong presence of leading pharmaceutical companies. Europe followed, supported by government-funded vaccination campaigns and antibiotic resistance monitoring programs. The Asia Pacific region is expected to record the highest CAGR, owing to high pneumonia prevalence rates, improving access to healthcare, and growing awareness of immunization and antibiotic therapy in countries such as India, China, and Indonesia. Latin America and Middle East & Africa (MEA) represent emerging markets where increasing healthcare investments and pneumonia awareness initiatives are gradually improving treatment accessibility.

Competitive Landscape

The pneumonia therapeutics market is moderately consolidated, with global players focusing on R&D for novel antibiotics, vaccine combinations, and respiratory biologics. Pfizer, GlaxoSmithKline, and AstraZeneca lead the market with strong antibiotic and vaccine portfolios addressing pneumococcal infections. F. Hoffmann-La Roche, Bayer, and Merck & Co. continue to invest in advanced formulations and combination therapies targeting resistant bacterial strains. Abbott Laboratories, AbbVie, and Bristol Myers Squibb are active in immunomodulatory and supportive treatment segments. Generic and regional manufacturers such as Cipla, Lupin Pharmaceuticals, Mylan, and Teva Pharmaceuticals play a key role in making pneumonia drugs affordable in developing markets. Novartis, Baxter International, Johnson & Johnson, and Daiichi Sankyo are investing in targeted therapies and vaccine development. Competitive strategies emphasize drug resistance management, product differentiation, and distribution network expansion, ensuring that innovation and accessibility remain central to pneumonia control efforts worldwide.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Pneumonia Therapeutics market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Infection Type

|

|

Treatment Type

|

|

Age Group

|

|

Route of Administration

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report