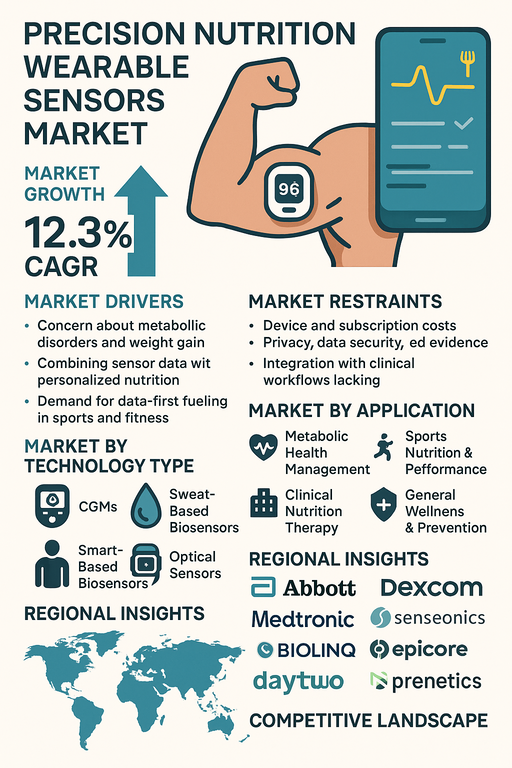

The precision nutrition wearable sensors market is growing at a 12.3% CAGR as consumers, athletes, and patients use real-time body data to personalize diet, timing of meals, and supplement intake. Devices such as continuous glucose monitors (CGMs), sweat-based biosensors, and optical wearables are moving from disease management into broader metabolic health and performance use cases. Within technology types, CGMs currently generate the highest revenue due to their established use in diabetes and growing off-label use in nutrition programs, while sweat-based biosensors are expected to post the highest CAGR as they move from pilot projects into commercial sports, wellness, and workplace offerings. By application, metabolic health management contributes the largest share today, whereas sports nutrition and performance solutions are set to grow the fastest as athletes and active consumers adopt “data-first” fueling strategies.

Market Drivers

Growth is driven by rising concern about metabolic disorders, weight gain, and related conditions such as prediabetes and type 2 diabetes. Consumers want simple tools to see how different foods impact blood sugar, energy, and recovery in real time. Precision nutrition platforms combine wearable sensor data with apps, AI-based insights, and coaching to recommend personalized meal plans, timing of carbohydrates, and macro adjustments. Sports and fitness users demand continuous feedback on fueling and hydration to improve performance and recovery. Advances in miniaturized sensors, low-power electronics, and wireless connectivity make devices more comfortable and easier to integrate into everyday life. Subscription models that bundle sensors, software, and coaching create recurring revenue for solution providers and lower entry barriers for users.

Market Restraints

Adoption is limited by device cost, subscription fees, and the need to replace single-use or short-life sensors, which can be expensive for long-term use outside of clinical reimbursement. Many users find continuous data streams complex and may not have access to professional coaching, reducing perceived value over time. Privacy and data security concerns remain, as nutrition, metabolic, and genetic data must be handled with care. Clinical evidence for some use cases outside diabetes and specific disease areas is still developing, which can slow partnerships with healthcare payers and providers. Integration with electronic health records and existing clinical workflows is incomplete in many regions, limiting uptake in formal nutrition therapy programs.

Market by Technology Type

Continuous glucose monitors (CGMs) form the backbone of the current precision nutrition sensor market. These sensors provide real-time or near-real-time glucose trends and are widely used in diabetes care; within technology types CGMs currently generate the highest revenue and are now repurposed for metabolic optimization, weight management, and sports fueling. Sweat-based biosensors track markers such as electrolytes, hydration status, and selected metabolites using skin patches or smart textiles. This segment is expected to post the highest CAGR as devices become more comfortable, disposable patches fall in price, and partnerships with sports brands and corporate wellness programs expand. Bioimpedance sensors measure body composition, fluid shifts, and sometimes muscle condition. They are used in smart scales, wearables, and clinical devices to support nutrition planning, weight management, and sarcopenia prevention. Optical sensors, including PPG and related optical methods, are embedded in smartwatches and wristbands to estimate heart rate, stress metrics, and in some cases proxies for energy expenditure and sleep; in precision nutrition they link lifestyle metrics to dietary advice and help close the loop between diet, recovery, and daily performance.

Market by Application

Metabolic health management is the leading application, covering prediabetes, diabetes, weight management, and cardiometabolic risk reduction. Users and clinicians rely on sensors to see individual responses to meals and adjust diets accordingly; within applications this segment currently generates the highest revenue. Sports nutrition and performance use wearable sensors during training and competition to guide carbohydrate intake, hydration, and recovery strategies; this segment is expected to record the highest CAGR as endurance athletes, teams, and fitness enthusiasts adopt data-driven fueling and partner with nutrition brands. Clinical nutrition therapy uses sensors to support diet plans in hospitals, clinics, and long-term care, including perioperative care, oncology, and chronic disease management, where precise monitoring of metabolic responses can improve outcomes. General wellness and prevention applications target the broader population with consumer-friendly apps that link daily food logs, sensor data, and simple recommendations focused on energy, mood, and healthy aging.

Regional Insights

North America currently accounts for a large share of revenue due to strong penetration of CGMs, active digital health start-ups, and high consumer awareness of metabolic health and sports performance. Europe shows steady growth under structured healthcare systems and increasing focus on obesity, prediabetes, and preventive programs, with attention to data protection and medical-device rules. Asia Pacific is expected to post one of the highest CAGRs, driven by large populations at risk of metabolic disease, fast growth in connected devices, and strong interest in mobile-first wellness and sports apps. Latin America and the Middle East & Africa are at an earlier stage but show rising demand through private clinics, premium fitness centers, and employer wellness programs. Regions that combine reimbursement for metabolic monitoring with strong digital health ecosystems and consumer spending on fitness and wellness will scale fastest.

Competitive Landscape

Abbott Laboratories and Dexcom Inc are leading CGM suppliers, expanding from diabetes care into partnerships with digital nutrition platforms, sports programs, and consumer apps that interpret glucose data for diet and performance. Medtronic plc and Senseonics Holdings Inc also provide CGM and implantable sensor solutions, focusing on long-term wear and integration with therapy management platforms. Biolinq Inc and Epicore Biosystems develop new generations of minimally invasive and sweat-based biosensors targeting real-time metabolic and hydration insights for both clinical and consumer use. DayTwo Inc, Nutrisense Inc, and Prenetics Global Limited act as precision nutrition platforms, combining CGM or other sensor data with microbiome, genetic, or lifestyle information to deliver personalized diet plans and coaching. Genesis Healthcare Co. participates with genetic and health analysis offerings that support personalized nutrition strategies.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Precision Nutrition Wearable Sensors market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Technology Type

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report