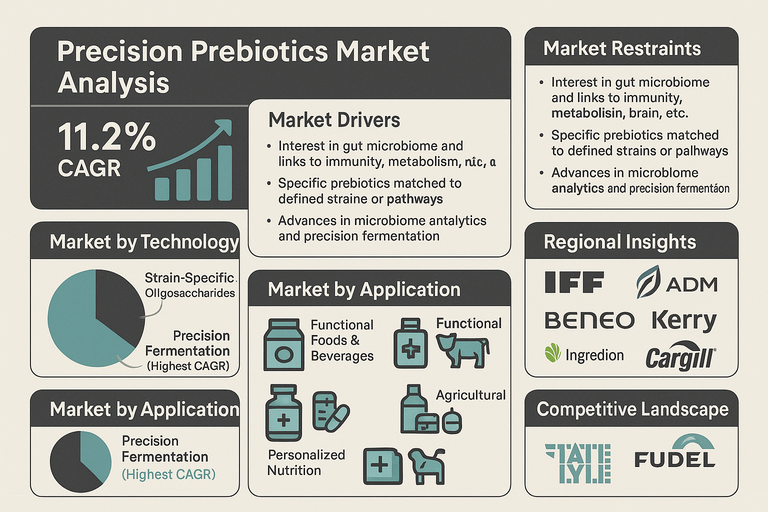

The precision prebiotics market is growing at an 11.2% CAGR as food, nutrition, and health companies move from generic fiber ingredients toward targeted compounds that feed specific beneficial microbes and support measurable health outcomes. Precision prebiotics are designed around defined strains or consortia in the gut, often guided by microbiome data, clinical evidence, and advanced manufacturing platforms like precision fermentation. They are used in dietary supplements, functional foods and beverages, personalized nutrition programs, animal feed, and emerging therapeutic formulations. This shift supports more differentiated products, stronger scientific positioning, and closer integration with diagnostics and digital health tools.

Market Drivers

Growth is driven by rising interest in the gut microbiome and its links to immunity, metabolism, brain health, and chronic disease risk. Consumers and clinicians are moving beyond generic probiotic capsules and basic fibers toward targeted combinations where specific prebiotics are matched to defined microbial pathways or health goals. Advances in sequencing, bioinformatics, and microbiome analytics help identify which bacteria respond to which substrates, enabling strain-specific and condition-specific prebiotics. Precision fermentation and advanced carbohydrate processing technologies allow the production of oligosaccharides that were previously scarce or expensive, including structures similar to those in human milk. Personalized nutrition platforms, microbiome testing services, and digital coaching programs provide direct channels for precision prebiotics, often sold by subscription. In parallel, animal nutrition, pharmaceutical, and personal care industries are exploring microbiome modulation to improve feed efficiency, treatment outcomes, and skin health, adding additional demand beyond human dietary supplements.

Market Restraints

The market faces restraints from high development and production costs, regulatory uncertainty, and the need for stronger clinical evidence. Designing and manufacturing strain-specific or engineered prebiotics requires specialized R&D, including structure–function studies, fermentation optimization, and scale-up, which raises entry barriers. Regulatory frameworks for novel oligosaccharides, engineered prebiotics, and microbiome-modulating ingredients vary by region and can require extensive safety and efficacy documentation, slowing time to market. Many microbiome and health claims are still under evaluation, and authorities limit what can be stated on labels, forcing conservative positioning. Understanding among healthcare professionals and consumers can be uneven, and confusion between probiotics, prebiotics, synbiotics, and postbiotics can dilute messaging. Price points for advanced precision prebiotics are often higher than for commodity fibers, limiting use in cost-sensitive mass-market food products and keeping many applications concentrated in premium supplements and specialized nutrition ranges.

Market by Technology

By technology, strain-specific oligosaccharides and related structured carbohydrates account for the highest revenue because they extend familiar categories such as inulin, FOS, and GOS into more targeted forms that support defined microbial groups, and they can be integrated relatively easily into existing supplement and functional food formats; at the same time, precision fermentation products are expected to record the highest CAGR as companies use engineered microbes and fermentation platforms to manufacture complex oligosaccharides (including HMO-like structures) and other designer prebiotics at scale, with human milk oligosaccharides (HMOs) and modified and engineered prebiotics also growing rapidly as infant nutrition, medical nutrition, and specialized gut health products adopt these higher-value, evidence-backed ingredients.

Market by Application

By application, functional foods and beverages generate the highest revenue in the precision prebiotics market because they leverage established categories such as breakfast cereals, dairy and dairy alternatives, nutrition bars, and drinks, where prebiotics can be incorporated as recognizable “gut health” and “fiber-plus” upgrades at meaningful volumes, while personalized nutrition is expected to post the highest CAGR as microbiome testing companies, digital health platforms, and specialty brands design prebiotic regimens tailored to individual microbiome profiles, health goals, and genetic or lifestyle data, supported by parallel growth in clinical and therapeutic uses, animal nutrition, pharmaceutical applications, personal care and cosmetics, and agricultural applications where precision prebiotics are explored for targeted modulation of microbiomes in specific organs, species, or soils.

Regional Insights

North America and Europe lead the precision prebiotics market due to high awareness of gut health, strong dietary supplement and functional food industries, and active microbiome research ecosystems. Many early launches in HMOs, strain-specific prebiotics, and synbiotic concepts originate from these regions, supported by collaboration between ingredient suppliers, startups, and academic centers. Europe’s regulatory framework for novel foods and claims is stricter but provides clear pathways for approved ingredients, while North America offers strong retail and e-commerce channels and a large base of early adopters. Asia Pacific is expected to show robust growth as companies in Japan, South Korea, China, India, and Southeast Asia combine traditional digestive health concepts with modern microbiome science and as domestic manufacturers scale fermentation capacity for advanced ingredients. Infant formula, clinical nutrition, and fortified foods are key entry points in this region. Latin America and the Middle East & Africa are at earlier stages but are seeing growth in gut health supplements, specialty nutrition, and animal feed applications. Regions with strong regulatory clarity, active microbiome research, and developed supplement and functional food brands will see faster adoption of precision prebiotics.

Competitive Landscape

DuPont/IFF, ADM, BENEO, Kerry Group, Ingredion, Cargill, Tate & Lyle, Cosucra, and Roquette are major ingredient suppliers expanding from conventional fibers and sweeteners into more advanced prebiotic portfolios, including chicory-derived inulin and oligofructose, FOS, GOS, and newer structured carbohydrates designed for defined gut bacteria and applications such as infant and medical nutrition. Yakult Honsha, Deerland Enzymes, and Optibiotix work at the interface of probiotics, enzymes, and precision prebiotics, developing targeted combinations and synbiotic concepts that leverage strain–substrate matching. Sun Genomics, Viome Life Sciences, Seed Health, and similar microbiome-focused companies operate closer to the consumer interface, providing testing, personalized recommendations, and subscription products that integrate precision prebiotics with probiotics and lifestyle guidance. These players rely heavily on data, bioinformatics, and direct engagement with end users. Across the market, companies that can link precise microbiome insights with well-characterized, scalable prebiotic technologies, demonstrate clear benefits with conservative but credible clinical evidence, and support customers with formulation, regulatory, and personalization tools are likely to lead revenue, while those that combine precision fermentation, HMOs, and engineered prebiotics with digital health and personalized nutrition platforms are positioned to capture the highest CAGR in the precision prebiotics market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Precision Prebiotics market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Technology

|

|

Application

|

|

End Use

|

|

Distribution Channel

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report