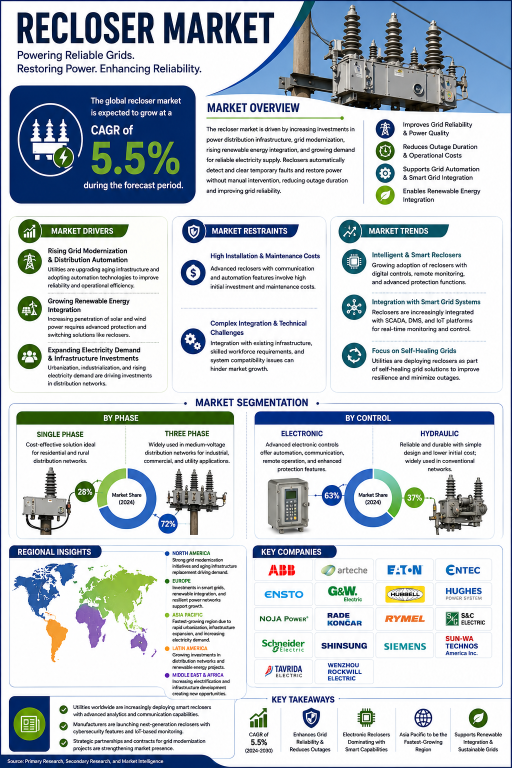

The global recloser market is expected to grow at a CAGR of 5.5% during the forecast period. Market growth is being driven by increasing investments in power distribution infrastructure, rising grid modernization initiatives, growing integration of renewable energy sources, and expanding electricity demand worldwide. Reclosers are critical components of electrical distribution networks, automatically detecting and isolating temporary faults while restoring power without manual intervention. Utilities are increasingly deploying advanced reclosers to improve grid reliability, reduce outage durations, and enhance operational efficiency. The growing adoption of smart grid technologies and digital distribution networks is further supporting market expansion.

Market Drivers

Increasing Grid Modernization and Distribution Automation

Utilities across the world are investing heavily in modernizing aging electrical infrastructure to improve reliability and resilience. Reclosers play an important role in distribution automation by automatically restoring service following temporary faults and minimizing power interruptions. Rising electricity consumption, urbanization, industrial expansion, and government initiatives focused on smart grid deployment are creating significant demand for advanced recloser systems.

Market Restraints

High Installation and Maintenance Costs

The deployment of reclosers involves substantial capital investment, particularly when integrated with advanced monitoring, communication, and automation systems. Utilities may face budget constraints when upgrading existing distribution infrastructure. Additionally, periodic maintenance, technical expertise requirements, and system integration challenges can increase overall ownership costs, particularly in developing regions.

Recloser Market Trends

The market is witnessing increasing adoption of intelligent reclosers equipped with digital control systems, remote monitoring capabilities, and advanced communication technologies. Integration with smart grid platforms, SCADA systems, and distribution management systems is becoming increasingly common. Utilities are also focusing on predictive maintenance, fault location technologies, and self-healing grid solutions to improve operational efficiency and reduce outage durations. Growing renewable energy integration is further driving demand for advanced protection and switching equipment.

Market Segmentation

By Phase

Based on phase, the market is segmented into Single Phase and Three Phase. Three Phase reclosers account for the largest market share due to their widespread deployment across medium-voltage distribution networks serving industrial, commercial, and utility applications. These systems provide enhanced protection and operational flexibility for larger electrical loads. Single Phase reclosers continue to maintain significant demand, particularly in rural distribution networks and residential power distribution applications where cost-effective fault protection solutions are required.

By Control

Based on control, the market is segmented into Electronic and Hydraulic. Electronic reclosers hold a significant market share due to their superior automation capabilities, advanced protection functions, communication features, and compatibility with smart grid systems. Utilities increasingly prefer electronic controls because they enable remote operation, data analytics, and predictive maintenance. Hydraulic reclosers continue to be used in traditional distribution networks due to their proven reliability, simple design, and lower initial costs.

Regional Insights

North America represents a major market for reclosers due to extensive investments in grid modernization, smart grid deployment, and aging infrastructure replacement programs. The United States and Canada continue to invest in advanced distribution automation technologies to improve network reliability. Europe is witnessing steady growth driven by renewable energy integration, digital grid initiatives, and increasing investments in power system resilience. Asia Pacific is expected to record the fastest growth during the forecast period owing to rapid urbanization, expanding electricity demand, infrastructure development, and large-scale grid expansion projects across China, India, Japan, South Korea, and Southeast Asia. Latin America and the Middle East & Africa are also experiencing increasing demand as utilities strengthen distribution networks and improve power reliability.

Competitive Landscape

The recloser market is moderately consolidated, with leading companies focusing on technological innovation, product reliability, digital automation, and global distribution capabilities. Manufacturers are investing in intelligent control technologies, communication platforms, and advanced protection systems to strengthen their competitive positions. Strategic partnerships with utilities, grid modernization projects, and expansion into emerging markets remain important growth strategies. Product differentiation is increasingly based on automation features, cybersecurity capabilities, remote monitoring functions, and integration with smart grid infrastructure.

Key companies operating in the market include ABB, Arteche, Eaton, Entec, Ensto, G&W Electric, Hubbell, Hughes Power System, Noja Power, Rade Koncar, Rymel, S&C Electric, Schneider Electric, Shinsung, Siemens, SUN-WA TECHNOS America Inc., Tavrida Electric, and Wenzhou Rockwill Electric.

Recloser Industry News

The industry is witnessing growing investments in digital distribution automation and intelligent grid protection technologies. Utilities are increasingly deploying smart reclosers equipped with advanced communication capabilities to support self-healing grid operations and renewable energy integration. Manufacturers continue to introduce reclosers with enhanced cybersecurity features, cloud-based monitoring platforms, and predictive maintenance capabilities. The ongoing transition toward smart and resilient power distribution networks is expected to create significant growth opportunities for the recloser market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Recloser market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Phase

|

|

Control

|

|

Interruption

|

|

Voltage

|

|

|

Region Segment (2024-2034; US$ Million)

|

Frequently Asked Questions

What is the expected growth rate of the recloser market?

The recloser market is expected to grow at a CAGR of 5.5% during the forecast period.

Which phase segment holds the largest market share?

Three Phase reclosers hold the largest market share due to their extensive use across utility, industrial, and commercial distribution networks.

Which control segment dominates the market?

Electronic reclosers dominate the market owing to their advanced automation, remote monitoring, communication, and smart grid integration capabilities.

What are the major growth drivers?

Major growth drivers include grid modernization initiatives, increasing distribution automation, growing renewable energy integration, expanding electricity demand, and investments in smart grid infrastructure.

Who are the major companies operating in the market?

Major companies include ABB, Arteche, Eaton, Entec, Ensto, G&W Electric, Hubbell, Hughes Power System, Noja Power, Rade Koncar, Rymel, S&C Electric, Schneider Electric, Shinsung, Siemens, SUN-WA TECHNOS America Inc., Tavrida Electric, and Wenzhou Rockwill Electric.