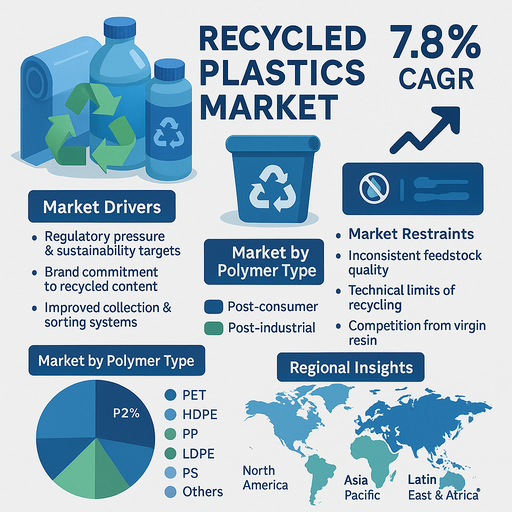

The recycled plastics market is growing at a 7.8% CAGR as brand owners, packaging producers, and manufacturers respond to regulatory pressure, corporate sustainability targets, and consumer concern over plastic waste. Recycled polymers increasingly replace or blend with virgin plastics in bottles, rigid and flexible packaging, textiles, automotive parts, and construction products. Investments in collection, sorting, and mechanical and chemical recycling capacity are helping to improve supply quality and scale. By polymer type, PET and HDPE account for the highest revenue due to their strong use in beverage bottles, food containers, and household packaging, while PP and LDPE are expected to post strong growth as film, flexible packaging, and rigid packaging users commit to higher recycled content. By source type, post-consumer recycled (PCR) resins represent the largest and strategically most important segment as brands target higher PCR content in consumer-facing products, whereas post-industrial recycled (PIR) streams provide more consistent quality and are expected to show steady growth as more manufacturers close the loop on in-plant waste.

Market Drivers

Growth is driven by tightening regulations on single-use plastics, extended producer responsibility (EPR) schemes, and mandatory recycled content targets in packaging and other applications. Governments and regional blocs are setting targets for recycled content in PET beverage bottles and other packaging formats, which directly raises demand for high-quality recycled PET and HDPE. Brand owners across food, beverage, personal care, and household products are making public commitments to increase recycled content and reduce virgin plastic use, translating sustainability pledges into long-term offtake agreements with recyclers. Improvements in collection systems, optical sorting, washing, and decontamination technologies enhance the quality of recycled resins, making them more suitable for food-contact and high-performance applications. Growing consumer awareness of plastic waste and marine pollution supports demand for products featuring visible recycled content claims and eco-labels, allowing some brand owners to charge modest premiums or protect market share. At the same time, volatile virgin resin prices and carbon-reduction programs encourage converters and manufacturers to diversify resin sourcing through recycled materials.

Market Restraints

The market faces restraints from inconsistent feedstock quality, limited collection infrastructure in some regions, and the technical limits of mechanical recycling for certain polymers and applications. Variations in post-consumer waste streams, contamination levels, and sorting performance can lead to quality fluctuations in recycled resins, which complicate high-speed processing and strict application requirements. In many developing markets, collection rates for plastics remain low and informal, limiting the available volume of feedstock and making supply more expensive or less reliable. For some applications, especially high-performance and sensitive food-contact uses, mechanical recycling may not always meet clarity, odor, or performance standards without blending or advanced processing. Investments in chemical recycling are growing but remain capital-intensive, with questions around scale, economics, and regulatory acceptance for food-contact materials. Price competition from virgin resin, especially during periods of low oil and feedstock prices, can weaken the cost advantage of recycled materials. In addition, the diversity of polymer types, additives, and multilayer structures in packaging and products makes it harder to design for recyclability, slowing the full circular transition.

Market by Polymer Type

PET (polyethylene terephthalate) is the largest polymer segment in the recycled plastics market, driven by strong demand for recycled PET (rPET) in beverage bottles, food containers, and polyester fibers. Bottle-to-bottle recycling, supported by deposit return systems and dedicated collection streams, makes PET the most advanced closed-loop system in many regions, and ongoing investments target higher-quality food-grade rPET. HDPE (high-density polyethylene) represents another major segment, with recycled HDPE used in household and personal care bottles, non-food containers, pipes, and industrial packaging. Its good mechanical properties and relative ease of separation support robust demand. PP (polypropylene) recycling is expanding as technologies improve for sorting and cleaning post-consumer PP from packaging and mixed rigid streams; recycled PP is used in automotive parts, non-food packaging, and household goods, and is expected to see strong growth as more companies seek to incorporate rPP in both packaging and durable products. LDPE (low-density polyethylene) recycling, focused on films and flexible packaging such as shrink wrap and bags, is growing as collection and film sorting lines improve, and as brand owners work to increase recycled content in films and flexible packaging. PS (polystyrene) recycling remains smaller, but efforts to collect and recycle PS and EPS waste are increasing, with recycled PS used in insulation, packaging, and some specialty products. The “Others” segment, which includes PVC, ABS, PC, and engineering plastics, is more fragmented and technically complex; recycling volumes are smaller but growing in selected niches such as construction, electronics, and automotive components.

Market by Source Type

Post-consumer recycled (PCR) plastics come from end-of-life consumer and commercial products and packaging that pass through collection, sorting, and recycling systems. PCR resins are central to brand strategies and regulatory targets, as they directly address visible plastic waste and are used in consumer-facing products where recycled content claims matter most. As deposit return schemes, curbside collection, and extended producer responsibility programs expand, PCR volumes and quality are expected to increase. Post-industrial recycled (PIR) plastics originate from production scrap, off-spec parts, and trim waste generated in manufacturing processes. PIR streams are typically cleaner and more homogeneous than PCR, since they come from controlled environments and known polymers, making them easier to reprocess and reintegrate into manufacturing lines. PIR is widely used internally by converters and OEMs to improve material efficiency and reduce waste, and increasingly sold as a defined recycled feedstock. PCR currently dominates the strategic growth agenda due to regulatory and brand commitments, while PIR provides stable, cost-effective volume growth in industrial and B2B applications.

Regional Insights

Europe is a leading region for recycled plastics due to strict regulations on packaging waste, ambitious recycling and recycled content targets, and mature collection and sorting systems. Policy frameworks support high recycling rates for PET and other packaging polymers and encourage investment in advanced mechanical and chemical recycling plants. North America has a significant and growing recycled plastics market, with strong PET and HDPE recycling infrastructure and expanding commitments from brand owners and retailers to use more PCR in packaging and products. Initiatives around deposit systems and improved curbside collection support rising feedstock availability. Asia Pacific is both a major producer and consumer of plastics and is expected to record strong growth in recycling as countries in the region invest in modern collection and sorting infrastructure, move away from informal waste export models, and build domestic recycling capacity. Demand for recycled plastics in packaging, textiles, and consumer goods is increasing as regional and global brands commit to circularity goals. Latin America and the Middle East & Africa are at earlier stages but are building capacity through new collection schemes, regional recycling hubs, and partnerships with global brand owners; in these regions, urbanization and growing awareness of plastic pollution support rising interest in recycled materials. Regions with robust regulatory frameworks, deposit and EPR systems, and strong brand commitments will see faster growth in high-quality recycled plastics.

Competitive Landscape

Indorama Ventures is one of the largest producers of recycled PET globally, with a network of recycling facilities supplying rPET for beverage bottles, food packaging, and fibers, and plays a central role in bottle-to-bottle recycling initiatives with major brands. Veolia Environnement and Suez SA operate large-scale collection, sorting, and recycling businesses, offering mechanical recycling across multiple polymers and providing brand owners and converters with PCR resins and feedstock management services as part of integrated waste and resource solutions. Plastipak Holdings, through its Clean Tech operations, focuses strongly on PET recycling, supporting closed-loop bottle-to-bottle and food-grade rPET supply for beverage and food packaging customers. Alpek Polyester and its subsidiary DAK Americas are important players in the PET and polyester value chain, including recycling operations that supply rPET for packaging and fiber applications. These companies, along with regional recyclers and technology partners, are investing in capacity expansions, improved decontamination and sorting technologies, and in some cases chemical recycling projects to handle more complex waste streams. Firms that can secure reliable feedstock, deliver consistent food-grade and high-spec recycled resins, and work closely with brand owners and converters on design-for-recycling and long-term supply agreements are positioned to lead revenue, while those that scale advanced recycling technologies and expand into additional polymer types are likely to capture the highest CAGR in the recycled plastics market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Recycled Plastics market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Polymer Type

|

|

Source Type

|

|

Recycling Technology

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report