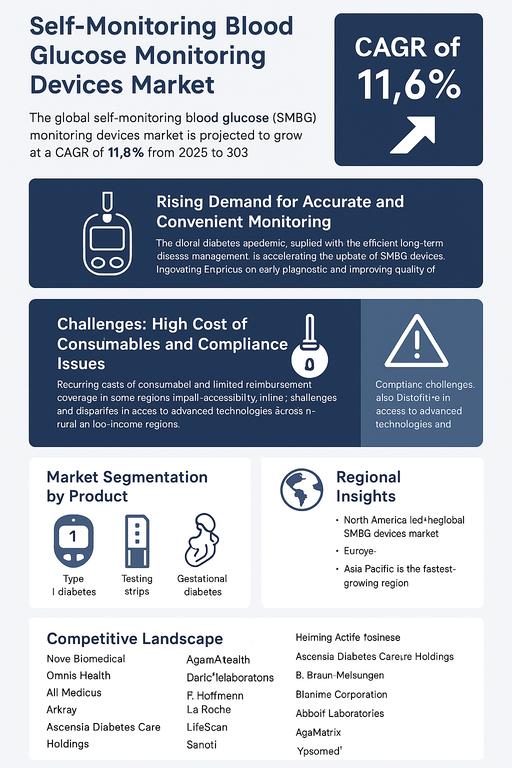

The global self-monitoring blood glucose (SMBG) monitoring devices market is projected to grow at a CAGR of 11.6% from 2026 to 2034. Growth is driven by the rising global diabetes population, increasing emphasis on early diagnosis and monitoring, and the expansion of home-based healthcare practices. SMBG devices, including meters, testing strips, and lancets, are essential tools that enable patients to regularly track blood glucose levels, empowering better glycemic control and improving quality of life. The trend toward personalized and proactive diabetes management is significantly boosting adoption across both Type 1 and Type 2 diabetes patients.

Rising Demand for Accurate and Convenient Monitoring

The global diabetes epidemic, coupled with the rising need for efficient long-term disease management, is accelerating the uptake of SMBG devices. Patients and healthcare professionals are prioritizing devices that offer rapid results, user-friendliness, and portability. The increasing integration of SMBG meters with smartphones and cloud-based health platforms allows real-time data sharing, strengthening adherence to treatment regimens. Additionally, advancements in disposable consumables such as high-sensitivity testing strips and minimally invasive lancets are enhancing patient convenience and accuracy of results.

Challenges: High Cost of Consumables and Compliance Issues

Despite strong market expansion, challenges persist. The recurring cost of consumables such as testing strips and lancets remains a burden, especially in price-sensitive markets. Limited reimbursement coverage in some regions further impacts accessibility for patients. Compliance challenges also exist, as some patients struggle with frequent testing routines due to discomfort, lack of awareness, or insufficient education. Furthermore, disparities in access to advanced SMBG technologies across rural and low-income regions restrict adoption. However, ongoing product innovation, broader insurance support, and increased patient education programs are expected to mitigate these barriers over time.

Market Segmentation by Product

By product, the market is segmented into self-monitoring blood glucose meters, consumables, testing strips, and lancets. In 2025, testing strips accounted for the largest revenue share, as they are the most frequently used consumables in daily glucose monitoring. SMBG meters are gaining adoption through improved design, portability, and smartphone integration, while lancets continue to evolve with innovations in painless sampling technology. Consumables remain the largest revenue driver due to their recurring purchase requirement, ensuring continuous market demand.

Market Segmentation by Application

By application, the market is divided into Type 1 diabetes, Type 2 diabetes, and gestational diabetes. Type 2 diabetes dominates the segment, supported by the rising global prevalence linked to obesity and lifestyle changes. Type 1 diabetes patients represent a significant user base due to the necessity of frequent glucose monitoring for insulin management. Gestational diabetes is an emerging application area, with growing awareness of the importance of continuous monitoring during pregnancy to prevent maternal and fetal complications.

Regional Insights

In 2025, North America led the global SMBG devices market, backed by advanced healthcare infrastructure, strong adoption of digital health technologies, and favorable reimbursement frameworks. Europe followed, with countries like Germany, the UK, and France focusing on patient-centric diabetes care and government-supported screening programs. Asia Pacific is the fastest-growing region, led by China, India, and Japan, where the high diabetes burden and increasing investments in affordable healthcare technologies are boosting adoption. Latin America and the Middle East & Africa (MEA) are emerging markets where rising awareness, healthcare expenditure, and urbanization are opening new growth opportunities.

Competitive Landscape

The 2025 market was characterized by strong competition among global medtech leaders and regional specialists. Abbott Laboratories and F. Hoffmann-La Roche remain leading players, leveraging innovation in glucose meters and consumables along with extensive global distribution networks. LifeScan and Ascensia Diabetes Care are well-positioned with reliable product portfolios and physician partnerships. Nova Biomedical, Arkray, and Bionime Corporation are strengthening positions with advanced meters and competitive consumables. DarioHealth and AgaMatrix are focusing on smartphone-connected monitoring and digital health integration. Meanwhile, Sanofi, Ypsomed Holding, and B. Braun Melsungen leverage their broad healthcare portfolios to enter the SMBG space with integrated patient solutions. Competitive differentiation is being driven by pricing, ease of use, connectivity, and accuracy, shaping rapid market evolution.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Self-Monitoring Blood Glucose Monitoring Devices market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product

|

|

Application

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report