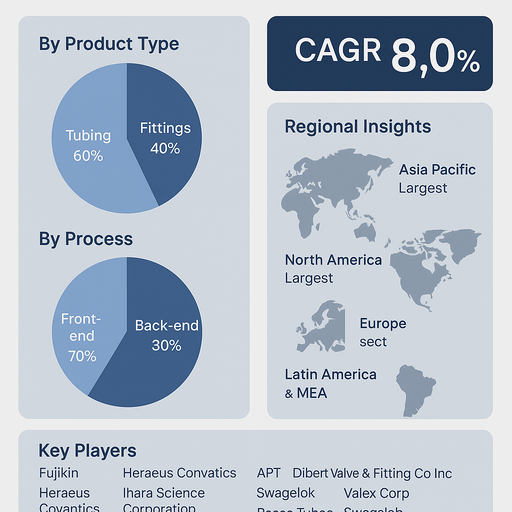

The global semiconductor tubing and fittings market is projected to grow at a CAGR of 8.0% from 2026 to 2034, supported by rising demand for advanced semiconductor manufacturing, miniaturization of electronic components, and investments in next-generation fabrication facilities. Tubing and fittings, essential for the transfer of high-purity gases and chemicals in semiconductor processes, are critical for maintaining contamination-free environments and ensuring precision in wafer production. As the semiconductor industry advances into sub-5nm technology nodes, demand for high-quality, durable, and chemically resistant tubing and fittings continues to expand.

Growing Demand for High-Purity Components

Semiconductor fabrication processes require ultra-pure gases, deionized water, and corrosive chemicals for wafer cleaning, etching, deposition, and lithography. Tubing and fittings play a vital role in preventing contamination and ensuring safe, efficient flow within front-end and back-end operations. The rising adoption of advanced process technologies, such as EUV lithography and 3D stacking, has intensified demand for high-performance tubing and fittings made from materials like stainless steel, fluoropolymers, and engineered plastics. Additionally, the expansion of fab capacity in Asia Pacific, North America, and Europe is creating sustained market opportunities.

Challenges: High Costs and Supply Chain Risks

Despite positive growth, the market faces challenges including high production costs of specialized tubing and fittings due to stringent quality and purity standards. Volatility in raw material prices and supply chain disruptions, especially for stainless steel and specialty alloys, affect market stability. Additionally, the need for compliance with industry-specific standards (SEMI, ISO) adds to manufacturing complexity and costs. Dependence on semiconductor industry cycles also creates demand fluctuations, impacting suppliers’ profitability. However, long-term demand for chips in AI, automotive electronics, and consumer devices is expected to offset cyclical downturns.

Market Segmentation by Product Type

By product type, the market is segmented into tubing and fittings. Tubing holds the largest share due to its wide application in transporting process gases and liquids in semiconductor fabs. Fittings, though smaller in market size, are equally critical for maintaining sealed, leak-proof connections that prevent contamination. Continuous innovations in corrosion-resistant materials and modular designs are enhancing durability and efficiency of both tubing and fittings.

Market Segmentation by Process

By process, the market is divided into front-end and back-end. The front-end segment dominates, as tubing and fittings are indispensable in wafer fabrication stages involving lithography, etching, cleaning, and deposition. Back-end processes, including assembly and packaging, also rely on tubing and fittings, though demand is relatively smaller. With the growing complexity of advanced packaging technologies, such as chiplets and heterogeneous integration, back-end demand is expected to see steady growth over the forecast period.

Regional Insights

In 2025, Asia Pacific led the semiconductor tubing and fittings market, supported by large-scale fab operations in Taiwan, South Korea, China, and Japan. North America followed, with major semiconductor players in the U.S. driving investments in domestic manufacturing through initiatives like the CHIPS Act. Europe is also emerging as a key market, with growing investments in semiconductor supply chain security and cleanroom infrastructure. Latin America and Middle East & Africa (MEA) remain smaller markets but show potential as global semiconductor value chains diversify geographically.

Competitive Landscape

The 2025 market was moderately consolidated, with global leaders and regional specialists providing tubing and fittings tailored for semiconductor applications. Swagelok, Valex Corp, and FUJIKIN lead in ultra-high-purity stainless steel tubing and fittings. Heraeus Covantics and Saint-Gobain specialize in high-performance fluoropolymer and plastic tubing solutions. Ihara Science Corporation, Superlok, and FITOK Group are strong players in Asia, offering high-quality fittings at competitive prices. Nippon Steel Corp and Rensa Tubes supply specialized alloy tubing for semiconductor applications. Advance Fittings Corp, APT, Dibert Valve & Fitting Co Inc, Masterflex Group, and Orion strengthen their presence in niche product categories. Competitive strategies focus on innovation in corrosion-resistant materials, precision manufacturing, global distribution, and long-term supply partnerships with semiconductor fabs.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Semiconductor Tubing and Fittings market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product Type

|

|

Process

|

|

Equipment Type

|

|

Distribution Channel

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report