The global sleep tech devices market is projected to grow at a CAGR of 18.3% from 2025 to 2033, driven by rising awareness of sleep health, growing prevalence of sleep disorders, and increasing adoption of connected health solutions. Sleep tech devices include both wearables and non-wearables designed to monitor, analyze, and improve sleep quality. These solutions play an essential role in addressing conditions such as obstructive sleep apnea, insomnia, and narcolepsy while catering to a growing consumer segment focused on wellness and preventive healthcare. Technological advancements in AI, biosensors, and IoT integration are further strengthening the demand for next-generation sleep solutions.

Rising Sleep Disorders and Consumer Health Awareness Fueling Growth

The prevalence of sleep-related disorders, particularly obstructive sleep apnea and insomnia, has grown significantly across both developed and developing regions. This rise, coupled with greater consumer awareness of the impact of sleep on overall health, is fueling market demand. Wearable devices such as smartwatches, bands, and rings have become popular for tracking sleep patterns, heart rate, and oxygen levels. Non-wearable solutions, including sleep monitors and smart beds, are also gaining traction, offering advanced features like automatic adjustments, temperature regulation, and contactless monitoring. Integration of these devices into broader digital health ecosystems, alongside telemedicine and remote monitoring platforms, is expanding accessibility and improving clinical outcomes.

Challenges: High Costs and Data Privacy Concerns

Despite strong market growth, several challenges hinder wider adoption. Advanced sleep tech devices such as smart beds and premium monitoring systems remain costly, limiting penetration in price-sensitive regions. Data privacy and security concerns also persist, as most devices collect sensitive biometric data that is transmitted to cloud-based platforms. Additionally, lack of interoperability across multiple devices and ecosystems creates complexities for end-users seeking seamless integration. However, ongoing developments in AI-powered personalization, cloud-based analytics, and affordable consumer-grade solutions are mitigating these challenges, supporting long-term market growth.

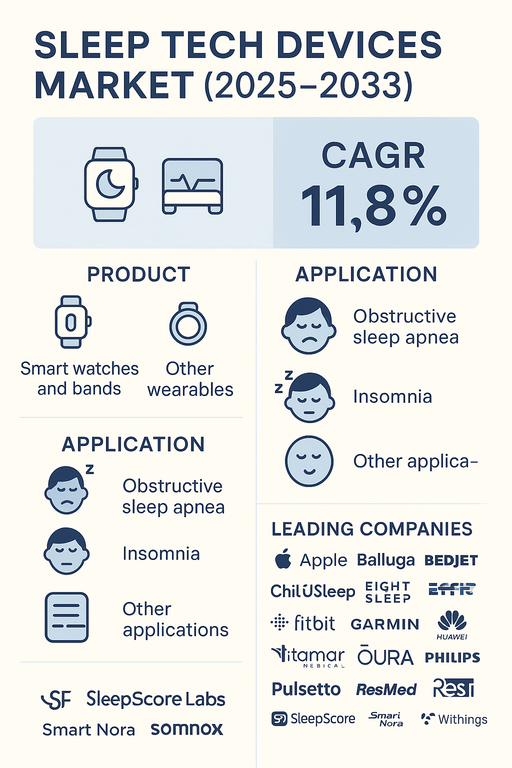

Market Segmentation by Product

By product type, the sleep tech devices market is segmented into wearables and non-wearables. Wearables include smartwatches, bands, and other devices such as rings and headbands, which collectively dominated the market in 2024 due to their affordability, multifunctional applications, and integration with fitness platforms. Non-wearables include sleep monitors and smart beds, which are steadily growing in demand among premium consumers and clinical users. Smart beds in particular are gaining attention with features like personalized climate control, pressure adjustment, and integration with connected home systems.

Market Segmentation by Application

By application, the market is divided into obstructive sleep apnea, insomnia, narcolepsy, and other applications. Obstructive sleep apnea held the largest market share in 2024, supported by increasing diagnostic rates and strong adoption of devices for continuous monitoring. Insomnia applications are also witnessing strong growth, with consumer-focused solutions such as wearable trackers and contactless monitoring devices gaining popularity. Narcolepsy and other sleep disorders represent smaller but steadily expanding segments as greater awareness and technological innovation enhance treatment options.

Regional Insights

In 2024, North America led the market, driven by strong consumer spending on wellness, high prevalence of sleep disorders, and favorable reimbursement for sleep apnea treatment devices. Europe followed, with Germany, the UK, and Nordic countries emerging as key adopters due to advanced healthcare infrastructure and rising interest in digital health. Asia Pacific is the fastest-growing region, with significant contributions from China, India, and Japan, where rising healthcare awareness, government initiatives, and growing penetration of global consumer electronics brands are creating strong growth opportunities. Latin America and the Middle East & Africa (MEA) are emerging markets, with increasing urbanization, internet penetration, and expanding healthcare investments supporting gradual adoption, though cost and infrastructure challenges remain.

Competitive Landscape

The 2024 market was characterized by intense competition between consumer electronics leaders and medical device companies. Apple, Fitbit (Google), Garmin, Huawei, Oura Health, Withings, and Xiaomi led the wearables category, offering multi-sensor platforms that combine fitness, health, and sleep tracking. ResMed, Philips, and Itamar Medical dominated the medical-grade sleep solutions segment with strong portfolios in obstructive sleep apnea diagnostics and treatment devices. Companies such as Eight Sleep, Balluga, ReST, ChiliSleep, and BedJet specialized in smart beds and temperature regulation technologies, catering to both consumer and clinical demand. Niche innovators like SleepScore Labs, Somnofy, Somnox, Smart Nora, Emfit, and Pulsetto introduced AI-driven analytics, non-invasive monitoring, and stress-reduction technologies. Competitive differentiation is shaped by accuracy, affordability, integration with digital ecosystems, and the ability to deliver clinically validated insights alongside consumer convenience.

Historical & Forecast Period

This study report represents analysis of each segment from 2023 to 2033 considering 2024 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2025 to 2033.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Sleep Tech Devices market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2023-2033 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Historical Year | 2023 |

| Unit | USD Million |

| Segmentation | |

Product

| |

Application

| |

Distribution Channel

| |

|

Region Segment (2023-2033; US$ Million)

|

Key questions answered in this report