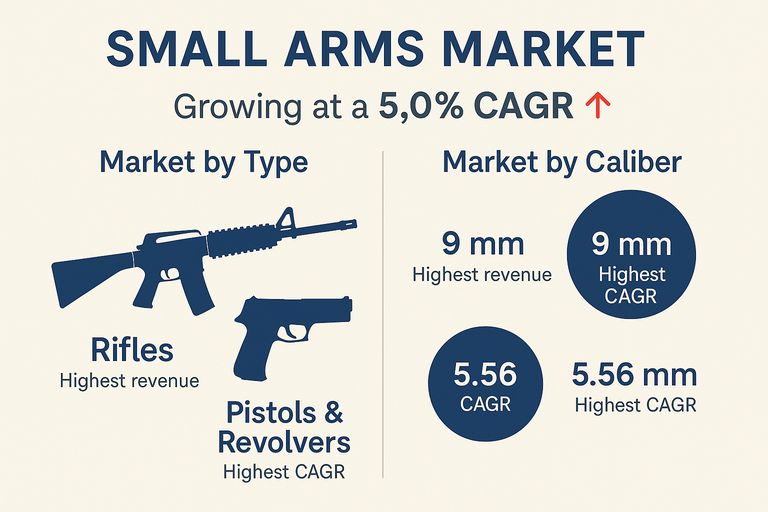

The small arms market is growing at a 5.0% CAGR as defense forces, law enforcement agencies, and civilian users continue to upgrade and replace legacy weapons with more modular, ergonomic, and accessory-ready platforms. Demand is supported by military modernization programs, internal security requirements, and steady civilian interest in sporting, hunting, and personal protection firearms. Within types, rifles currently generate the highest revenue because they dominate front-line military and many law-enforcement and sporting applications, while pistols & revolvers are expected to post the highest CAGR as sidearm replacement cycles, concealed-carry markets, and specialized law-enforcement requirements expand. By caliber, 9 mm ammunition accounts for the highest revenue due to its widespread use in military, police, and civilian handguns and submachine guns, whereas 5.56 mm is expected to record the highest CAGR as armed forces and security units continue to field modern assault rifles and light support weapons in this caliber.

Market Drivers

Growth is driven by ongoing military and paramilitary modernization programs that replace older platforms with lighter, modular small arms compatible with optics, suppressors, and under-barrel accessories. Many countries are shifting from legacy 7.62 mm battle rifles to 5.56 mm or modern 7.62 mm platforms with improved ergonomics and rails, which generates fresh demand for both weapons and compatible ammunition. Law-enforcement agencies are upgrading duty pistols, patrol carbines, and less-lethal options to improve accuracy, reliability, and interoperability with tactical accessories. Civilian demand from sport shooting, hunting, and personal defense adds a stable revenue base in markets where ownership is regulated but allowed. Replacement of aging stockpiles, new police units, and special operations requirements further support the market. At the same time, incremental innovation in materials, recoil management, and integrated optics stimulates replacement demand even in mature segments.

Market Restraints

The small arms market faces strong regulatory and political constraints. Stricter export controls, arms-embargo regimes, and licensing requirements can delay or block international contracts. Domestic gun-control measures, changes in civilian ownership laws, and public concern about firearm misuse can limit demand or shift it toward specific user groups. Budget pressures in some countries delay modernization cycles, leading to life-extension of legacy platforms rather than new procurements. High competition and commoditization in some segments, especially basic pistols and shotguns, put pressure on margins. Compliance with evolving standards on safety, traceability, and marking raises manufacturing and documentation costs. In addition, reputational risk and environmental concerns around lead ammunition and old stockpile disposal can affect procurement policies and export approvals.

Market by Type

Pistols & revolvers serve as standard sidearms for military officers, law-enforcement personnel, and many security and civilian users. Compact and subcompact pistols gain traction for concealed carry and specialized roles. While unit prices are often lower than for rifles, high annual volumes and frequent replacement of police duty weapons support solid growth; within types, pistols & revolvers are expected to post the highest CAGR over the forecast period. Rifles, including assault rifles, designated marksman rifles, and precision rifles, form the backbone of military and many law-enforcement operations. They are central to infantry modernization and remain the largest revenue contributor within the small arms portfolio. Shotguns occupy a niche but important role in law enforcement, home defense, and hunting, particularly in close-quarters and breaching scenarios. Machine guns, covering light, medium, and heavy systems, are more specialized but command high unit values and are critical in infantry support and vehicle-mounted roles; they see steady replacement and upgrade cycles in professional forces. The “Others” category includes submachine guns, personal defense weapons, and specialized carbines that address close-protection, urban operations, and special operations needs, often bundled with advanced optics and suppressors.

Market by Caliber

5.56 mm calibers are widely used in assault rifles and light machine guns, especially within NATO and partner countries, and are central to many modernization programs; this segment is expected to deliver the highest CAGR as forces adopt new 5.56 mm platforms or upgrade existing ones. 7.62 mm calibers remain important for designated marksman rifles, general-purpose machine guns, and legacy battle rifles, providing greater range and stopping power and retaining a significant share of both military and civilian markets. The 9 mm segment is dominant in handguns and submachine guns worldwide and, due to massive installed base and high ammunition consumption rates, currently generates the highest revenue among calibers. Larger calibers such as 12.7 mm and 14.5 mm are employed mainly in heavy machine guns, anti-materiel roles, and vehicle or naval mounts; although volumes are lower, unit values and specialized military applications give them a steady but more niche revenue contribution. “Others” includes regional or legacy calibers used in hunting, sport shooting, and older military systems that remain in service in some markets.

Regional Insights

North America represents a major share of the small arms market due to high defense and law-enforcement spending combined with a large and regulated civilian firearms sector. Europe shows steady demand driven by NATO modernization, border security, and internal security requirements, though civilian ownership patterns vary widely by country. In Asia Pacific, rising defense budgets, territorial tensions, and modernization of land forces in countries such as India, China, South Korea, and others support strong demand for rifles, machine guns, and sidearms. The Middle East and parts of Africa see procurement linked to regional security dynamics, counterterrorism operations, and internal security forces, often involving large multi-year contracts. Latin America experiences mixed dynamics, with security needs and police modernization in some countries offset by budget limits and regulatory constraints. Regions with active modernization programs, high perceived security threats, and established defense-industrial partnerships tend to show the strongest and most predictable demand for small arms.

Competitive Landscape

Smith & Wesson Brands, Inc., Sturm, Ruger & Co., Inc., SIG SAUER, GLOCK, and Taurus Armas are key suppliers of pistols and revolvers to law enforcement, security, and civilian markets, focusing on reliability, ergonomics, and modular platforms with a wide accessory ecosystem. FN Herstal, Heckler & Koch, Beretta, Colt’s Manufacturing, CZ, Israel Weapon Industries (IWI), and Kalashnikov Concern JSC provide full portfolios covering pistols, carbines, rifles, and machine guns, targeting military and police tenders as well as professional and sporting users. Barrett Firearms Manufacturing specializes in large-caliber precision rifles and anti-materiel platforms, while Daniel Defense, Savage Arms, Mossberg & Sons, Benelli Armi, and Armscor International are prominent in sporting, tactical, and hunting segments with rifles and shotguns. American Outdoor Brands and related accessory companies supply optics, mounts, stocks, and other enhancements that are often bundled with small arms in professional and civilian markets. Companies with broad product lines, strong compliance and export capabilities, and close relationships with defense ministries, police agencies, and major distributors are positioned to lead current revenue, while those that invest in modular platforms, lighter materials, and integrated accessory ecosystems are likely to capture higher growth within the small arms market.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Small Arms market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Type

|

|

Caliber

|

|

Barrel Type

|

|

Technology

|

|

Firing Mechanism

|

|

Operation Mode

|

|

End Use Application

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report