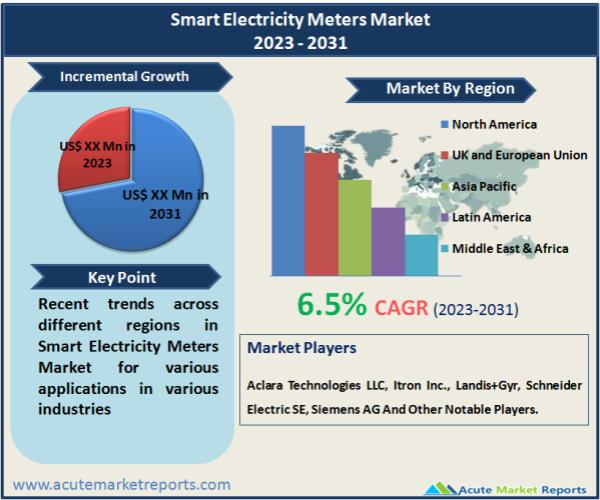

The smart electricity meters market is experiencing significant growth due to the increasing focus on energy conservation, the need for accurate billing and monitoring, and the rising adoption of smart grid technologies. Smart electricity meters are advanced devices that enable two-way communication between the utility company and consumers. They provide real-time data on energy consumption, facilitate remote meter reading, and offer features such as time-of-use pricing and load control.The global smart electricity meters market is projected to grow at a CAGR of 6.5% during the forecast period of 2026 to 2034. Smart electricity meters offer benefits such as improved meter accuracy, reduced operational costs for utility companies, and enhanced energy management capabilities for consumers. With the increasing focus on energy efficiency and the integration of renewable energy sources, the demand for smart electricity meters is expected to surge.

Energy Efficiency and Conservation

The drive towards energy efficiency and conservation is a significant driver for the Smart Electricity Meters Market. Smart meters enable real-time monitoring of energy consumption, providing consumers with valuable insights into their usage patterns and promoting energy-saving behaviors. By empowering consumers to make informed decisions about their energy consumption, smart meters contribute to reducing overall energy demand and optimizing energy usage. For example, a study conducted by the American Council for an Energy-Efficient Economy (ACEEE) found that residential households with smart meters achieved energy savings ranging from 1% to 3%.

Grid Modernization and Smart Grid Initiatives

The need for grid modernization and the implementation of smart grid initiatives is another key driver for the Smart Electricity Meters Market. Smart meters play a vital role in enabling two-way communication between utilities and consumers, facilitating dynamic pricing, demand response programs, and grid management. They provide accurate and timely data on energy consumption, enabling utilities to optimize energy distribution, identify areas of inefficiency, and reduce losses. The integration of renewable energy sources and the effective management of distributed energy resources are also supported by smart metering systems.

Government Policies and Mandates

Government policies and mandates promoting the deployment of smart meters are driving the growth of the Smart Electricity Meters Market. Many governments worldwide have introduced regulations and initiatives to encourage the adoption of smart metering systems. For instance, the European Union has set a target for member states to achieve 80% smart meter penetration by 2021. These policies create a favorable regulatory environment, incentivize utilities and consumers to invest in smart metering infrastructure, and drive market growth. In addition, government-backed financial incentives and rebate programs further support the adoption of smart meters.

Infrastructure Limitations and Implementation Costs

The deployment of smart electricity meters faces the challenge of infrastructure limitations and high implementation costs. Upgrading existing metering infrastructure to support smart meters requires significant investments in hardware, communication networks, and data management systems. The cost of installation, including meter replacements and network infrastructure upgrades, can be substantial, particularly for utilities serving large customer bases. For example, a study conducted by the U.S. Department of Energy estimated the cost of implementing advanced metering infrastructure (AMI) to range from $200 to $500 per meter. Moreover, the existing electrical grid infrastructure may not be well-equipped to handle the increased data transmission and processing requirements of smart meters. Upgrading the infrastructure and establishing reliable communication networks can be complex and time-consuming, posing challenges to the widespread adoption of smart meters. These implementation costs and infrastructure limitations can impede the pace of smart meter deployments, especially in regions with limited financial resources or outdated grid systems. Additionally, concerns related to data privacy and security can act as a restraint. The collection and transmission of real-time energy consumption data raise privacy concerns among consumers. Ensuring the secure storage and transfer of sensitive information requires robust cybersecurity measures and compliance with data protection regulations. Addressing these concerns and establishing trust in data privacy and security are essential for the successful deployment of smart electricity meters.

Single Phase Meters Reign in Revenue, Three Phase Meters Surge in Growth

Single phase meters are used in residential and small commercial settings where the electricity supply is typically single-phase. These meters measure the consumption of electricity for individual households or small businesses. Single phase meters have been widely adopted globally and have contributed to the overall growth of the smart electricity meters market. Three phase meters are designed for industrial, commercial, and larger residential applications where the electricity supply is three-phase. These meters measure electricity consumption across all three phases and are capable of handling higher power loads. The adoption of three phase meters has been increasing, particularly in industrial and commercial sectors, to enable better monitoring and management of energy usage.

Residential Sector Leading in Revenue, Industrial Sector Driving Growth with Smart Meters

The residential sector represents households and individual consumers. Smart electricity meters in the residential segment enable accurate measurement of energy consumption, real-time monitoring, and data analysis for efficient energy management. The growing emphasis on energy conservation and the adoption of smart home technologies are driving the demand for smart meters in residential settings. This segment generally accounts for a significant share of the smart electricity meters market revenue due to the large number of residential customers. The industrial sector comprises manufacturing plants, factories, and large-scale industries. Smart meters in the industrial segment provide accurate energy monitoring, load management, and power quality analysis. Industrial facilities with high energy demands can utilize smart meters to optimize energy usage and reduce costs. The CAGR for the industrial sector in the smart electricity meters market has the potential to be higher than the residential and commercial sectors due to the increasing need for efficient energy management in industrial facilities.

North America: The Global Leader in Smart Electricity Meters Market

North America holds a significant revenue share in the smart electricity meters market. This region has emerged as a prominent market for smart meters due to various factors that have facilitated their widespread adoption. One of the key drivers behind North America's revenue leadership is the early adoption of smart meters in the region. Utility companies in North America have been at the forefront of deploying smart grid infrastructure, which includes the installation of advanced metering systems. This proactive approach has enabled utilities to leverage the benefits of smart meters for improved energy management, demand response programs, and enhanced customer engagement. Additionally, government mandates and regulations have played a crucial role in driving the adoption of smart meters in North America. Many states and provinces have implemented policies that require utilities to install smart meters as part of their grid modernization initiatives. These mandates have provided a strong impetus for the deployment of smart meters, further boosting the revenue share of the region. The Asia Pacific region is experiencing a remarkable surge in the adoption of smart meters, driven by several factors that contribute to its significant growth potential in the market. One key driver is rapid urbanization in the region. As urban areas expand and populations grow, there is an increasing need for efficient energy management and resource conservation. Smart meters provide accurate measurement of energy consumption, enable real-time monitoring, and facilitate demand-side management, helping utilities and consumers make informed decisions about energy usage. The rise in urbanization and the associated increase in electricity demand have fueled the demand for smart meters in the Asia Pacific region.

Completive Trends

The smart electricity meters market is marked by intense competition among market players such as Aclara Technologies LLC, Itron Inc., Landis+Gyr, Schneider Electric SE, Siemens AG, ABB, Ltd., microchip Technology Inc., Elster Group GmbH, OSAKI Electric Co., Ltd., driven by technological innovation, strategic partnerships, market consolidation, customer engagement, cybersecurity, and global expansion. Companies are investing in research and development to introduce advanced technologies and functionalities in smart meters. Strategic collaborations and acquisitions are helping companies expand their market reach and product portfolio. Focus on customer engagement and data analytics capabilities is becoming increasingly important, while cybersecurity measures are being strengthened to protect data privacy. Market players are also targeting emerging markets and adapting their offerings to regional requirements. These competitive trends reflect the dynamic nature of the market and the strategies employed by companies to maintain a competitive edge in the smart electricity meters industry.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Smart Electricity Meters market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Phase

|

|

Communication Technology

|

|

End-User

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report