The solar thermal market is anticipated to grow at a CAGR of 8.1% during the forecast period 2026 to 2034. This growth is driven by rising global efforts to decarbonize energy systems, coupled with government incentives promoting the adoption of renewable heating solutions. Solar thermal systems convert sunlight into heat for residential, commercial, and industrial applications - especially in regions with high solar insolation. These systems are increasingly favored for domestic hot water, space heating, industrial process heat, and solar cooling. As environmental concerns intensify, solar thermal technologies offer a cost-effective, sustainable alternative to fossil fuel-based heating systems.

Market Drivers

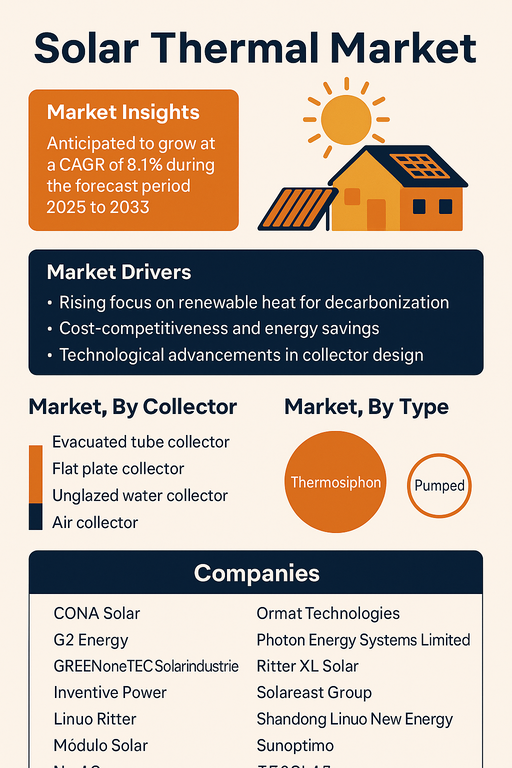

Rising Focus on Renewable Heat for Decarbonization

Global heating sectors account for over 40% of energy-related CO₂ emissions. Solar thermal technologies provide a clean and efficient means of reducing emissions from buildings and industrial processes. Policies such as the EU's Renewable Energy Directive (RED III) and China's solar water heating mandates are pushing large-scale solar thermal adoption. For instance, in 2025, numerous governments across Europe and Asia invested in solar district heating networks - boosting long-term market potential.

Cost-Competitiveness and Energy Savings

Once installed, solar thermal systems provide long-term cost savings, especially in regions with high electricity or natural gas prices. Commercial and industrial sectors are particularly attracted to solar heat for pre-heating water or supporting thermal processes below 150°C. Countries like Mexico, India, and Germany have seen significant industrial adoption in sectors such as dairy, textiles, food processing, and pulp & paper.

Technological Advancements in Collector Design

Innovation in collector technologies (including better heat transfer fluids, improved insulation, and selective coatings) has significantly increased system efficiency. In particular, evacuated tube collectors with higher thermal performance in cold or cloudy climates have expanded the geographic scope of deployment. Integrated system designs that include thermal storage or hybrid photovoltaic-thermal (PVT) components further extend use cases.

Market Restraint

Lack of Awareness and Initial Capital Costs

Despite the proven benefits, lack of consumer awareness and relatively high upfront costs remain major barriers to widespread adoption - especially in low-income regions or among small businesses. Financial incentives such as subsidies or green loans are critical to offset these entry costs. Additionally, in markets with dominant low-cost natural gas infrastructure, the business case for solar thermal may be harder to justify without policy support.

Market Segmentation by Collector

The Collector segment includes Evacuated Tube Collectors, Flat Plate Collectors, Unglazed Water Collectors, and Air Collectors. Among these, Flat Plate Collectors generated the highest revenue in 2025, primarily due to their versatility and use in residential and commercial buildings. They are well-suited for moderate climates and low-temperature applications such as domestic water heating. Evacuated Tube Collectors, on the other hand, are expected to witness the highest CAGR from 2026 to 2034. Their ability to operate efficiently in low-irradiance or colder environments makes them ideal for regions with harsh winters or industrial applications requiring higher output temperatures. Advancements in vacuum insulation, absorber coatings, and anti-fouling materials further increase performance and durability. Unglazed Water Collectors are gaining traction in niche applications such as swimming pool heating or agricultural uses where low-cost, low-temperature heating is sufficient. Meanwhile, Air Collectors are finding adoption in commercial ventilation and solar drying applications, particularly in industries such as wood, tea, and spices.

Market Segmentation by Type

The Type segment is categorized into Thermosiphon and Pumped systems. Thermosiphon systems dominated revenue generation in 2025 due to their simplicity, cost-effectiveness, and widespread use in residential applications. They are highly popular in countries like India, Brazil, and South Africa, where decentralized water heating solutions are encouraged. Pumped systems are expected to register higher growth during the forecast period, especially in commercial and industrial segments. These systems allow for greater design flexibility and performance optimization, as they enable fluid circulation irrespective of the storage tank location. The increasing trend of integrating solar thermal with conventional backup heating or district heating networks further supports the growth of pumped configurations.

Geographic Trends

Geographically, Asia Pacific held the largest market share in 2025 and is projected to retain its dominance through 2034, with the highest CAGR as well. Countries such as China, India, and Japan are aggressively pushing solar thermal installations via mandates, subsidy programs, and awareness campaigns. China's vast residential and commercial sectors are significant contributors to global collector deployment, with millions of square meters of annual collector area additions. Europe remains a mature yet high-value market, especially in countries such as Germany, Austria, and Denmark, which are investing in solar district heating and decarbonized building retrofits. Government initiatives such as REPowerEU, along with national-level energy transition programs, are driving large-scale solar thermal integration in urban heating networks. Latin America, particularly Mexico and Brazil, is gaining momentum due to solar resource availability and national clean energy goals. Meanwhile, Middle East & Africa (MEA) offers strong future potential, driven by rising energy demand, high insolation levels, and a growing push toward clean industrial heat.

Competitive Trends

Key players in the market include CONA Solar, G2 Energy, GREENoneTEC Solarindustrie, Inventive Power, Linuo Ritter, Módulo Solar, Next Source, Ormat Technologies, Photon Energy Systems Limited, Ritter XL Solar, Solareast Group, Shandong Linuo New Energy, Sunoptimo, T.E SOLAR, and Vicot. These companies collectively invested in expanding collector production, enhancing international distribution networks, and developing turnkey thermal energy systems in 2025.

Between 2026 and 2034, leading companies are expected to focus on:

GREENoneTEC and Solareast Group have been at the forefront of exporting large-scale collectors, while companies like Ormat and Sunoptimo are investing in modular system designs and solar-thermal hybridization with geothermal or biomass energy. Furthermore, regional companies such as Inventive Power and Módulo Solar are gaining ground in local industrial heat segments across Latin America.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Solar Thermal market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Collector

|

|

Type

|

|

System

|

|

Application

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report