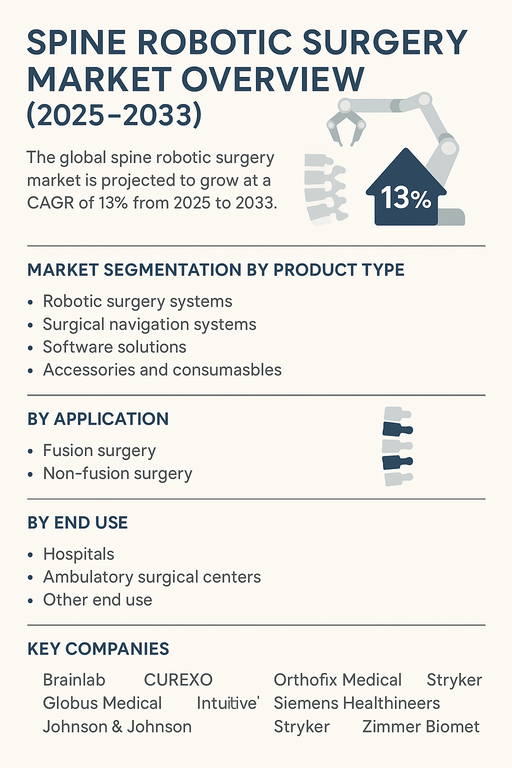

The global spine robotic surgery market is projected to grow at a CAGR of 13% from 2026 to 2034, driven by increasing demand for minimally invasive procedures, rising prevalence of spinal disorders, and continuous technological advancements in robotic-assisted surgery. Spine robotic systems are revolutionizing spinal surgeries by providing enhanced precision, reduced complication rates, and shorter recovery times compared to traditional approaches. The integration of navigation systems, AI-driven planning tools, and real-time imaging is improving surgical outcomes and patient safety, fueling strong adoption across hospitals and specialty centers worldwide.

Rising Demand for Minimally Invasive and Precision-Based Surgery

The market is witnessing strong growth due to the rising incidence of degenerative disc diseases, scoliosis, spinal injuries, and age-related spinal conditions. Patients and healthcare providers are increasingly favoring robotic-assisted surgeries as they enable higher accuracy, reduced blood loss, and faster recovery. Furthermore, the integration of surgical planning software and intraoperative navigation tools enhances the efficiency of spine surgeries. Growing investments in hospital infrastructure, training programs for surgeons, and the availability of robotic systems across advanced healthcare markets are accelerating adoption.

Challenges: High Costs and Technical Barriers

Despite rapid adoption, the spine robotic surgery market faces challenges such as the high cost of robotic systems, which restricts their penetration in cost-sensitive regions. The need for extensive training and technical expertise can limit accessibility in smaller healthcare facilities. Furthermore, concerns about system maintenance, long setup times, and reimbursement limitations pose barriers to broader adoption. However, continuous innovation, the development of compact and cost-effective systems, and favorable reimbursement initiatives in developed markets are expected to reduce these constraints and drive long-term market expansion.

Market Segmentation by Product Type

By product type, robotic surgery systems account for the largest market share, serving as the core technology in robotic-assisted spine procedures. Surgical navigation systems are also growing significantly as they enhance intraoperative visualization and complement robotic systems for greater accuracy. Software solutions are gaining importance, offering preoperative planning, AI-based analytics, and integration with hospital IT systems. Accessories and consumables, including robotic tools and disposable surgical kits, represent a recurring revenue stream, supporting the long-term growth of the market.

Market Segmentation by Application

Fusion surgery represents the dominant application segment, as robotic systems provide enhanced precision in placing screws and stabilizing spinal structures. Non-fusion surgeries, such as decompressions and tumor resections, are growing steadily as robotic systems expand their application scope beyond fusion procedures. The shift toward minimally invasive non-fusion approaches is expected to gain traction over the forecast period.

Market Segmentation by End Use

Hospitals remain the largest end-use segment, driven by their advanced surgical infrastructure, access to capital-intensive technologies, and availability of highly trained specialists. Ambulatory surgical centers are witnessing faster growth, particularly in developed markets, due to rising demand for cost-effective, same-day procedures supported by robotic assistance. Other end-use settings, including specialty spine clinics and research institutions, are gradually adopting robotic systems to expand their treatment capabilities.

Regional Insights

North America leads the spine robotic surgery market, supported by strong healthcare infrastructure, high adoption of advanced surgical technologies, and favorable reimbursement frameworks. Europe follows with steady growth, driven by rising investments in minimally invasive care and supportive regulatory pathways in countries such as Germany, France, and the UK. Asia Pacific is the fastest-growing region, fueled by large patient populations, rising prevalence of spinal disorders, and increasing investments in hospital robotics in countries like China, India, and Japan. Latin America and the Middle East & Africa are emerging markets where improving healthcare infrastructure and growing surgeon training programs are gradually expanding access to robotic spine surgery.

Competitive Landscape

The 2025 market was shaped by a mix of global medtech leaders and specialized robotic surgery innovators. Medtronic and Globus Medical are major players, offering advanced robotic-assisted platforms for spine surgery. Stryker and Zimmer Biomet maintain strong positions through their comprehensive surgical portfolios and innovation in robotic guidance systems. Intuitive Surgical Operations continues to expand its robotics expertise into the spine segment, leveraging its leadership in robotic-assisted surgery. Johnson & Johnson and B Braun are enhancing competitiveness with integrated surgical navigation solutions and robotic platforms. Siemens Healthineers and Brainlab are advancing imaging and navigation technologies that complement robotic systems. Emerging players such as CUREXO, Orthofix Medical, and R2 Surgical are introducing cost-effective and innovative solutions tailored for spine-specific applications. Competitive differentiation is being driven by system precision, AI-based planning, workflow integration, and cost-effectiveness, ensuring rapid innovation and transformation in the spine surgery landscape.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Spine Robotic Surgery market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product Type

|

|

Application

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report