The global surgical scissors market is projected to grow at a CAGR of 4.5% between 2026 and 2034, supported by the increasing number of surgical procedures, advancements in surgical instrumentation, and the steady rise in healthcare expenditure worldwide. Surgical scissors remain a vital tool across all surgical specialties due to their precision, ergonomic design, and safety, making them a cornerstone in most operating rooms. Continuous product innovation, strict sterilization standards, and the broad application of surgical scissors in both reusable and disposable formats contribute to stable demand across diverse medical and surgical domains.

Market Drivers

The growth of the surgical scissors market is driven by the increasing volume of surgeries globally, especially in cardiovascular, orthopedic, gastrointestinal, and neurology specialties. The ongoing focus on surgical accuracy, minimal invasiveness, and patient safety is further encouraging the adoption of specialized scissors that offer better control and reduced trauma during delicate procedures. In addition, rising hospital investments in surgical tools that help optimize workflow and cut operating times contribute to increased demand. Regulatory requirements emphasizing the use of high-quality surgical tools with proper certifications and enhanced sterilization compatibility also support this sustained market growth.

Market Restraint

Despite positive growth, the surgical scissors market is limited by cost pressures, especially for premium instruments. Healthcare facilities in price-sensitive regions often face budget constraints that impact the rate of adoption of advanced surgical instruments. Additionally, the need for regular maintenance and stringent sterilization protocols can add to the total cost of ownership for reusable scissors, creating a challenge for small clinics and resource-constrained hospitals.

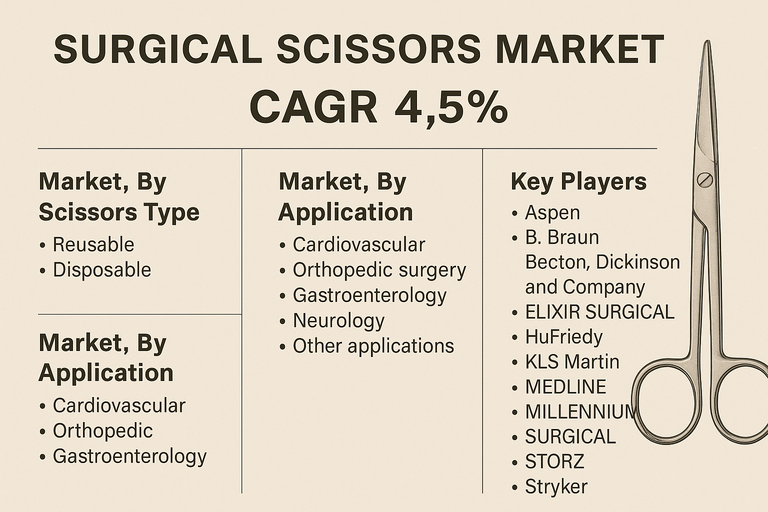

Market By Scissors Type

By scissors type, reusable surgical scissors accounted for the highest revenue share in 2025 owing to their durability and cost-effectiveness in high-volume surgical settings. Reusable scissors are preferred in larger hospitals and specialty clinics where instruments can be adequately sterilized and reused without compromising performance. The disposable surgical scissors segment is projected to grow at the highest CAGR due to their convenience, elimination of cross-contamination risks, and increasing preference for single-use instruments in day-surgery centers and outpatient facilities, especially in infection-prone procedures.

Market By Application

The surgical scissors market is segmented by application into cardiovascular, orthopedic surgery, gastroenterology, neurology, and other surgical specialties. Cardiovascular surgery led the market by revenue in 2025, driven by a high rate of heart surgeries and the increasing complexity of cardiovascular procedures. Orthopedic surgery is expected to register the highest CAGR due to the rising number of trauma and joint replacement procedures worldwide. Gastroenterology also holds a substantial share due to the high frequency of laparoscopic and gastrointestinal interventions that require specialized scissors. Neurology and other surgical specialties continue to present stable demand, supported by innovations in precision instruments and specialized surgical scissors that enhance outcomes.

Geographic Trends

North America dominated the surgical scissors market in 2025 due to advanced healthcare infrastructure, widespread surgical instrument usage, and stringent sterilization regulations that drive replacement rates. Europe followed as a key region, sustained by a focus on quality surgical tools, highly skilled surgical professionals, and steady investments in healthcare. Asia Pacific is projected to register the fastest CAGR through 2034 due to expanding hospital capacity, rising surgical volumes, improving healthcare standards, and increased training of healthcare professionals in countries like China, India, and South Korea. Latin America and the Middle East & Africa present emerging opportunities as governments and private healthcare operators modernize their surgical facilities and focus on patient safety.

Competitive Trends

The surgical scissors market features a diverse mix of global and regional players. Leading companies include Aspen, B. Braun, Becton, Dickinson and Company, ELIXIR SURGICAL, HuFriedy, INTEGRA, KLS Martin, MEDLINE, MILLENNIUM SURGICAL, SCANLAN, STORZ, Stryker, Surgicalholdings, Teleflex, and WPI, all competing on product quality, instrument ergonomics, durability, and service offerings. These companies leverage innovations in materials such as high-grade stainless steel and tungsten carbide inserts as well as strict quality controls to meet surgeon expectations. Strategic partnerships with hospitals, focus on after-sales services like instrument maintenance, and enhancements in supply chain efficiency will continue to shape competitive positioning. Going forward, the market will also witness increasing interest in disposable product lines and environmentally friendly solutions, allowing companies to align with sustainability goals and evolving customer preferences.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Surgical Scissors market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Scissors Type

|

|

Application

|

|

Material

|

|

Tip Shapes

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report