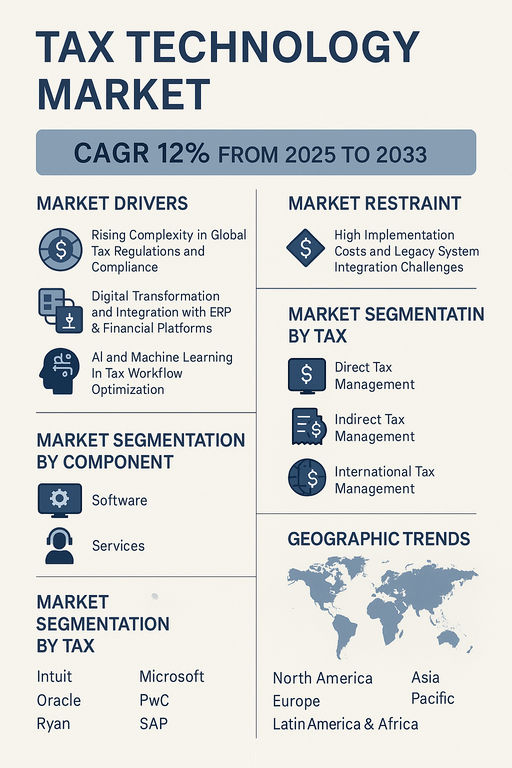

The global tax technology market is projected to grow at a CAGR of 12% from 2026 to 2034, driven by increasing digitalization of financial operations, rising complexity in global tax compliance, and the adoption of cloud-based and AI-powered tax management solutions. Enterprises and tax advisory firms are increasingly investing in intelligent tax automation platforms to enhance accuracy, ensure regulatory compliance, and reduce operational burden across direct, indirect, and international tax processes.

Market Drivers

Rising Complexity in Global Tax Regulations and Compliance

With evolving tax frameworks, especially in areas such as cross-border transactions, e-invoicing mandates, and digital service taxes, enterprises require automated solutions to ensure timely, accurate, and auditable tax filings. Governments across regions are also mandating real-time reporting and tax digitization, accelerating the shift toward tax technology adoption.

Digital Transformation and Integration with ERP & Financial Platforms

Organizations are embedding tax technology tools within their enterprise systems to streamline reporting, enhance audit readiness, and gain real-time visibility into tax liabilities. Cloud-based tax engines, automated filing modules, and data analytics capabilities are helping enterprises manage multi-jurisdictional tax operations more efficiently.

AI and Machine Learning in Tax Workflow Optimization

AI-powered tax solutions are being used for predictive tax analytics, anomaly detection, and risk scoring. Machine learning helps in the continuous improvement of tax coding accuracy, while natural language processing (NLP) enables better document review and regulation mapping.

Market Restraint

High Implementation Costs and Legacy System Integration Challenges

Despite significant benefits, tax technology platforms often require large upfront investments and complex integration with legacy ERP and accounting systems. Small and mid-sized enterprises (SMEs) face budget constraints and limited in-house IT capabilities, which can hinder adoption and limit full-feature utilization.

Market Segmentation by Component

The tax technology market is segmented into Software and Services. In 2025, the software segment dominated, driven by increased enterprise reliance on automation tools, tax engines, and analytics dashboards. However, services including implementation, consulting, and support are expected to grow steadily as companies seek tailored integration and compliance solutions across tax regimes.

Market Segmentation by Tax Type

By tax type, the market is divided into Direct Tax Management, Indirect Tax Management, and International Tax Management. Indirect tax management, including VAT, GST, and sales tax, held the largest share in 2025 due to varying jurisdictional requirements. International tax management is expected to grow fastest through 2034 due to expanding global operations, digital economy taxation, and OECD's BEPS implementation.

Geographic Trends

In 2025, North America led the tax technology market, supported by early adoption of automation and mature tax compliance frameworks across the U.S. and Canada. Europe followed, with growth driven by VAT digital reporting mandates, e-invoicing regulations, and increasing use of tax engines in EU member states. Asia Pacific is projected to register the highest CAGR from 2026 to 2034, led by rapid digitalization and GST/VAT reforms in India, China, and Southeast Asia. Latin America, especially Brazil and Mexico, is witnessing momentum due to evolving e-reporting mandates. The Middle East & Africa region is gradually embracing tax automation amid regulatory modernization and ERP investments in the UAE, Saudi Arabia, and South Africa.

Competitive Trends

The tax technology market in 2025 featured a mix of global enterprise software vendors and specialized tax solution providers. Intuit, Microsoft, and Oracle offered integrated tax modules as part of their broader financial and ERP platforms. SAP and Thomson Reuters dominated in enterprise-level indirect and international tax compliance tools. Vertex and Wolters Kluwer provided cloud-based and industry-specific tax automation solutions for corporate and advisory use cases. PwC and Ryan offered robust managed services and advisory-led platforms catering to large multinational clients. The competitive landscape is increasingly shaped by partnerships between software providers and tax firms, growing investment in AI-enabled solutions, and demand for real-time global compliance platforms.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Tax Technology market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Component

|

|

Tax

|

|

Deployment Mode

|

|

Organization Size

|

|

Application

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report