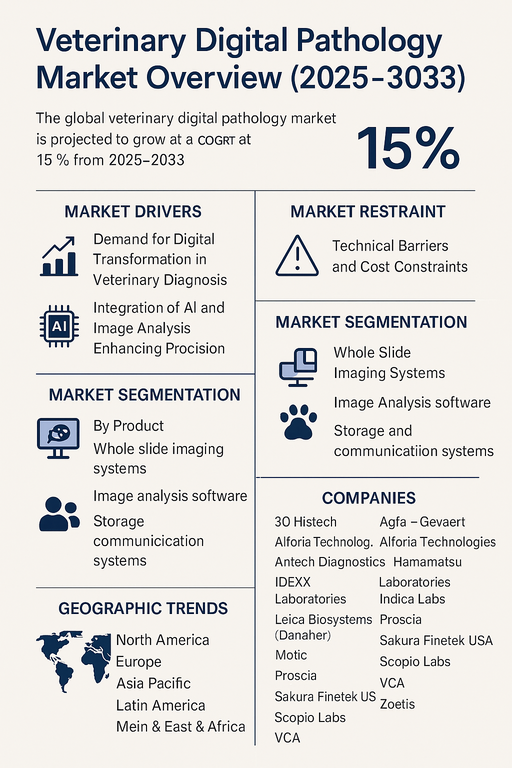

The global veterinary digital pathology market is projected to grow at a robust CAGR of 15% from 2026 to 2034. This high growth rate is attributed to the increasing demand for accurate and rapid diagnosis in animal healthcare, rising pet ownership, and advancements in digital imaging technologies. Veterinary digital pathology enables the digitization of glass slides for easier storage, remote consultations, and AI-based image analysis. It plays a critical role in improving diagnostic turnaround times, facilitating collaboration between veterinary pathologists, and enhancing the accuracy of disease detection in both companion and livestock animals.

Demand for Digital Transformation in Veterinary Diagnosis

The market is witnessing strong momentum as veterinary clinics, diagnostic laboratories, and research institutions increasingly adopt digital pathology solutions to modernize diagnostic workflows. Traditional pathology involving manual slide review under a microscope is time-consuming and limits accessibility. With whole slide imaging systems, veterinarians can digitize tissue samples and store them securely for easy sharing and analysis. This improves operational efficiency and enables second opinions from remote experts, particularly valuable in rural or under-resourced areas. The shift to digital solutions also supports the growing trend of telepathology in veterinary practice.

Integration of AI and Image Analysis Enhancing Precision

One of the core drivers of market expansion is the integration of AI-powered image analysis software, which enables the detection of subtle histopathological features with high precision. AI tools assist in the classification of tumors, detection of parasites, and grading of inflammatory conditions. These automated insights enhance diagnostic accuracy, reduce interobserver variability, and support faster treatment decisions. Research institutions are also leveraging digital pathology platforms for large-scale veterinary studies and comparative pathology research. The capability to process and analyze large image datasets in real-time is accelerating veterinary research and drug development.

Technical Barriers and Cost Constraints

Despite the growth potential, the market faces limitations related to high upfront costs, especially for small veterinary practices. Whole slide scanners, high-resolution monitors, and storage solutions require significant capital investment. Additionally, bandwidth limitations and data privacy concerns may affect cloud-based deployment in certain regions. Integration of digital pathology systems with existing laboratory information management systems (LIMS) can also present technical challenges. However, the emergence of scalable, modular solutions and cloud-native platforms is gradually lowering entry barriers, especially in emerging markets.

Product Segmentation Insights

By product, the market is segmented into whole slide imaging systems, image analysis software, and storage and communication systems. In 2025, whole slide imaging systems held the largest share due to their central role in digitizing pathology workflows. These systems are increasingly being adopted by veterinary diagnostic labs for high-throughput scanning and long-term archiving. Image analysis software is projected to witness the fastest growth rate during the forecast period, driven by advancements in AI and deep learning algorithms that enhance decision-making. Storage and communication systems are also critical for supporting teleconsultation and digital archiving needs, especially in multi-site veterinary networks.

Application Segmentation Insights

By application, the market is divided into diagnosis and research. Diagnostic applications accounted for the majority of revenue in 2025, supported by increasing use in clinical veterinary practices and animal hospitals. Digital pathology enables faster and more consistent diagnostic outcomes, particularly in oncology and infectious disease screening. The research segment is expected to grow significantly between 2026 and 2034, driven by increased R&D activities in veterinary oncology, zoonotic diseases, and drug development. Academic institutions and veterinary schools are also investing in digital tools for education and collaborative research projects.

Geographic Trends

North America held the largest share of the veterinary digital pathology market in 2025, owing to advanced veterinary infrastructure, high pet healthcare spending, and strong adoption of diagnostic technologies. The U.S. market is particularly driven by key players like IDEXX Laboratories, Zoetis, and VCA, which are investing in digital platforms to expand diagnostic capabilities. Europe followed closely, with countries like Germany, the UK, and the Netherlands adopting digital pathology in both companion and farm animal practices. Asia Pacific is expected to register the highest CAGR through 2034 due to growing veterinary healthcare awareness, government animal health initiatives, and expanding veterinary networks in China, India, and Southeast Asia. Latin America and the Middle East & Africa are emerging markets where telepathology and mobile diagnostic solutions are enabling access to specialized veterinary services.

Competitive Landscape

The veterinary digital pathology market in 2025 comprised established diagnostics companies and emerging tech firms offering end-to-end imaging and analysis solutions. IDEXX Laboratories, Zoetis, and VCA maintained strong leadership through their integrated diagnostic platforms and expansive clinical networks. Leica Biosystems (Danaher), Hamamatsu Photonics, and Sakura Finetek USA provided high-performance slide scanners and imaging hardware tailored for veterinary use. Agfa-Gevaert, 3DHistech, and Motic focused on digital slide systems and microscopy solutions for both diagnostics and research. Aiforia Technologies, Proscia, Indica Labs, and Scopio Labs led innovations in AI-based image analysis and cloud pathology platforms. Antech Diagnostics and Zoetis leveraged their extensive reach in veterinary care to promote digital adoption at the clinic level. The competitive focus is on enhancing software capabilities, ensuring system interoperability, and offering flexible cloud-based solutions that cater to diverse veterinary practice sizes and budgets.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Veterinary Digital Pathology market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product

|

|

Animal Type

|

|

Application

|

|

End Use

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report