The global winch market is projected to grow at a CAGR of 4.0% from 2026 to 2034, driven by the rising adoption of lifting and pulling equipment across industries such as construction, marine, oil & gas, and logistics. Winches are crucial for material handling, towing, and recovery applications in both industrial and commercial settings. Growing infrastructure development, offshore exploration, and vehicle recovery operations are key factors contributing to steady market expansion.

Growing Demand Across Industrial and Marine Sectors

The market’s growth is supported by increasing demand for compact and high-capacity winching systems capable of operating in harsh environments. In industrial sectors, winches are widely used for equipment lifting, pipeline tensioning, and ship anchoring. The marine industry, in particular, continues to drive demand through the use of hydraulic and electric winches for vessel mooring and offshore platform support. Moreover, technological innovations such as remote-controlled and automated winch systems are enhancing operational safety and efficiency.

Challenges: High Maintenance and Operational Costs

The winch market faces challenges related to high maintenance costs, wear-and-tear from continuous operation, and the need for periodic inspection and certification. Hydraulic systems, while powerful, are prone to leakage and demand regular servicing, impacting operational budgets. Furthermore, fluctuating raw material prices and stringent safety regulations pose cost-related challenges for manufacturers. However, the introduction of energy-efficient electric winches and the increasing preference for automated, low-maintenance systems are creating growth opportunities for market participants.

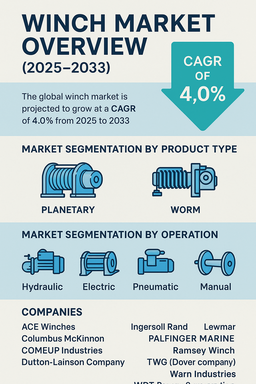

Market Segmentation by Product Type

By product type, the market is segmented into planetary and worm winches. In 2025, the planetary winch segment dominated the market due to its compact design, higher efficiency, and suitability for both industrial and off-road applications. Its ability to handle heavy loads with reduced power loss makes it ideal for construction, marine, and automotive uses. The worm winch segment, while slower, offers advantages in self-locking mechanisms and precise load control, making it a preferred choice for applications requiring stability and safety, such as cranes, hoists, and utility equipment.

Market Segmentation by Operation

By operation, the market is categorized into hydraulic, electric, pneumatic, and manual. The hydraulic winch segment held the largest share in 2025, favored in marine and offshore applications where high torque and durability are critical. Electric winches are expected to witness the fastest growth, supported by advancements in battery-powered systems and rising demand in automotive recovery and industrial automation. Pneumatic winches serve niche applications in hazardous environments, while manual winches remain popular in small-scale construction and recreational uses due to their simplicity and low cost.

Regional Insights

In 2025, North America led the winch market, driven by robust industrial infrastructure, expanding oil & gas operations, and high adoption of electric and hydraulic winches in vehicle recovery and construction. Europe followed closely, supported by growing maritime trade, offshore wind projects, and industrial automation initiatives. The Asia Pacific region is projected to register the highest CAGR during the forecast period, fueled by rapid industrialization, infrastructure expansion, and increasing shipbuilding activities in countries such as China, Japan, and South Korea. Latin America and Middle East & Africa (MEA) are emerging markets, with growth driven by mining projects, construction activities, and oilfield operations.

Competitive Landscape

The winch market is moderately fragmented, with both global and regional manufacturers competing through technological innovation and product customization. ACE Winches, Ingersoll Rand, Columbus McKinnon, and PALFINGER MARINE are leading players, offering advanced hydraulic and electric winch systems for heavy-duty applications. Warn Industries, Superwinch, and Ramsey Winch focus on automotive and off-road recovery winches, while Lewmar specializes in marine equipment. Companies such as COMEUP Industries, Rotzler, Thern, and TWG (Dover Company) emphasize durability and safety compliance in industrial-grade models. WPT Power Corporation, Transvictory Winch System, and Dutton-Lainson Company cater to regional demand through efficient distribution networks and customizable solutions. Strategic initiatives center on product innovation, operational automation, and geographic expansion to strengthen market presence and improve customer access worldwide.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Winch market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Product Type

|

|

Operation

|

|

Pulling Capacity

|

|

Application

|

|

End Use Industry

|

|

Distribution Channel

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report