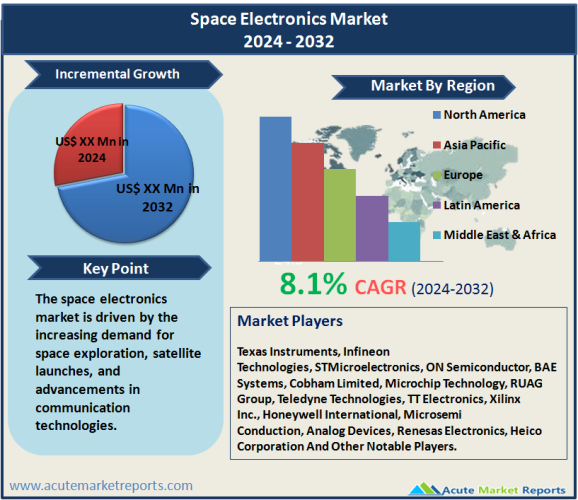

The space electronics market is expected to grow at a CAGR of 8.1% during the forecast period of 2026 to 2034, driven by the increasing demand for space exploration, satellite launches, and advancements in communication technologies. Power electronics are critical components in space missions, providing the electrical power management and distribution necessary to ensure the optimal functioning of satellites, spacecraft, and other space systems. In 2025, the market experienced robust growth due to the rising number of satellite launches for both government and commercial purposes, as well as technological innovations in power modules and discrete devices designed specifically for the harsh conditions of outer space. Moving forward, from 2026 to 2034, the market is expected to witness significant expansion as the commercial space industry, driven by companies like SpaceX and Blue Origin, continues to grow. The increasing number of small satellite constellations and the rise of space-based internet services, such as SpaceX’sStarlink, are also projected to fuel market demand for reliable, efficient, and durable power electronics.

Drivers of the space electronics market

Rising Number of Satellite Launches and Space Exploration Missions

One of the key drivers of the space power electronics market is the increasing number of satellite launches. In 2025, the global space industry saw a record number of satellite deployments, with companies and governments launching a mix of communication, observation, and research satellites. The demand for low-earth orbit (LEO) satellites has surged, driven by the need for global internet coverage, navigation services, and scientific research. For instance, SpaceX alone launched more than 60 Starlink satellites in 2025 as part of its goal to create a global broadband internet service. As the number of satellites grows, so too does the need for power electronics that can manage, convert, and distribute power within these satellites, ensuring their longevity and functionality in space. The harsh conditions of space, including radiation exposure, extreme temperatures, and vacuum environments, make power electronics a critical component in ensuring the success of these missions. Additionally, government space agencies such as NASA, the European Space Agency (ESA), and the Indian Space Research Organization (ISRO) continue to fund exploratory missions to the Moon, Mars, and beyond, further increasing the demand for advanced power electronics systems. From 2026 to 2034, the number of satellite launches is expected to rise significantly, fueled by continued commercial investments in space technology and global efforts to expand satellite-based services such as weather monitoring and defense.

Technological Advancements in Power Electronics Components

Technological innovations are playing a critical role in the growth of the space power electronics market. In 2025, advancements in power modules, discrete components, and integrated circuits designed for space applications drove a significant portion of the market’s revenue. For example, developments in Gallium Nitride (GaN) and Silicon Carbide (SiC) semiconductors have enabled the creation of smaller, more efficient, and more durable power devices that can operate at higher temperatures and frequencies compared to traditional silicon-based systems. These advancements have resulted in improved power density, reduced weight, and higher efficiency, all of which are crucial for space applications where every gram of weight and watt of power counts. Additionally, innovations in energy storage, such as high-efficiency battery systems, are further enhancing the performance of space power electronics. Companies such as Texas Instruments and Infineon Technologies have been at the forefront of these technological innovations, developing cutting-edge components that are specifically designed for use in space environments. Looking ahead to the forecast period of 2026 to 2034, these technological advancements are expected to continue to shape the market, as demand for smaller, lighter, and more efficient power electronics components increases, particularly for small satellite constellations and deep-space exploration missions.

Growth of the Commercial Space Industry

The commercial space industry has been a major driver of the space power electronics market, with companies such as SpaceX, Blue Origin, and Rocket Lab leading the charge in terms of satellite launches and space exploration. In 2025, the commercial space sector generated significant revenue from satellite launches, space tourism, and space station logistics, all of which require advanced power electronics for efficient and reliable operation. The entry of private companies into what was once the exclusive domain of government space agencies has dramatically changed the landscape of the industry. SpaceX, for example, has revolutionized the launch market with its reusable rocket technology, which significantly reduces the cost of launching payloads into space. This has led to a sharp increase in satellite launches for both commercial and governmental customers, creating new opportunities for power electronics manufacturers. Blue Origin has also invested heavily in space tourism and lunar exploration, further expanding the market for power electronics used in spacecraft and lunar landers. The trend toward privatization in the space industry is expected to accelerate over the forecast period of 2026 to 2034, with more private companies entering the market and launching missions ranging from satellite constellations to deep-space exploration. As a result, the demand for high-reliability, high-performance power electronics systems will continue to grow, driving the overall market expansion.

Restraint in the space electronics market

High Costs of Development and Manufacturing

One of the primary challenges facing the space electronics market is the high cost of development and manufacturing. Space-qualified electronics components must meet stringent requirements for reliability, radiation resistance, and durability, which significantly increases the cost of design, testing, and production. In 2025, many companies struggled with the high costs associated with producing power electronics systems that meet space-grade standards, as these components require extensive testing in simulated space environments to ensure they can withstand the harsh conditions of outer space. For example, semiconductors used in space must be radiation-hardened to prevent malfunction due to cosmic radiation exposure, and this process can increase production costs by up to 50%. Additionally, space missions often require custom-designed power systems that are tailored to the specific needs of a satellite or spacecraft, further driving up costs. As a result, smaller companies and startups in the space industry may find it difficult to enter the market, limiting innovation and competition. This cost barrier is expected to remain a challenge throughout the forecast period from 2026 to 2034, although advances in technology and manufacturing processes may help to mitigate these costs over time.

Market Segmentation by Device Type

The space electronics market is segmented by device type into power discrete, power modules, and power ICs. In 2025, power discrete devices, including diodes and transistors, held the highest revenue share due to their widespread use in a variety of space applications. Power discrete devices are essential for managing electrical currents in spacecraft and satellites, and their high reliability and performance under extreme conditions make them a critical component in space missions. However, power modules are expected to witness the highest compound annual growth rate (CAGR) during the forecast period of 2026 to 2034, driven by the increasing demand for integrated and intelligent power management systems. Power modules, including intelligent power modules (IPMs) and integrated power modules, are designed to provide more efficient power conversion and control, which is essential for optimizing the performance of spacecraft and satellites. Power ICs, including application-specific ICs and power magnet ICs, also represent a growing segment of the market, with demand expected to rise as more complex space missions require sophisticated power management solutions.

Market Segmentation by Application

The space electronics market is segmented by application into satellites, spacecraft and launch vehicles, rovers, and space stations. In 2025, satellites accounted for the highest revenue share, as they represent the largest segment of space-related power electronics demand. The proliferation of small satellites and satellite constellations for communications, Earth observation, and research purposes has significantly increased the need for power electronics that can efficiently manage power distribution and control within these systems. However, spacecraft and launch vehicles are expected to witness the highest CAGR from 2026 to 2034, as the number of deep-space missions, lunar exploration, and Mars missions grows. Power electronics are crucial for the propulsion systems, command and control systems, and energy storage systems in these spacecraft, and the increasing complexity of these missions is driving the demand for more advanced power electronics solutions. Rovers and space stations also represent significant market segments, with power electronics playing a key role in enabling these systems to operate autonomously in remote environments and under extreme conditions.

Market Segmentation by Platform Type

The market segmentation by platform type includes power, command, and data handling (C&DH), attitude determination and control systems (ADCS), propulsion, telemetry, tracking, and control (TT&C), structure, and thermal systems. In 2025, power systems held the highest revenue share, as power management and distribution are essential components of any space mission. The power platform ensures that all systems within a spacecraft or satellite receive the necessary electrical power to operate, making it a critical element of space missions. However, command and data handling (C&DH) systems are expected to experience the highest CAGR from 2026 to 2034, driven by the increasing need for sophisticated data processing and communication systems in space missions. C&DH systems manage the collection, processing, and transmission of data, and the growing complexity of space missions, including scientific research and deep-space exploration, is expected to drive demand for advanced power electronics in this area. Propulsion systems also represent a growing segment, as the need for more efficient and reliable propulsion technologies continues to rise with the expansion of space exploration efforts.

Market Segmentation by Voltage

In the space electronics market, voltage segmentation includes low-voltage, medium-voltage, and high-voltage systems. In 2025, low voltage systems accounted for the highest revenue, as they are commonly used in small satellites and other space systems that require lower power levels for operation. However, high-voltage systems are expected to witness the highest CAGR during the forecast period of 2026 to 2034, driven by the increasing power demands of larger spacecraft, space stations, and deep-space exploration missions. High voltage systems are crucial for powering propulsion systems, energy storage, and advanced communication systems in space, and their growing importance is expected to drive significant market growth.

Market Segmentation by Current

The market is further segmented by current levels, including up to 25A, 25-50A, and over 50A. In 2025, power electronics systems with up to 25A accounted for the highest revenue share, as these systems are widely used in small satellites and other low-power space applications. However, systems with over 50A are expected to witness the highest CAGR from 2026 to 2034, as larger spacecraft and deep-space missions require higher current levels to support their energy-intensive systems. The growing demand for power electronics capable of handling higher currents is expected to drive significant market growth, particularly in the areas of propulsion and energy storage.

Market Segmentation by Material

The market is segmented by material into silicon, silicon carbide (SiC), gallium nitride (GaN), and others. In 2025, silicon-based power electronics held the highest revenue share due to the widespread use of silicon in power devices for space applications. However, gallium nitride (GaN) is expected to witness the highest CAGR during the forecast period of 2026 to 2034, as GaN-based devices offer superior performance in terms of efficiency, power density, and thermal management. GaN and SiC are particularly well-suited for high-power and high-frequency applications in space, and their adoption is expected to grow significantly as space missions become more complex and power demands increase.

Geographic Segment

In terms of geographic segmentation, North America accounted for the highest revenue share in 2025, driven by the presence of major space agencies such as NASA and private companies like SpaceX, Blue Origin, and Lockheed Martin. The U.S. leads the global space industry in terms of satellite launches, space exploration missions, and technological innovation, making it the largest market for space power electronics. However, the Asia-Pacific region is expected to witness the highest CAGR from 2026 to 2034, driven by the growing space programs in countries such as China, India, and Japan. China’s ambitious space program, including plans for lunar exploration and a space station, is expected to significantly drive demand for space power electronics in the region. India’s ISRO is also investing heavily in space exploration, with plans for multiple satellite launches and deep-space missions. Europe also represents a key market, with the European Space Agency (ESA) continuing to fund space exploration missions and satellite deployments.

Competitive Trends

The space electronics market is characterized by the presence of several major players, including Texas Instruments, Infineon Technologies, STMicroelectronics, ON Semiconductor, BAE Systems, Cobham Limited, Microchip Technology, RUAG Group, Teledyne Technologies, TT Electronics, Xilinx Inc., Honeywell International, Microsemi Conduction, Analog Devices, Renesas Electronics, and Heico Corporation. In 2025, these companies generated significant revenue from the sale of power electronics components designed specifically for space applications. Texas Instruments, for example, has developed a range of radiation-hardened power management devices that are used in satellites and spacecraft, while Infineon Technologies has focused on developing GaN and SiC-based power electronics for high-power applications. Looking ahead to the forecast period of 2026 to 2034, these companies are expected to continue investing in research and development to create more advanced power electronics solutions that can meet the growing demands of the space industry. Collaboration with space agencies and private companies is also expected to play a key role in the competitive landscape, as these partnerships enable companies to develop customized solutions for specific space missions. Additionally, the growing trend toward privatization in the space industry is expected to attract new players to the market, further intensifying competition.

Historical & Forecast Period

This study report represents analysis of each segment from 2024 to 2034 considering 2025 as the base year. Compounded Annual Growth Rate (CAGR) for each of the respective segments estimated for the forecast period of 2026 to 2034.

The current report comprises of quantitative market estimations for each micro market for every geographical region and qualitative market analysis such as micro and macro environment analysis, market trends, competitive intelligence, segment analysis, porters five force model, top winning strategies, top investment markets, emerging trends and technological analysis, case studies, strategic conclusions and recommendations and other key market insights.

Research Methodology

The complete research study was conducted in three phases, namely: secondary research, primary research, and expert panel review. key data point that enables the estimation of Space Electronics market are as follows:

Market forecast was performed through proprietary software that analyzes various qualitative and quantitative factors. Growth rate and CAGR were estimated through intensive secondary and primary research. Data triangulation across various data points provides accuracy across various analyzed market segments in the report. Application of both top down and bottom-up approach for validation of market estimation assures logical, methodical and mathematical consistency of the quantitative data.

| ATTRIBUTE | DETAILS |

|---|---|

| Research Period | 2024-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Year | 2024 |

| Unit | USD Million |

| Segmentation | |

Device Type

|

|

Application

|

|

Platform Type

|

|

Voltage

|

|

Current

|

|

Material

|

|

|

Region Segment (2024-2034; US$ Million)

|

Key questions answered in this report